What's the idea?

- The company worsened its forecasts in the latest report, but with a positive economic scenario, it has a chance of exceeding expectations.

- New acquisitions will ensure revenue growth.

- Spin-offs will help them to manage their capital more effectively.

- The high potential return on the idea comes with significant downside risks in the event of a deteriorating macroeconomic environment.

About Company

Vista Outdoor Inc. designs and sells products for outdoor recreation and shooting sports. The company's products are designed for tourists, golfers, campers, hunting and shooting enthusiasts, as well as members of the uniformed services. The company's business consists of two main segments: Sporting Products (ammunition, components and related equipment for hunters, law enforcement and military) and Outdoor Products (outdoor equipment for cyclists, campers, skiers, golfers and others).

Why do we like Vista Outdoor Inc When Issued?

Reason 1. Takeovers

Vista Outdoor closed two takeover deals in August:

- On 8 August, the company announced the closing of its acquisition of the renowned global motocross, mountain bike and recreational equipment brand Fox Racing for $540 million, with an optional consideration of a further $50 million based on financial results. Fox Racing is expected to post calendar year 2022 revenues and adjusted EBITDA of $350 million and $50 million, respectively.

- The purchase of fishing products company Simms Fishing Products for $192.5 million was completed on 23 August, subject to a future tax break of $20 million.

The new acquisitions will help Vista Outdoor expand its product portfolio and increase its customer base. In addition, the acquisitions will help to better diversify the business of the Outdoor Products segment, which is expecting a spin-off in 2023.

Reason 2. Spin-off

On 5 May, it was announced that Vista Outdoor will be split into two independent companies in order to maximise long-term value creation. Among the benefits of such a separation are an improved strategic focus for each business area and the ability to tailor capital allocation, which should help to accelerate growth:

- A Growth strategy was chosen for Outdoor Products — capital will be invested in organic growth and M&A deals.

- For Sporting Products, a Value strategy is planned ¬— the capital allocation will be aimed at reducing the debt burden and paying dividends.

