What's the idea?

- The tourism industry recovery, supported by the low base effect, pent-up demand and China’s removal of COVID restrictions, will help the company to accelerate growth.

- The promising Viator segment will support the company's results.

- High level of financial stability will allow the company to invest in growth in 2023.

About Company

TripAdvisor, Inc. (TRIP) is an online travel agency that owns and manages a portfolio of online travel brands. The company's business is divided into three main segments:

- Tripadvisor Core — a global online platform for travelers. It allows users to discover, generate and share content about interesting places via ratings and reviews. By the end of 2022, Tripadvisor had over 1 billion user ratings and reviews about nearly 8 million places.

- Viator — online travel agency that allows clients to book various experiences in memorable places.

- TheFork — an online search and reservation platform for over 55,000 restaurants in 12 countries with over 20 million reviews as of the end of 2022.

Why do we like TripAdvisor Inc.?

Reason 1. Travel industry recovery continues

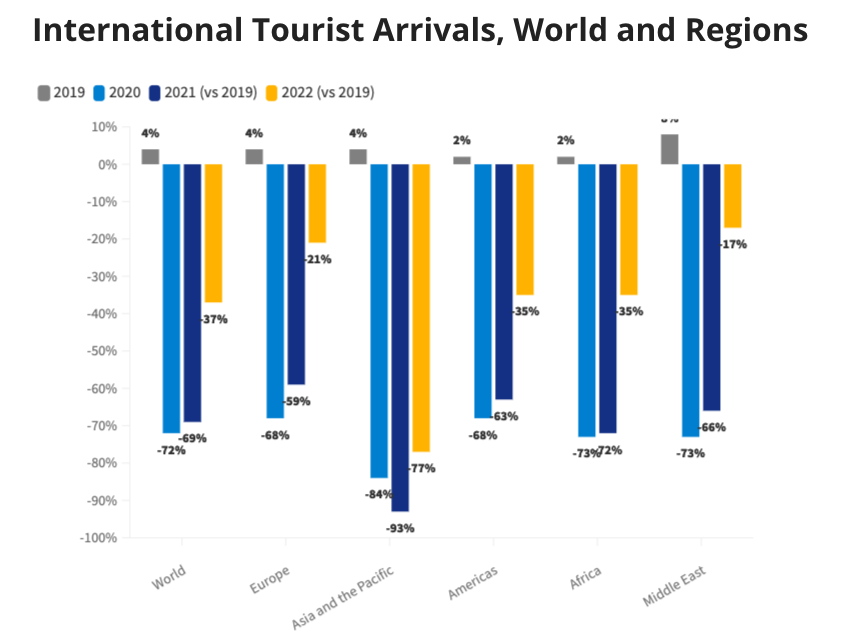

Tourism industry was at the forefront of those affected by epidemiological restrictions due to the pandemic. The damage was so significant that even despite macroeconomic challenges in 2022, the number of international trips increased by 172% year-over-year in the January-July period.

However, even with such high growth rates, the industry has still to recover to the 2019 levels. According to the UN World Tourism Organization, the 2022 volume of international travels reached 63% of the 2019 levels, and in 2023 the industry is expected to recover to 80%-95% of the 2019 numbers.

A major recovery driver could be the Asia-Pacific region, where the level of international tourism is still 77% below 2019.

The gradual removal of Covid restrictions in China will be another tailwind. Thus, Hong Kong has canceled the mask regime, which had been in effect for more than 2.5 years, from March 1. The China Tourism Academy predicts that in 2023, the country’s domestic travel will recover to 76% of the 2019 level, showing a 73% year-over-year growth. Outbound tourism is expected to more than double.

We expect a positive trend in the US travel industry, as dollar strength relative to other currencies should also have a positive impact on Americans' interest in international travel. Due to the difference in exchange rates the cost of travel for US citizens is 10%-20% lower today than a year earlier.

Despite the industry’s incomplete recovery, in 2022 TripAdvisor earned $1.5 billion, which was 96% of the 2019 level, while exceeding the 2019 number by 6% in Q4 2022. This shows that TripAdvisor is recovering faster than the industry and has the potential to outpace the industry in 2023.

Reason 2. Viator Potential

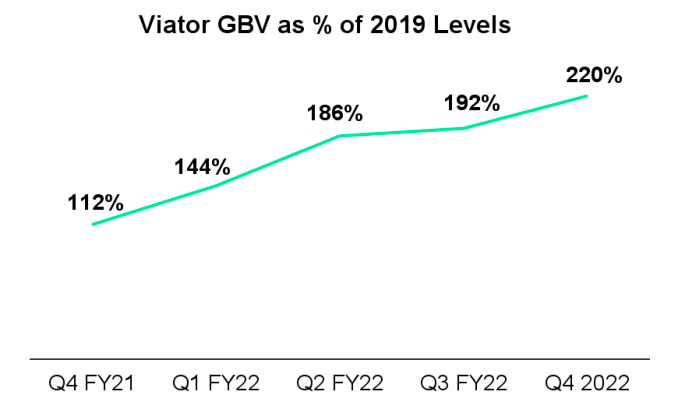

Booking service Viator showed strong growth in 2022: the segment’s revenue (first chart below) increased by 168% year-over-year and amounted to a third of TripAdvisor's total revenue. At the same time, GBV (gross booking value, the cost of booking minus cancellations and changes; second chart below) grew by ~ 95% year-over-year.

