What's the idea?

- Viasat provides communication services on board aircraft, and also produces systems for the services’ implementation. According to forecasts, the market will grow at a compound annual growth rate (CAGR) of 15.9% in 2023–2030 to reach $21.03 billion by 2030. In addition, Viasat has contracts for the installation of communication systems on at least 1,600 airliners, in addition to 3,270 already served.

- The SatCom (Satellite Communication) market is expected to grow at a CAGR of 9.54% in 2023–2029 to reach $56.7 billion by the end of the forecast period.

- More than twofold quarter-on-quarter growth of the company's backlog in Q1 FY2024.

- The company's plan is to increase its satellite fleet by more than eightfold by the end of FY2025.

About Company

Viasat (VSAT) operates high-performance Ka-, L- and S-band satellites, through which the company provides broadband satellite communications services, aircraft and marine communications services, as well as products and solutions for receiving satellite communications on the ground. In addition, Viasat provides selected communications and cybersecurity solutions for the public sector in the US and other countries.

Why do we like Viasat Inc?

Reason 1. High potential of target markets

Viasat’s main business direction is providing communications products and services. Through the existing network of satellites, the company's customers can be connected to the global network both from hard-to-reach places where traditional communication cannot be maintained, and from within the coverage area of cellular operators.

One of the company’s key markets is the In-Flight Services market, represented by IFS systems, and W-IFE (Wireless In-Flight Entertainment). Viasat manufactures the systems for the aviation industry and installs them on aircraft, while providing further support through its own network of satellites.

For example, through W-IFE systems, airline passengers can access multimedia entertainment on board, and IFS systems allow in-flight Internet communication services that are not inferior in quality to those available on the ground.

Both markets are expected to show rapid growth in the coming years, as the post-coronavirus recovery of the aviation industry and the commissioning of new aircraft will become an additional driver.

According to Businesswire, the W-IFE systems market will grow at a CAGR of 17.3% in 2023–2030 and reach $6.0 billion by the end of the forecast period.

According to Fortune Business Insights, the IFS market in the same period will grow at a CAGR of 15.9% to reach $21.03 billion by 2030.

As of the end of Q1 FY 2024 (ended June 30), Viasat's IFS systems were installed and used on approximately 3,270 aircraft. Moreover, according to the current agreements, Viasat's IFS systems are going to be installed on about 1,600 more ships.

In 2022–2023, Viasat received several awards for its communications services. In particular, the company’s IFS systems received the following recognition:

- APEX Passenger Choice Award 2023 and 2022 for Best Wi-Fi (services for Delta Air Lines);

- APEX Regional Passenger Choice Award 2023 for Best Wi-Fi in the South Pacific (services for Qantas);

- APEX Regional Passenger Choice Award 2022 for Best Wi-Fi in Europe and North America (services for Finnair and Jetblue, respectively).

Since 2018, the company has been performing an 8-year fixed-price government contract providing in-flight communications services to senior US government officials and private jets, which proves the high quality of Viasat’s services.

The Viasat also provides broadband satellite services, which are carried out in two stages: a user connects to a public or personal terminal (manufactured and installed by the company), which communicates directly with a Viasat satellite.

In the US and Europe, this type of communication is used, for the most part, as an alternative to cellular communication. In Brazil and Mexico, as well as other countries where Viasat operates, satellite communications are provided on a prepaid basis, mainly in areas without cellular coverage.

Viasat satellite broadband services are also used by the crews of ships both when working with navigation systems and for obtaining personal access to the Internet.

According to the Fortune Business Insights’ forecast, the SatCom market will grow at a CAGR of 9.54% in 2023–2029 to reach $56.7 billion by the end of the forecast period.

All of the above mentioned Viasat services and products are provided to the US and other countries’ governments.

Thus, in addition to the rapid growth of target markets, Viasat has a large and reliable customer base including government agencies, which provides the company with a stable demand for its services.

