What's the idea?

Savers Value Village Inc. is a second-hand apparel and accessories retailer. It is the largest for-profit thrift operator in the US and Canada based on number of stores, with a total of 326 stores in the US, Canada and Australia. Thrift stores is a sector of the broader second-hand market that includes traditional options such as Goodwill, Salvation Army, and yard sales.

The US second-hand apparel market grew 10.3% in 2023 and is forecast to reach $73 billion by 2028, with an average annual growth of 11.2% in 2023–2028. However, many resale and thrift companies struggle to stay afloat since turning a profit in the pre-owned clothing business is challenging.

As a thrift operator, SVV conducts its business through three main operating stages: supply and processing, retail, and wholesale trade. Over the past several years, the company’s management has built a powerful, vertically integrated business model, with a customer base of 5.5 million of active members enrolled in the US and Canadian loyalty programs.

SVV stores offer a wide selection of quality items across clothing, home goods, books and other items, with an average unit retail price (AUR) of approximately $5. In 2023, more than 35,000 items were merchandised per store every week.

SVV’s growth strategy encompasses three key components: organic expansion of the store base, consistent comparable store sales growth, and inorganic growth opportunities through M&A deals. The recently updated 2024 outlook implies opening 29 new stores (+8.9% YoY), revenue of $1.57–$1.59 billion (+5.3% YoY), and net income of $85–$92 million (+65.7% YoY).

About Company

Savers Value Village Inc. (SVV) is a second-hand apparel and accessories retailer. It is the largest for-profit thrift operator in the US and Canada based on number of stores, with a total of 326 stores in the US, Canada and Australia. The stores operate under the Savers, Value Village, Value Village Boutique, Village des Valeurs, Unique and 2nd Ave brands. SVV stores offer a wide selection of quality goods across clothing, home goods, books and other items. The company was founded in 2019 and is headquartered in Bellevue, the US.

Why do we like Savers Value Village Inc?

Reason 1. Second-hand retail economics is challenging, but market offers significant opportunities

Savers Value Village Inc. (SVV) is a second-hand apparel and accessories retailer. It is the largest for-profit thrift operator in the US and Canada based on number of stores, with a total of 326 stores in the US, Canada and Australia (as of December 30, 2023). The stores operate under the Savers, Value Village, Value Village Boutique, Village des Valeurs, Unique and 2nd Ave brands. Thrift stores is a sector of the broader second-hand market that includes traditional options such as Goodwill, Salvation Army, and yard sales. These second-hand options are primarily, but not exclusively, offline.

