What's the idea?

Integrating technology into all corporate operations provides significant growth potential for the digital customer experience management industry. Through a series of strategic acquisitions, TELUS has entered the prominent and promising markets of content moderation and data annotation for artificial intelligence. Unlike most industry players, TELUS offers its customers complete solutions, giving them a significant competitive advantage. We expect the company's future M&A deals to be predominantly complementary rather than transformational. TELUS trades at a discount to the industry average. According to Wall Street consensus, the stock has more than 60% upside potential.

About Company

TELUS International (TIXT) is a provider of digital customer experience services. The company develops, creates and supplies solutions to technology and telecommunications companies, e-commerce enterprises, banks, insurance and fintech companies. TELUS was formed as a spin-off from telecommunications company TELUS Corp. in 2021.

Why do we like TELUS International?

Reason 1. Industry opportunity

Digital transformation is the main driver of all the company's target markets. According to Straits Research, the global digital transformation market was valued at $400.34 billion in 2021 and is expected to reach $2.20 trillion by 2030, implying a compound annual growth rate (CAGR) of 22.5%.

Expected market dynamics for digital transformation

Technology integration into all corporate operations and functional areas provides significant growth potential for the Digital Customer Experience Management (DCEM) industry. The DCEM market is expected to grow at a compound annual growth rate of 18.1% through 2030, reaching $38.98 billion at the end of the forecast period.

Expected DCEM market dynamics

Through the acquisitions of CCC and Lionbridge AI, TELUS has entered the large and promising markets of content moderation and data annotation for artificial intelligence (AI).

Due to the proliferation of misinformation on social media, there has been a steady increase in demand for content moderation. A telling example is a scandal surrounding Twitter over a possible moderation policy change. Typically, companies like Twitter and Facebook do not moderate content themselves but rather outsource this task to firms like TELUS. Allied Market Research estimates that this market will grow at a compound annual growth rate of 12.2% until 2031, when it reaches $26.3 billion.

AI development depends on the quality of the data on which machine learning is based. For data to be valuable, it must be tagged (annotated) by humans. TELUS is one of the leaders in this market. The data annotation market for AI is expected to grow at a compound annual growth rate of 26.6% to reach $5.3 billion by 2030.

Reason 2. Strong competitive positioning

TELUS provides three categories of services: solution design (Design), implementation (Build) and delivery (Deliver). If a company is experiencing problems with the customer experience, TELUS can identify the source of the issues and develop a solution. Once the problem has been identified, the client can then engage TELUS to implement the earlier proposed solution (e.g. launch a website). TELUS can then provide support for the implemented solution (e.g. maintain the website).

Thus, unlike most industry players, the company can provide its clients with comprehensive solutions that consider their needs at all stages and allow TELUS to consider changing trends as the firm evolves. The ability to provide complex solutions makes the company attractive to large enterprises that prefer to deal with a single supplier capable of offering a "package deal" and ensuring business continuity. As such, TELUS has a significant advantage over its competitors.

Reason 3. Exemplary M&A deals

What sets TELUS apart is its enviable track record in mergers and acquisitions. The company was born by acquiring a small call centre in the Philippines with 1,500 employees, but it has grown into an industry giant with more than 70,000 employees through effective acquisitions. Through M&A deals, TELUS has entered the IT consulting, computer vision technology, data annotation for lidar systems, and the aforementioned markets of content moderation and data annotation for AI.

TELUS development history

During the Q3 2022 earnings conference call, management noted that thoughtful M&A deals would remain a key part of the company's long-term growth model. A year earlier, CFO Vanessa Kanu emphasised that future acquisitions would increase revenues and improve margins. We expect future M&A deals to be largely complementary rather than transformational. We could see new deals already in the short to medium term, as the company has a relatively low debt burden, a positive liquid asset balance sheet and growing cash flow (see below for details).

Given TELUS' deep expertise in the M&A market, we believe it is prudent to view the extensional development model as an advantage for the company and a potential driver for sustainable growth in the long term.

Financial indicators

The company's results for the past 12 months can be summarised as follows

- TTM's revenue was $2.44 billion, up 11.1% from 2021.

- Gross profit increased from $1.76 billion to $1.97 billion. Gross margin increased from 80.31% to 80.76%.

- Operating profit increased from $185 million to $286 million. The operating margin was 11.73% compared to 8.43% for the year.