Reason 2. Significant backlog growth in Q1 FY 2024

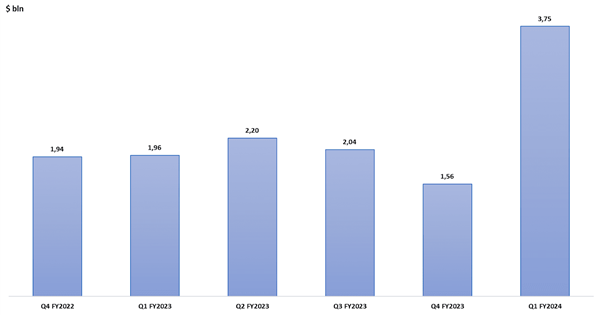

As noted earlier, Viasat not only provides communication services, but also manufactures products necessary for the services’ adjustment and maintenance. In addition, the company designs and develops satellite communications systems, their architecture, as well as semiconductors for application-specific integrated circuits (ASICs) and monolithic microwave integrated circuits (MMICs). Since most of the products are custom-made and developed over a long period of time, Viasat takes them into account as a funded backlog, which represents the volume of signed contracts, under which clients have committed to pay cash in the future. Viasat backlog also reflects future revenues from subscription agreements for the provision of fixed broadband satellite services. The chart below shows historical changes in the company's funded backlog.

Viasat backlog increase

In Q1 FY2024, Viasat's backlog significantly increased: by 140% to $3.75 billion. The growth occurred in all business segments, with the Satellite Services division’s backlog up more than fivefold quarter-on-quarter, mainly due to the purchase of Inmarsat (more below).

The backlog of the Government Systems segment (provides communication systems for the public sector and the military) also showed significant growth, more than twofold quarter on quarter, caused by an increase in orders for information security products and satellite communications solutions for governments.

Viasat estimates that revenue for about 50% of the backlog will be received over the next 12 months. Thus, due to the significant growth of backlog in Q1 FY2024, we expect higher growth in the company's revenue in the coming quarters.

Reason 3. Expansion of satellite fleet

In Q1 FY2024, Viasat operated 22 Ka-, L- and S-band commercial satellites, 16 of which were added to the company's fleet after the purchase of Inmarsat for $551 million in cash and $2.1 billion in shares. It is worth noting that the total cost of the deal was estimated at $8 billion, and Viasat, in addition to assets, received $6.2 billion of liabilities and $860 million of deferred revenue.

In addition to increasing the number of satellites under management, the acquisition of Inmarsat allowed Viasat to bolster its presence in the European market for IFS systems, as well as significantly expand its coverage network for the provision of broadband satellite communications services in the Americas and the EMEA region, including on ships.

According to forecasts, Inmarsat’s acquisition is expected to have a significant effect: by 2026, Viasat's revenue is seen to increase to ~ $7.67 billion from $ 2.63 billion in the calendar year 2022, which implies a more than threefold increase. The charts below show forecasts for Viasat's revenue and Adj. EBITDA for the coming years.

Viasat's revenue growth, taking into account the purchase of Inmarsat

Growth Adj. Viasat's EBITDA including purchase of Inmarsat

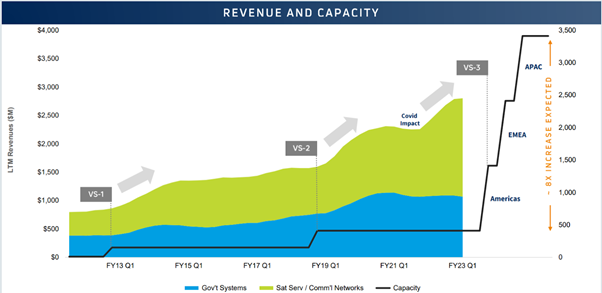

In addition to increasing its business scale through M&A, Viasat also grows organically by building up a fleet of satellites. Thus, in April 2023, the company launched its ViaSat Americas 3rd generation satellite, which was announced to have antenna problems in May (more below). This is the first satellite of this class to be launched by the company. In addition, Viasat is currently building 8 satellites, 5 of which are planned to launch before the end of FY2025. In particular, two more 3rd generation satellites — ViaSat EMEA and ViaSat APAC — are expected to launch within the next two years.