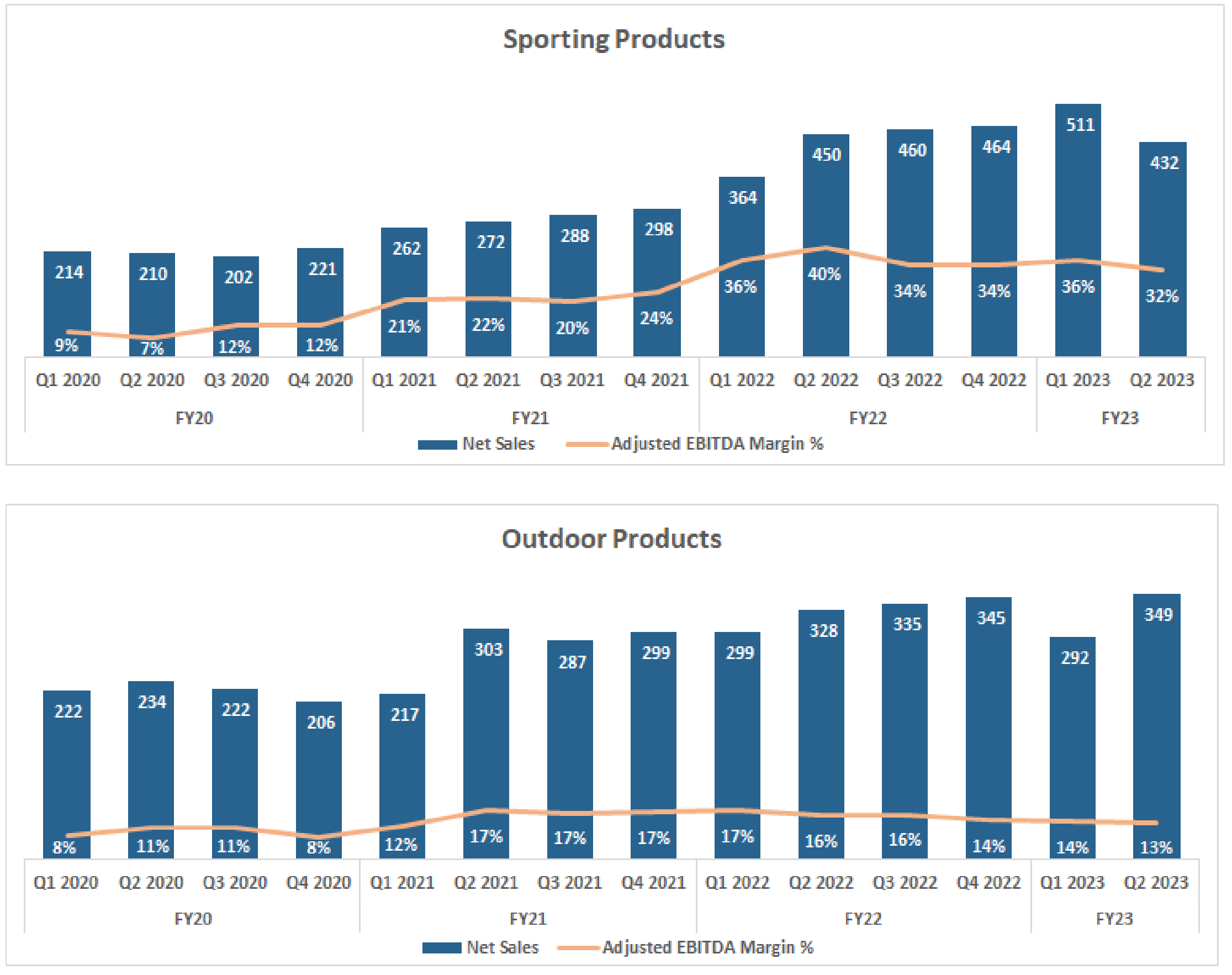

We believe this is the right approach because, as the charts below show, Sporting Products already has quite high business margins, while Outdoor Products has yet to optimise business processes and gain synergies from mergers to achieve higher profitability.

There was a similar case earlier when Smith & Wesson split into two parts: Smith & Wesson Brands, which is in the gun business, and American Outdoor Brands, which offers outdoor products. Before the split, the company had a market capitalisation of $1.02 billion as of 31 July 2020. Six months after that, on 31 December, the total market capitalisation of the two companies was $1.23 billion and a year later it was $1.96 billion.

Given the significantly different macroeconomic environment, we do not expect the same rapid growth rate after the Vista Outdoor split, but we believe such an operation will help the business grow more efficiently.

Reason 3. Improved macroeconomic environment

In presenting results for the latest reporting period, Vista Outdoor lowered its FY2023 forecasts, shifting revenue expectations from $3.2 billion-$3.325 billion to $3.05 billion-$3.15 billion and adjusted EBITDA margin expectations from 21.0%-21.5% to 19.75%-20.25%. The projected range of adjusted earnings per share also decreased from $7.05-$7.65 to $6-$6.50.

Management cited inflation and rising interest rates as the main reasons for the change in expectations, which are affecting consumer spending, as well as an increase in inventories. Reduced outlooks by now have been priced in, but in our view the impact of these drivers may be less severe due to an accelerating decline in inflation in the first half of 2023, as we have previously described.

In addition, the US Bureau of Economic Analysis released figures on 9 November showing that the outdoor recreation market will generate $862 billion in economic returns in 2021, showing growth of 25% year-on-year. Legislation, including those promoted by Vista Outdoor, could support the market's growth rate, including:

- Outdoor Recreation Act

- the Simplifying Outdoor Act

- Access for Recreation Act

- the Gateway Community and Recreation Enhancement Act

- the Biking on Long Distance Trails Act

The above acts will encourage the development of infrastructure for active recreation — government support can attract more people to active recreation and support an industry that generates 1.9% of US GDP. We expect the market to react positively and the company's stock price to rise if the approval of the acts moves forward.