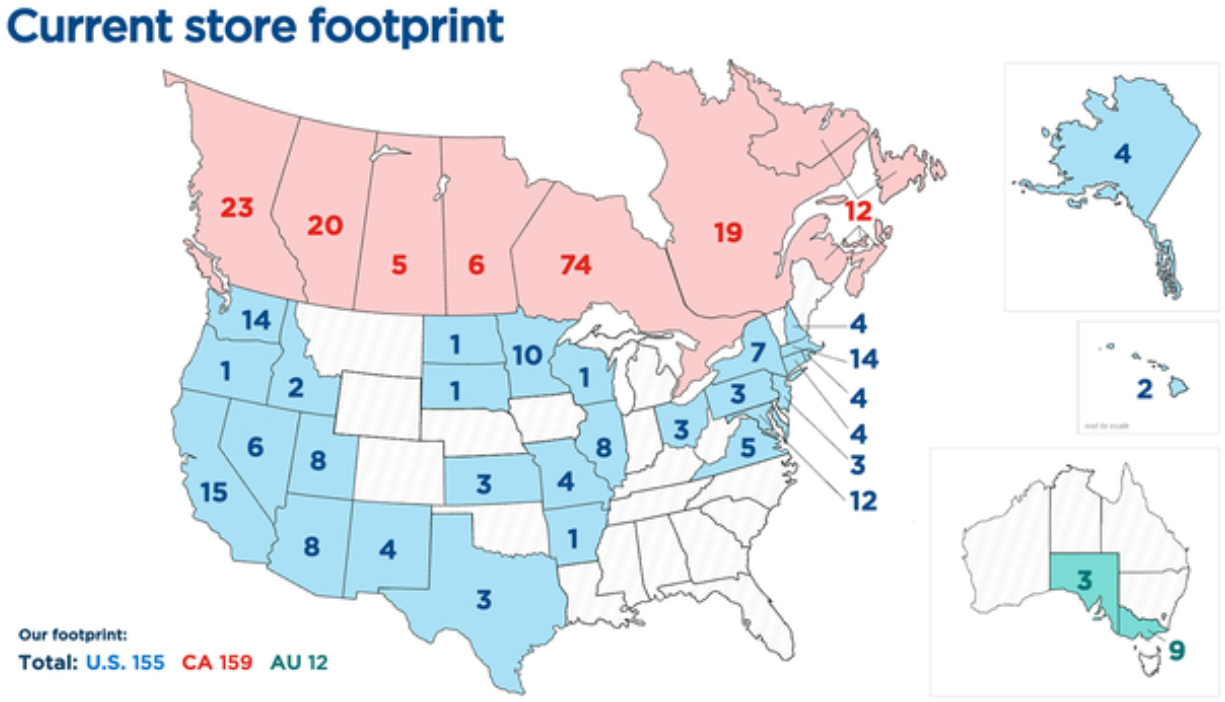

SVV’s store footprint as of December 30, 2023

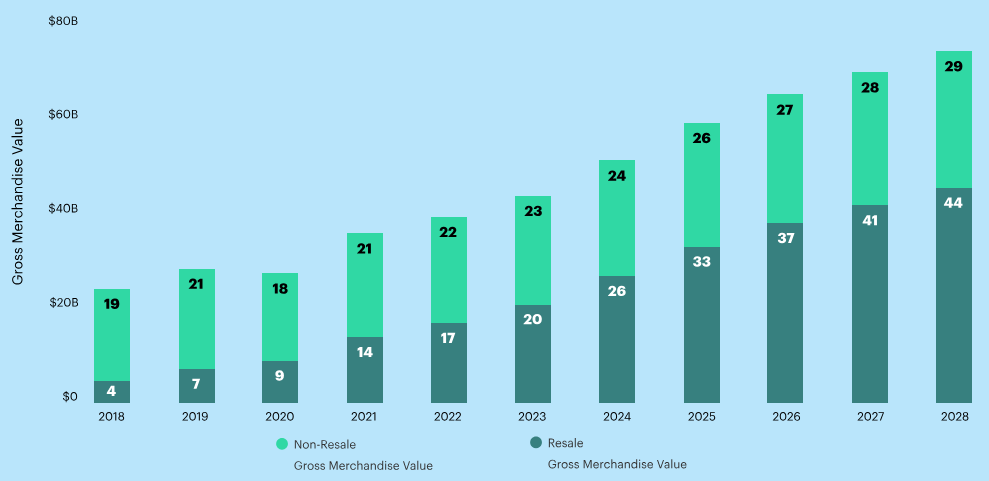

SVV operates in a large, fragmented, and rapidly growing second-hand goods market, which is part of a broader retail market. According to a ThredUp study, the global second-hand clothing market reached $197 billion in 2023 and is expected to grow to $350 billion by 2028. SVV's key market - the second-hand clothing market in the United States - grew by 10.3% in 2023, with its growth rate seven times higher than the growth rate of the retail clothing market overall. According to forecasts, by 2028, the volume of the second-hand clothing market in the United States will reach $73 billion, corresponding to a cumulative average annual growth rate (CAGR) of 11.2% from 2023 to 2028. In 2022, the thrift segment accounted for approximately 56% of the total second-hand market in the United States.

The resale segment is experiencing even more rapid expansion. In 2023, it grew 15 times faster than the broader retail clothing sector, and is projected to more than double by 2028, growing at a CAGR of 17%, which is 6.4 times faster than the broader retail clothing market. A significant driver of this growth is the online resale market. In 2023, online resale accelerated with a growth rate of 23%, 220 basis points faster than in 2022. By 2025, it is projected to account for half of all second-hand spending. Furthermore, over the next five years, online resale is expected to more than double, reaching $40 billion by 2028 with a CAGR of 17%.