The combined power of three satellites — ViaSat Americas, ViaSat EMEA and ViaSat APAC — is expected to be about eightfold bigger than the power of the company's two older satellites, 1st and 2nd generations ViaSat. The graph below shows the correlation between the company’s revenue and its satellite capacity.

Dependence of ViaSat's revenue on the power of satellites

Thus, the satellite fleet expansion and the acquisition of Inmarsat open up significant prospects for Viasat's financial growth in the coming years.

Reason 4. Market overreaction to ViaSat-3 Americas problems

In the summer of 2023, it was reported that the ViaSat-3 Americas satellite, launched in April 2023, had antenna problems, which could significantly influence its performance. The problems occurred after the satellite was launched into orbit to prepare for commercial use.

According to Viasat, the antennas used on ViaSat-3 Americas were previously installed on other company’s satellites and never had any problems, so the latest problems could not be foreseen.

The company assured that the antenna anomaly will not affect the current communication coverage. Viasat is currently trying to fix the problem and also has insurance in case the device cannot be repaired. At the same time, other equipment of the satellite is operating normally.

On July 13, 2023, the day when the antenna failure news was released, Viasat stock price fell by 28.5% to $30.7 per share and is still near the level. We believe that the market reaction to the news was excessive, and the current stock price offers an excellent opportunity for investing in the company.

First, Viasat has insurance that can cover most of the costs in the event of an antenna failure. Secondly, these satellite elements are not produced by the company itself, but by a certain supplier. Accordingly, the failure constitutes a breach of contract and Viasat is likely to be entitled to seek compensation in court or pre-trial proceedings.

Thirdly, even if it is impossible to eliminate antenna defects on ViaSat-3 Americas, the company plans to launch two other 3rd generation satellites in the coming months, which can mitigate the negative effect of the antenna failure by the replacement of ViaSat-3 Americas. The company management сonfirmed it in a statement on the satellite malfunction.

It is also important to add that the company's satellite fleet is well diversified and is represented by more than 20 operating devices, and eight satellites under construction.

Thus, we believe that the negative effect of the ViaSat-3 Americas antennas failure is exaggerated and already priced in. Even if the problem cannot be resolved, it willl only affect the speed of company's strategy implementation rather than its current financial performance.

Financial performance

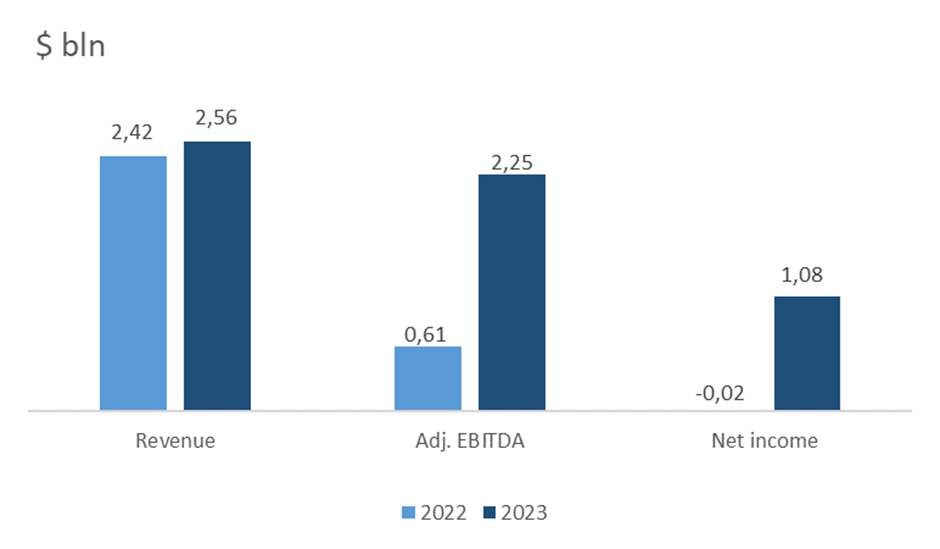

Viasat's fiscal year 2023 ended in March. Given this, the company’s financial results for 2023 can be summarized as follows:

