What's the idea?

- After taking office in January 2025, new US President Donald Trump, a supporter of conventional energy, may introduce measures to support the industry, which could increase demand for the services of oilfield services companies such as Weatherford. The possible measures include:

- revising Joe Biden's offshore oil and gas permitting plan and radically increase the number of new drilling auctions;

- lifting the moratorium on liquefied natural gas (LNG) exports from new projects;

- redirecting budget incentives from renewable energy projects to hydrogen production and carbon capture and storage projects;

- imposing tariffs on US oil imports.

- Weatherford is active in M&A transactions, focusing on smaller companies with promising technologies that the company can acquire at a relatively low price.

- Weatherford is implementing a share buyback programme equivalent to 7.24% of its current market capitalisation. In addition, the company has started paying dividends with an annualised yield of 1.17%.

About Company

Weatherford International (WFRD) is a major oilfield services company that provides a complete range of services for the exploration, drilling, servicing, stabilising and completion of oil and gas wells. Founded in 1941, the company operates in 75 countries worldwide and is headquartered in Texas, USA.

Why do we like Weatherford International PLC?

Reason 1. Donald Trump's victory in the US election

Weatherford International is a major oilfield services company providing a full range of services in the exploration, drilling, servicing, stabilising and completion of oil and gas wells. The company operates in 75 countries around the world, working on both onshore and offshore hydrocarbon projects.

Following Donald Trump's recent victory in the US presidential election, the country's oilfield services industry could see an increase in demand for its products and services. During his campaign, Trump made a number of promises to the oil and gas industry, summarized in the phrase "Drill, baby, drill". The earnings of oilfield service companies are affected far more by production volumes and dramatic changes in market conditions than by energy prices. As a result, Trump's inauguration could have a positive impact on the value of companies in the sector.

In his pre-election speeches, the US President-elect announced the following measures:

Expanding auctions for oil and gas drilling on federal lands. During the campaign trail, Trump repeatedly called for expanding the allocation of new offshore oil and gas development areas to businesses, compared to the 5-year plan Biden approved in 2023. The plan includes holding just three auctions to allocate offshore areas to the private sector for development in 2025, 2027 and 2029. US authorities under Biden also imposed a rule banning drilling in more than half of the National Petroleum Reserve areas in Alaska. The measures resulted in a record low number of offshore development permits being issued since the Second World War. By comparison, the Trump plan approved in 2018 called for 47 auctions over its lifetime, and no such plan since 1992 has included fewer than 11 auctions.

Analysts believe that Trump could radically revise this policy immediately upon taking office, instructing industry executives to immediately increase the number of auctions. In addition, lifting the ban on drilling in Alaskan waters could boost oil and gas development in the region: many companies have rights to acreage there but cannot drill because of the Biden ban.

Thus, a revision of the past administration's plan to authorize offshore oil leases could lead to a significant increase in demand for oilfield services products and services as US companies begin drilling in new areas.

Lifting the moratorium on issuing new LNG export permits. In early 2024, Biden suspended the review of LNG export applications for new projects. This decision, which was welcomed by climate activists, delayed the start-up of new liquefaction plants and created uncertainty in the industry.

Trump has signaled in his campaign speeches that he will reverse this decision once he takes office. If this happens, it could boost investment in gas production, which would increase demand for oilfield services companies' services. Against this backdrop, the stock price of Energy Transfer LP, one of the key companies involved in LNG exports, have risen by almost 10% since Trump won the election.

Antagonism towards the green energy industry. It is well known that Trump is an ardent skeptic of renewable energy sources (RES), prioritizing investments in the extraction of energy resources from conventional deposits. Therefore, it is to be expected that the new US administration may support a radical reduction of investments in the RES sector.

Similar to Biden's LNG decision, Trump could support a ban on new offshore wind farm permits. As a presidential candidate, Trump repeatedly cited wind farms as the cause of whale and bird deaths. At the same time, lawyers say it would be extremely difficult to challenge such a ban in court.