During a conference call with investors about Q3 results, the company’s management noted that despite the current market state, Viator will focus on seizing market opportunities. This announcement is significant as TripAdvisor announced in a 2021 Shareholder Letter that the company was evaluating holding a sub-IPO to sell a minority stake in Viator in the market. The company said that it has submitted a confidential draft registration of S-1 statements regarding Viator's initial public offering in the U.S. Securities and Exchange Commission. The market in 2022 was indeed not in the best condition to implement such a plan. However, in our opinion, if the economy recovers in 2023, the company may return to this plan and implement the original idea on more favorable conditions.

It should be noted that if the company does not proceed with the IPO plan, this will not be a negative factor. Viator will continue to have a positive impact on TripAdvisor's financial results thanks to the excellent business performance of the subsidiary, which is not only increasing revenue, but also increasing its share in the overall company revenue. The adj. EBITDA dynamics suggests that the segment has all chances to become profitable in 2023 (chart below).

We believe the Viator segment holds great potential to add value to TripAdvisor's business and will boost the company's stock price this year.

Financial results

TripAdvisor's financial performance in 2022:

Revenue: up from $0.90 billion to $1.49 billion

Operating profit: up from $-131 million to $101 million:

in terms of operating margin, growth from -14.5% to 6.8%, mainly due to a decrease in SG&A costs from 94.0% to 78.4%

Net income: up from $-148 million to $20:

in terms of net margin, an increase from -16.4% to 1.3%

Operating cash flow: up from $108.0 million to $400.0 million, due to increased profitability and positive changes in working capital

Free cash flow: up from $54.0 million to $344.0 million

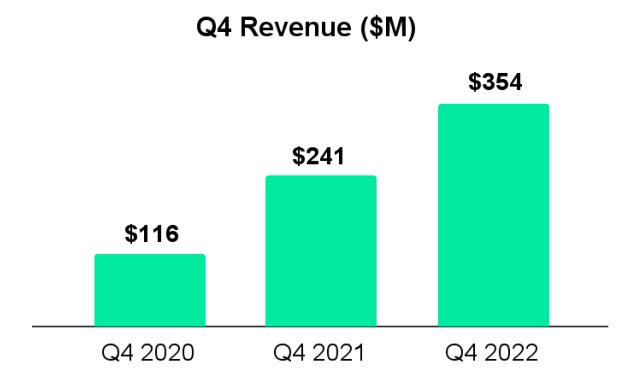

The company’s results for the most recent reporting period:

Revenue: up from $241 million to $354 million

Operating profit: up from $-28 million to $-13 million:

in terms of operating margin, growth from -11.6% to -3.6%, due to a decrease in SG&A costs from 92.5% to 85.6%

Net income: up from $-29 million to $-3 million:

in terms of net margin, growth from -12.0% to -0.8%

Operating cash flow: down from $65 million to $-40 million, mainly due to negative changes in accounts payable

Free cash flow: down from $51 million to $-55 million

TripAdvisor performed well both in the whole year and in Q4 of 2022. The loss in the last quarter, in our opinion, was caused by the seasonal decline in tourist activity. In 2023, we expect further improvement in the company's financial performance, which will positively affect the company's stock price.

Cash and cash equivalents: $1.02 billion

Net debt: $-121 million

Good level of cash and cash equivalents on the balance sheet, coupled with negative net debt, demonstrates TripAdvisor's strong financial stability and leaves space for management to invest in further business growth.

Evaluation

In terms of trading multiples, TripAdvisor is underperforming its peers across all indicators except for EV/EBITDA (which is due to a negative multiple of one competitor) and P/E.

High level of the second multiplier is mainly due to the fact that the company only recently managed to become profitable after challenges related to the pandemic (chart below). The company's Forward PE is currently valued at 15.87x. We expect a decrease in the PE level by the end of 2023.

Ratings of other investment houses

According to Refinitiv, since the beginning of the year, TripAdvisor Inc. got 14 recommendations with a target price, of which two are Strong Buy, three Buy, five Hold, two Sell and two Strong sell. The average recommendation price is $26.43, which implies a 40,51% upside potential.

Our estimate

If we evaluate TripAdvisor in terms of the average trading multiples over the past five years and compare with the current values, accepting weights for them in accordance with the illustration below, we find that at the current price of $21.7 per share, there is still upside potential of 40.51% to $33.3 per share.

Key risks

- The economic situation is still uncertain, so in case of a negative macroeconomic development, the company's growth rate can slow down.

- In the event of new COVID outbreak and return of restrictions in China, business growth may also slow down.

- The company may abandon Viator's IPO plans. However, in any case the business should have a positive impact on the company's financial results and stock price.