What's the idea?

The rapid collapse of Silicon Valley Bank and Signature Bank once again proved the destructive power of the bank panic run. The financial system’s stability has become a major concern for many investors. A high degree of uncertainty instantly affected the market value of bank stocks. Amid the increased risks of confidence runs and liquidity shortage, the SPDR S&P Regional Banking exchange-traded fund, which holds the stocks of 140 US regional banks, lost more than 26% of its market value. The Invesco KBW Bank's exchange-traded fund, focused primarily on the large-cap financial stocks, such as JPMorgan Chase, Citigroup, Wells Fargo and Bank of America, lost more than 23% of its market capitalization.

However, apart from banks with heavy accumulated losses exceeding their equity capital, the market underperformers also included first-class financial stocks with healthy safety margins. We have selected bank with strong competitive positions, allowing them to successfully navigate headwinds and provide high returns to their investors: Truist Financial Corporation (TFC).

Why do we like Truist Financial Corp?

Truist Financial is a major regional player. The volume of assets on the bank's balance sheet exceeds $555 billion, which makes it the country's 7th largest bank by assets. Amid growing uncertainty, depositors are likely to seek shifting some of their savings to the country's largest financial institutions. At the beginning of the banking panic, the thesis could only apply to financial giants such as JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup. However, today the list of the most trustworthy companies can also include some regional banks, including Truist Financial.

In mid-March, one of the panic run victims, First Republic Bank, was reported to have received $30 billion in deposits from 11 largest financial companies, including Truist Financial. In addition to making an important contribution to the sustainability of the country’s financial system, the move has also significantly increased the banks’ credibility.

Like Fifth Third Bancorp described in a similar investment idea, Truist Financial has a strong deposit base. Only 46% of all company deposits are uninsured, which is significantly below the industry average. Although the held-to-maturity assets account for a significant 44.6% share of the company's securities portfolio, the accumulated deficit in the liabilities side of the balance sheet suggests a healthy margin of safety. At the end of the last reporting period, the bank’s accumulated deficit stood at $13.6 billion with equity amounting to $60.5 billion. Even if we assume that the actual deficit is twice as large (due to the revaluation of held-to-maturity assets), it still amounts to less than half of equity.

TFC’s Equity and accumulated deficit

Truist Financial stands out by its loan portfolio quality. Most of the loans on the bank's balance sheet relate to the manufacturing and real estate sectors. At the end of the last reporting period, the allowance for credit losses (ACL) stood at 1.43% against 1.62% a year earlier. Net charge-offs increased from 0.24% to 0.27%, but the figure is still lower than 0.36% in 2020.

Truist Financial provides its shareholders with a significant dividend yield. The company distributes $0.52 per share for quarterly dividends, which equates to $2.08 per share per year. Thus, the forward dividend yield makes up about 6%. Truist pays out half of its net income in dividends, which means that the coverage ratio provides a sufficient margin of safety. However, the company may revise its payout policy amid headwinds in the banking industry.

Truist Financial's 2022 results can be summarized as follows:

- Interest Income was $16.64 billion, up 20.8% from a year earlier.

- Net Interest Income stood at $14.32 billion compared to $13.01 billion a year earlier.

- Net Income fell from $6.03 billion to $5.93 billion due to higher loan loss provisions.

The company’s financial performance

- In 2022, the return on assets (ROA) was 1.07% against 1.11% a year earlier.

- The return on equity (ROE) amounted to 9.79% against 8.71% a year earlier.

TFC’s profitability

Truist Financial is a well-capitalized bank. The bank’s capital adequacy ratio (CET1) is 10.6%, above the minimal regulatory requirement of 6.50%. Tier 1 capital accounts for 10.6% against the regulatory requirement of 8.00%. The total capital ratio is 12.1% versus 10.00%, and the leverage ratio is 8.5% versus 5.00%.

TFC’s regulatory capital ratios

Truist Financial is trading at the following multiples: P/E (TTM) — 7.70x, FWD P/E — 7.05x, and P/B — 0.84x. In other words, the bank is trading at a discount not only to larger competitors like PNC Financial and U.S. Bancorp, but also to smaller firms like M&T Bank and Fifth Third.

TFC’s comparable valuation

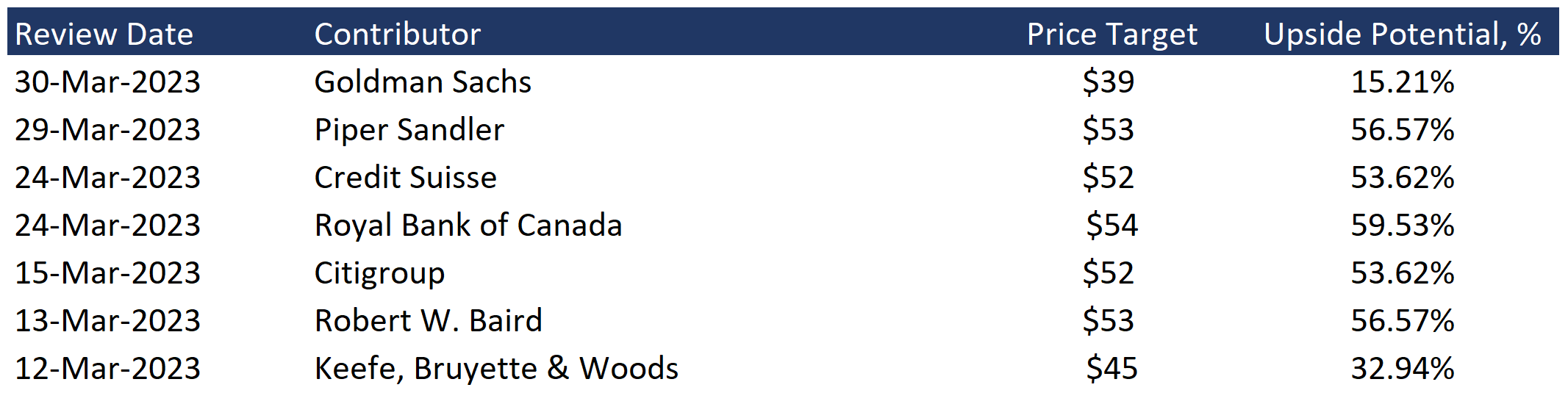

The minimum price target from investment banks set by Goldman Sachs is $39 per share. However, Royal Bank of Canada estimates TFC at $54 per share. According to the Wall Street consensus estimate, the stock’s fair market value is $51, implying a 59.12% upside potential.

Price targets of investment banks

Key risks

- Although Truist Financial is highly resilient, in the event of a significant outflow of deposits, the bank could face a squeeze in its net interest margin.

- It must be taken into account that investments in the banking industry in the current environment carry high risks. The deterioration of the industry situation and the appearance of signs of another panic run could lead to significant losses for the shareholders of financial institutions.