- Revenue was $2.56 billion, up 5.75% from 2022.

- Adj. EBITDA increased from $611 million to $2.25 billion, but it is worth noting that this includes the sale of the Link-16 TDL subsidiary. Without the sale, adj. FY 2023 EBITDA was $583 million. EBITDA margin decreased from 25.28% to 22.82%.

- Net profit amounted to $1.08 billion against a loss of -$15.53 million a year earlier. Net margin increased from -0.64% to 42.44%.

Revenue grew due to increased demand for the company's services, as well as due to the payment of $62.5 million to Cisco as a result of the Acacia Communications dispute resolution. At the same time, a sharp increase in operating and net income is associated with the sale of a subsidiary in Q2 FY 2023 for $1.96 billion, which was reflected in the financial statements as a discounted transaction.

Dynamics of the company's financial indicators

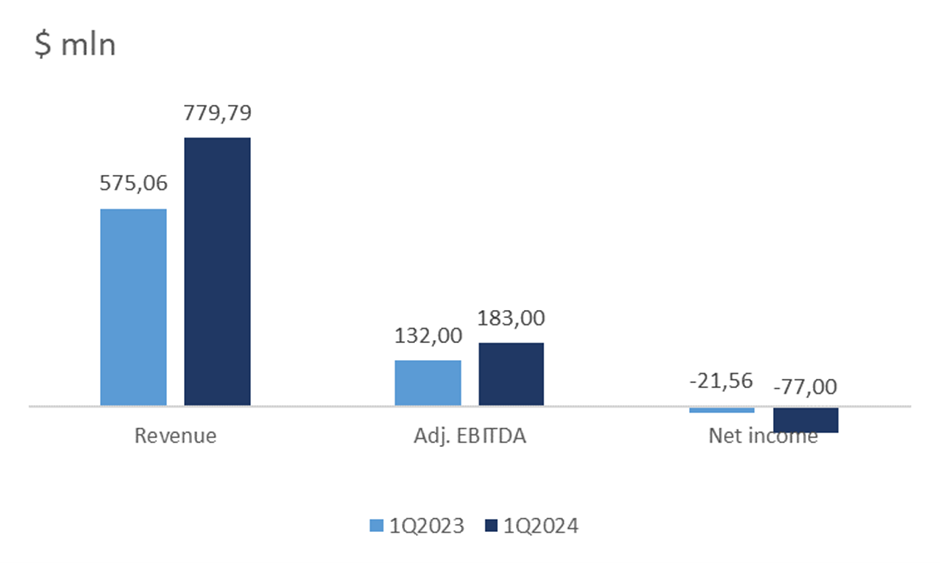

Viasat's financial results in Q1 FY2024 are presented below:

- Revenue grew by 35.60% YoY: from $575.06 million to $779.79 million.

- Adj. EBITDA increased from $132 million to $183 million. Adj. EBITDA margin increased from 22.95% to 23.47%.

- Net loss amounted to -$77.00 million against -$21.56 million a year earlier.

Dynamics of the company's financial results in 1Q 2023

In Q1, the company continued to show positive dynamics in revenue and operating profit from continuing operations, which indicates higher demand for the company's services. The deeper net loss is due to a significant increase in interest payments on loans taken for the acquisition of Inmarsat.