Eco-activists also fear the possible repeal of The Inflation Reduction Act, which provides for large-scale investment in the renewable energy industry, now that the Republican Party has gained control of the US Congress. However, analysts believe it is unlikely to be repealed. However, it is very likely that the priorities for the allocation of funds will change: instead of renewable energy, investment will be directed towards hydrogen production and carbon capture and storage (CCS) projects. Both types of projects require specialised oilfield service companies, as hydrogen is produced using natural gas, while CCS requires drilling and stabilisation of wells.

Macroeconomic effects of reduced investment in RES. Trump's return to power may put the renewable energy industry in a less favorable position. As it becomes less profitable to invest in green energy than in conventional energy, we can expect to see an increase in oil and gas production in the US and globally, which will also increase demand for oilfield services companies, even though energy prices are likely to fall.

Massive imposition of duties. Trump is an advocate of setting quotas on imports of raw materials and goods into the US. As a candidate for the presidency, Trump has stated that he would support imposing 10%–20% duties on the country's oil imports, which could significantly change the existing balance in the market. According to The US Energy Information Administration (EIA), daily US oil consumption in 2024 was about 20.3 million barrels per day (b/d), while US oil imports in July 2024 reached 7.1 million b/d, more than a third of daily consumption.

If the new US administration imposes tariffs on oil imports, oil production in the country may become more profitable than imports, which could increase investment in the industry. In addition, the tariffs may help US producers to keep prices for crude oil and petroleum products at reasonable levels and avoid a significant drop in prices as a result of increased production.

During the election campaign, Trump announced a number of measures to support the conventional hydrocarbon production industry in the US. It is not certain that all of these will be implemented, but the adoption of even some of these measures could lead to a significant increase in demand for the services of oilfield services companies, including Weatherford International.

It is also worth noting that oil and gas companies were the largest contributors to Trump's election campaign. Only the visible part of the money received directly from the industry amounted to about $75 million, which is the best evidence that the sector has high hopes for the new president.

Reason 2. Business expansion through M&A transactions

In today's oilfield services business, maintaining technology leadership is critical as efficiency gains open the door to higher margins.

In this respect, Weatherford's M&A strategy looks promising. Instead of acquiring large companies and then integrating them into the overall business over a long period of time, Weatherford finds small companies with innovative technologies that can be quickly scaled across the company.

For example, in early 2024, Weatherford acquired two companies, Probe and Impact Selector International, that specialize in cable solutions for the energy industry. Probe and Impact Selector International's products improve the speed and quality of oil and gas well monitoring, reservoir health, and asset management.

In addition, earlier this year Weatherford acquired Ardyne, with whom the company entered into a strategic partnership in 2022. Ardyne specializes in well completion technologies, enabling the complete cessation of mineral pumping or reducing production from inefficient fields to 70%–80% of initial production rates. The deal strengthens Weatherford's position in its respective markets, as the company's completion customer offering was previously not fully responsive to customer needs.

As Weatherford management noted, all three transactions met the strict criteria of the company's M&A strategy and immediately contributed to net income generation. The acquisition cost of all three companies amounted to $136 million.

Continuing its policy of strengthening its technology leadership, in September 2024, Weatherford acquired Datagration Solutions, an innovator in unified data integration, analytics and machine learning for the energy industry, for $160 million. Datagration's products provide a powerful solution to monitor, optimize and manage a well throughout its lifecycle and accelerate the digital transformation of oil and gas companies.

According to Weatherford management, the integration of Datagration's products into the company's ecosystem will create synergies by combining them with the company's existing remote well control platforms —ForeSite®, CygNet® and CENTRO®.

It is worth noting that Weatherford continues to generate strong free cash flow: $0.65 billion over the last 12 months. Combined with high cash reserves ($920 million at the end of Q3 2024), this allows Weatherford to participate in M&A transactions without significant external financing.

Thus, Weatherford has an effective M&A policy: it acquires small companies with technologies it is interested in. As a result, Weatherford acquires promising technologies at a relatively low price. We believe that maintaining this policy will allow the company to achieve its margin growth targets.

Reason 3. Capital allocation

Recently, Weatherford has been more active in returning capital to shareholders. In particular, the company recently announced its first share repurchase program and dividend payment.