- Net profit was $185 million compared to $78 million for the year. Net profit margin increased from 3.56% to 7.59%.

Company margin dynamics

Company margin dynamics

TELUS, like any IT services company, is a labour-intensive business. Employee salaries and bonuses account for more than half of the company's expenses, limiting operating leverage growth. Without acquisitions of firms capable of delivering synergies or with higher margins, TELUS' margins are likely to remain in the high single/low double digits.

The financial results for the 33rd quarter of 2022 are as follows

- Revenue rose 10.6% year on year, from $556 million to $615 million.

- Gross profit increased by 13.0% year-on-year: from $446 million to $504 million. Gross margin increased by 1.7 percentage points: from 80.22% to 81.95%.

- Operating profit was $84 million compared to $47 million a year earlier. The operating margin increased from 8.45% to 13.66%.

- Net profit was $59 million compared to $23 million a year earlier. Net margin increased from 4.14% to 9.59%.

Trends in the company's financial results

TTM operating cash flow stood at $401 million for the latest reporting period, compared to $282 million for the entire year. Free cash flow to equity increased from $181 million to $293 million. The increase was driven by higher net income.

Company cash flow

TELUS has a strong balance sheet: total debt is $986 million, cash equivalents and short-term investments account for $143 million, and net debt is $843 million, which is 1.5 times TTM EBITDA (Net debt/EBITDA — 1.49x).

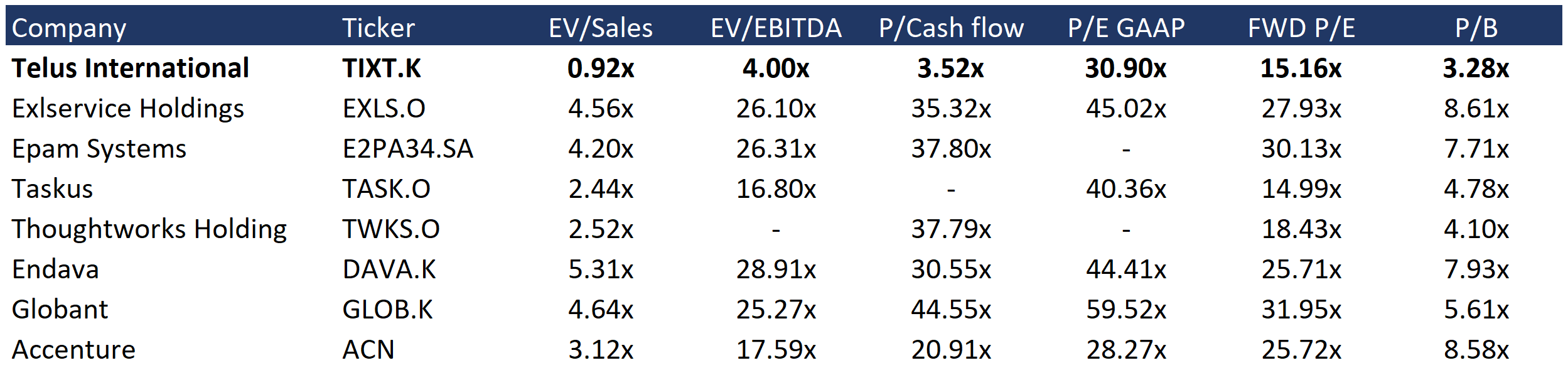

Evaluation

TELUS trades at a discount to the industry average: EV/Sales — 0.92x, EV/EBITDA — 4.00x, P/Cash flow — 3.52x, P/E — 30.90x, FWD P/E — 15.16x, P/B — 2.68x.

Comparable estimate

The minimum price target from investment banks set by Scotiabank is $26 per share. CIBC Capital, on the other hand, values TIXT at $36.5 per share. By consensus, the fair market value of the stock is $30 apiece, suggesting a 41.3% upside potential.

Price targets of investment banks

Key risks

TELUS is characterised by a high concentration of revenues — the 10 largest customers account for around 60% of revenues. The loss of one of these customers could significantly impact the company's financial performance.

A deteriorating macroeconomic environment could reduce spending on digital transformation, which is likely to affect demand for TELUS services and lead to a deterioration in the company's financial performance.

A significant concentration on mergers and acquisitions creates risks to shareholder value. There is a possibility that TELUS will overpay for a particular business or that the fundamental qualities of the acquired companies will prove to be worse than initially estimated.