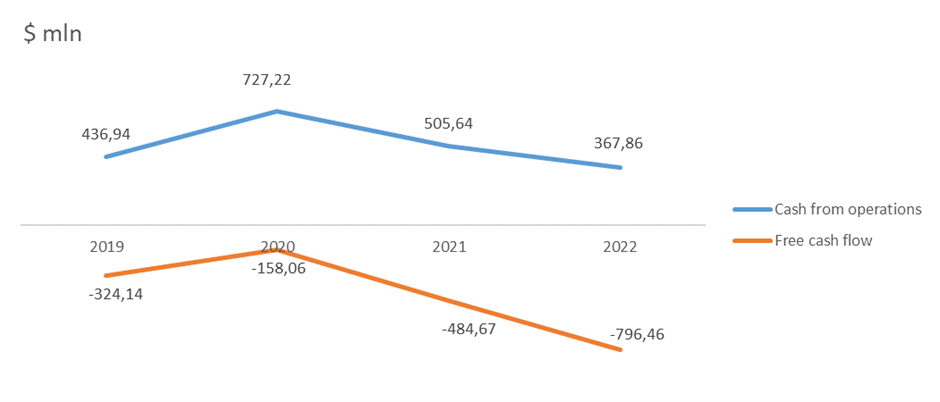

- In FY2023, operating cash flow decreased to $367.86 million from $505.64 million in 2022.

- Free cash flow decreased from -$484.67 million to -$796.46 million in 2022.

Operating and free cash flows declined primarily due to lower earnings from continuing operations in FY2023, as well as higher capital expenditures.

Company cash flow

Viasat has an increased debt load:

- Total debt is $7.28 billion.

- Cash equivalents account for $1.96 billion.

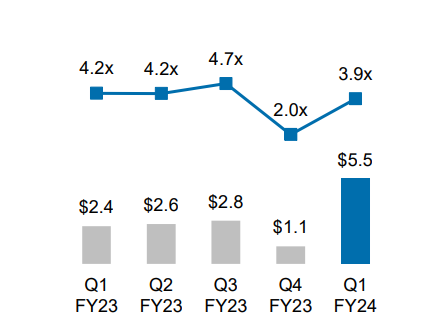

- Net debt is $5.5 billion, Net Debt/adj. EBITDA was 3.9x over the last 12 months.

Net debt & Net leverage ratio

This level of debt burden is elevated. It is worth noting that along with the acquisition of Inmarsat, the company consolidated its debt by $3.52 billion, which significantly increased the company’s debt burden. However, repayment is expected only at the end of 2026, which, in our opinion, partially offsets this risk.

Stock valuation

Viasat trades at a discount to the industry average: EV/Sales — 3.32x, EV/EBITDA — 4.00x, P/B — 0.62x. Viasat, like other companies in the industry, does not have a P/E multiple due to net loss, which we do not see as a relevant figure to the industry.

Comparable score

The average price target from Wall Street's top five investment banks is $49.6 per share. According to our consensus, the company is undervalued by industry average and historical multiples; the stock’s fair market value is $45.7, which implies a 59.8% upside potential.

Price targets of investment banks

Key risks

- Possible delay in the launch of the ViaSat-3 EMEA and ViaSat-3 APAC satellites, which have similar equipment to ViaSat-3 Americas. Viasat noted that it was looking into the issues with ViaSat-3 Americas that could affect the timing of launch for the other two models. At the same time, the satellite launch dates have not been violated.

- The discovery of new problems on the existing or upcoming satellites could have a negative impact on both the company’s financial plans and its stock price.

- Viasat supplies products and services to the public sector and is therefore exposed to risks associated with public contracting changes. Moreover, the US and other governments may terminate ViaSat services, which could adversely affect the company's revenue.

- High debt load. Consolidation of Inmarsat's debt has significantly increased the risks to Viasat's financial stability. If the company fails to achieve the planned synergies from the acquired firm, this may negatively affect its financial position.