Financial indicators

The company's results for the last 12 months:

- TTM revenue: up from $2.61 billion to $3.19 billion

- TTM operating profit: up from $496.1 million to $615.4 million

in terms of operating margins, an increase from 19.0% to 19.3%

- TTM net profit: up from $388.2 million to $485.8 million

in terms of net margin, down from 14.9% to 14.1%

- Operating cash flow: up from $252.7 million to $406.5 million thanks to positive changes in working capital

- Free cash flow: increase from $217.8 million to $365.2 million

Based on the results of the most recent reporting period ended 25 September 2022:

- Revenue: up from $778.5 million to $781.7 million

- Operating profit: down from $190.7 million to $131.2 million:

in terms of operating margins, decrease from 24.5% to 16.8% due to an increase in cost of revenue from 61.6% to 66.4% and an increase in SG&A expenses from 13.1% to 16.9%

- Net income: down from $139.5 million to $93.5 million:

in terms of net margin, down from 17.9% to 12%

- Operating cash flow: up from $105.2 million to $193.4 million thanks to positive changes in working capital

- Free cash flow: up from $90.7 million to $180.4 million

Vista Outdoor has shown good financial performance over the past year, but has weakened in the last quarter. We believe that this is already built into the stock price and will be recouped in the future if the macroeconomic situation recovers and the company's financial results improve.

- Cash and cash equivalents: $66 million

- Net debt: $1.24 billion

- Net Debt/LTM adj. EBITDA: 1.7x

Vista has a moderate level of debt, but a fairly low cash and cash equivalents reserve, which resulted from the investment in the acquisitions of the companies. Note that the company has an undrawn credit line of $55 million to provide liquidity. We expect that the acquired companies will further increase Vista Outdoor's cash flows and allow it to reduce its debt burden in the medium term.

Evaluation

In terms of trading multiples, Vista Outdoor is undervalued relative to the industry:

Ratings of other investment houses

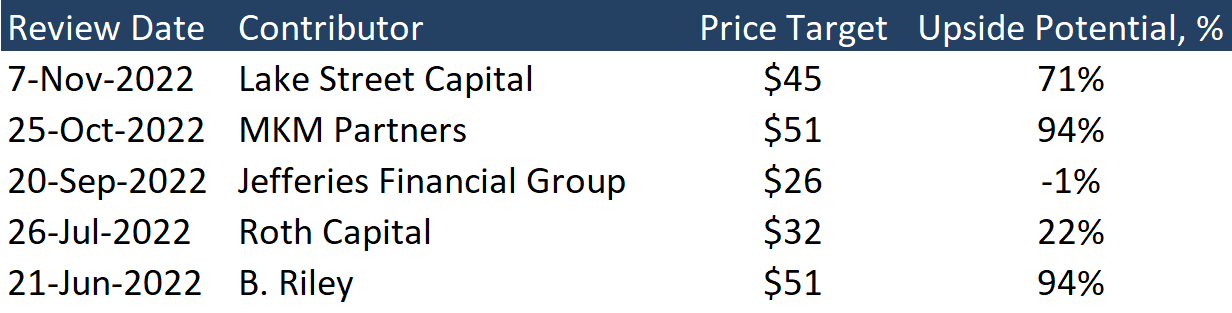

The minimum price target set by Jeffries Financial Group is $26 per share. MKM Partners and B. Riley, in turn, set a target price of $51 per share. According to the consensus, the fair value of the stock is $41 per share, which implies a 56% upside potential.

Key risks

- Should a negative macroeconomic scenario develop, we can expect to see increased pressure on both the company and its customers, resulting in lower overall revenues and business margins and a negative impact on the company's value.

- Lack of specific timing of spin-off: the company's separation could be delayed, potentially slowing down growth.