At the end of Q3 2024, the authorised amount of Weatherford's share buyback program was $449.79 million, or 7.24% of the company's current market capitalisation.

In addition, Weatherford declared its first quarterly dividend of $0.25 per share for Q3 2024, representing an annualised yield of approximately 1.17%.

We believe that these actions could draw investors' attention to the company and also indicate that management believes the stock is undervalued.

Financial performance

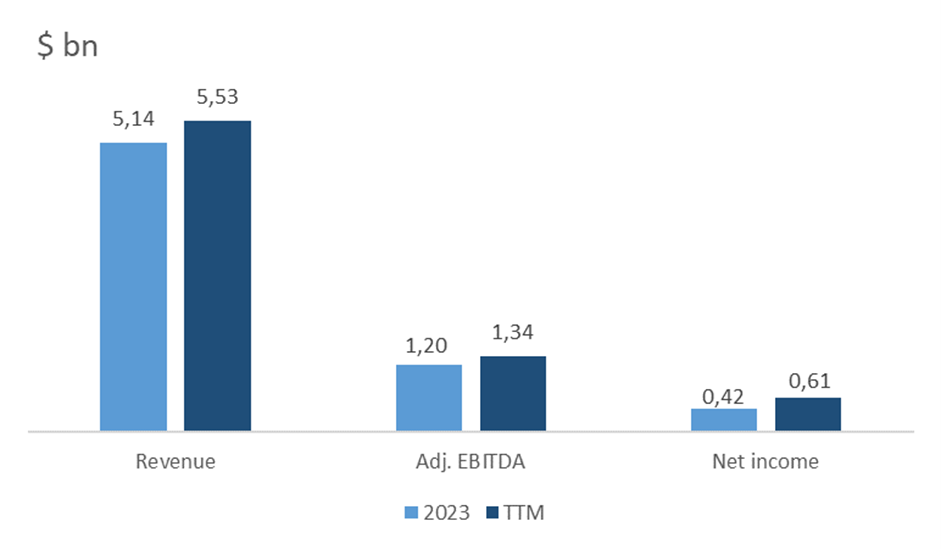

Weatherford's financial results for the past 12 months (TTM) can be summarized as follows:

- Revenue totaled $5.53 billion, a 7.77% increase over FY2023.

- Adj. EBITDA increased from $1.20 billion to $1.34 billion. EBITDA margin increased from 23.37% to 24.29%.

- Net income was $0.61 billion compared to $0.42 billion at the end of the previous fiscal year.

The increase in revenue and earnings was driven by increased activity across all segments, which also benefited the company's results for the first nine months (9M) of 2024.

Dynamics of the company's financial indicators

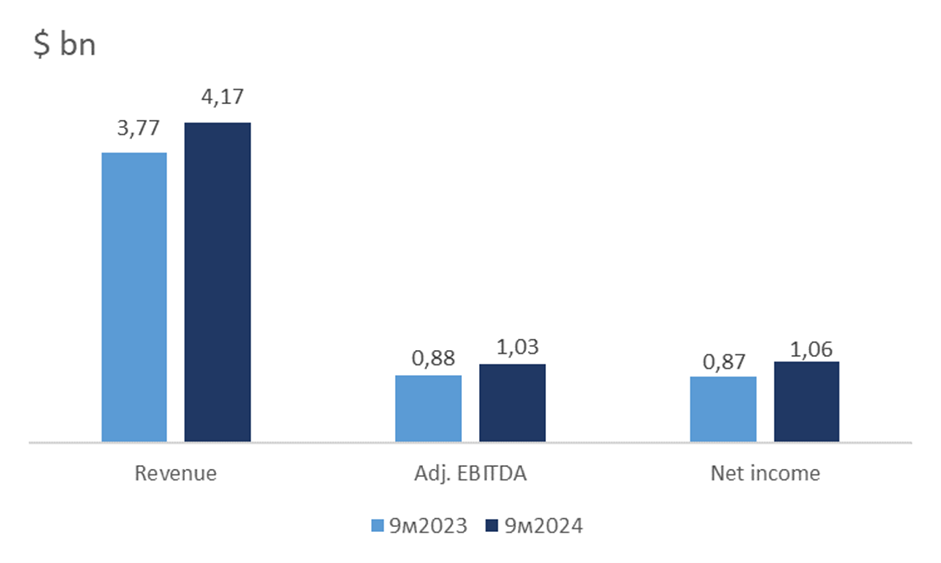

Weatherford's results for 9M 2024 are summarized below:

- Revenue rose 10.58% year-over-year (YoY) to $4.17 billion.

- Adj. EBITDA increased from $0.88 billion to $1.03 billion.

- Net income was $1.06 billion compared to $0.87 billion a year earlier.

Dynamics of the company's financial results for 9M 2024

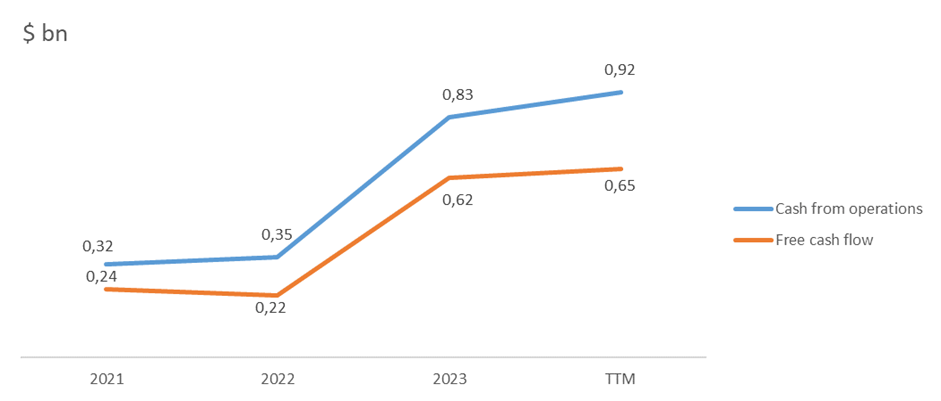

- In the last 12 months, Weatherford's operating cash flow has increased to $0.92 billion compared to $0.83 billion at the end of 2023.

- Free cash flow increased to $0.65 billion from $0.62 billion.

The increase in operating and free cash flow was mainly due to higher earnings from our largest customer in Mexico.

Company cash flow

Weatherford's balance sheet can be characterized as healthy:

- Total debt is $1.82 billion.

- Cash equivalents accounted for $920 million.

- The Net debt to Adj. LTM EBITDA ratio is 0.7x.

- The interest expense coverage ratio is 12.4x.

This level of debt load indicates excellent financial stability of the company.

Stock valuation

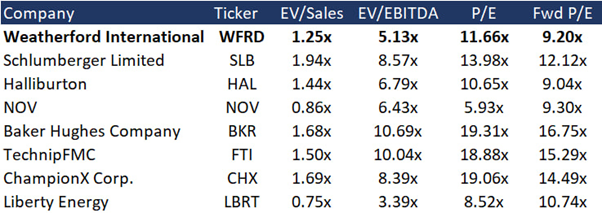

Weatherford is trading at a discount to the industry average, with EV/Sales at 1.25x, EV/EBITDA at 5.13x, P/E at 11.66x, and Fwd P/E at 9.20x.

Price targets of investment banks

Key risks

Significant decline in oil prices. If Trump's initiatives or other reasons lead to a significant drop in oil prices, oil and gas companies may experience a decline in profits and, in this context, reduce investment in exploration and drilling, which could adversely affect the performance of oilfield service companies.

Stagnation of OPEC production capacity. If US oil production increases in the near future, OPEC will be forced to further reduce production capacity. This in turn could reduce demand for oilfield services outside the US.

Rapid development of renewable energy production. In the event of a more active development of the green energy sector, including outside the US, global oil consumption will be limited and declining, so investment in the oil and gas industry may be limited to maintaining current production without investing in new projects, which could negatively impact Weatherford's backlog.