Volume of the secondhand clothing market in the US

The current growth of the second-hand clothing market in the US is largely driven by economic uncertainty, which prompts consumers to be more frugal. The GlobalData Consumer Resale Survey, which surveyed 3,654 US residents, showed that in 2023, 52% of consumers bought clothes in second-hand stores. This trend is even more pronounced among Generation Z and millennials: 65% of them buy second-hand clothes compared to 60% in 2022. Furthermore, over the past year, consumers have spent almost half of their clothing budget on second-hand items. Additionally, 55% of consumers indicated that if the economy does not improve in 2024, the share of second-hand in the total clothing budget will increase even more.

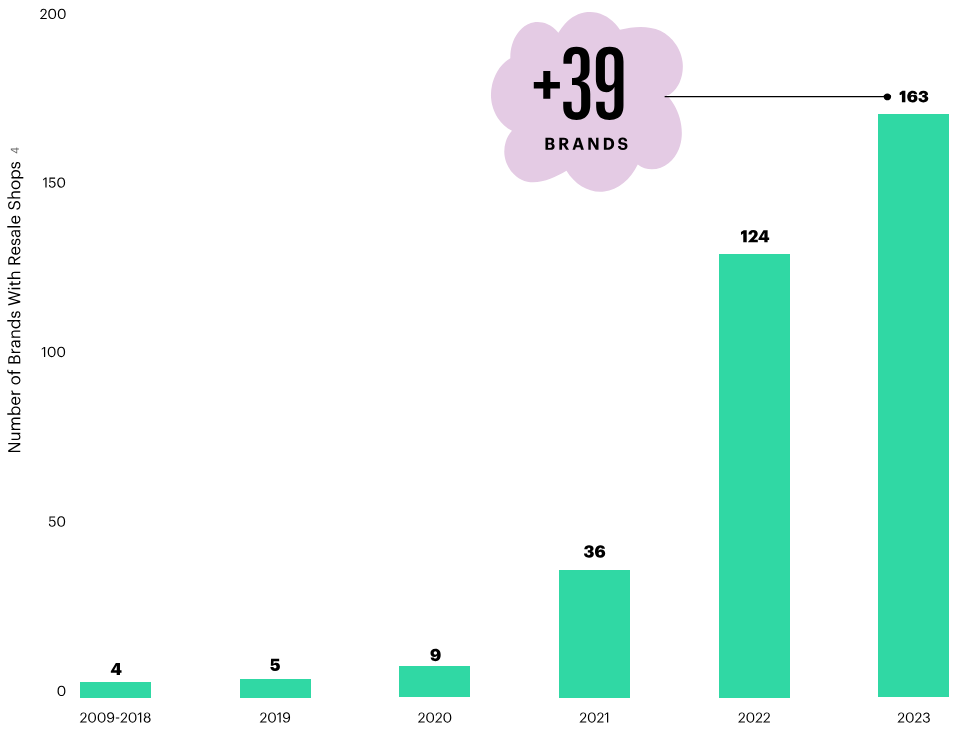

The growing popularity of second-hand is also due to other factors: the desire to find profitable and unique offers, afford more expensive brands, and environmental considerations. Noticing these trends, many clothing brands are entering the resale market. Thus, the number of brands that have opened second-hand stores, increased from nine in 2020 to 163 in 2023. This list includes such well-known brands as Zara, Patagonia, Lululemon Athletica, The North Face, Abercrombie & Fitch, Dr. Martens and Converse. This trend is likely to persist as 74% of companies that have not yet developed this direction are either considering or planning to enter the second-hand market in the future, while in 2022 the share of such companies was 69%.

Number of brands with second-hand stores

Thus, the second-hand clothing market opens up significant opportunities for companies. However, there is a serious problem: making the second-hand clothing business profitable is very difficult. Even the largest players are still loss-making. For example, American companies ThredUp and The RealReal do not generate net profit, causing their share prices to fall below the IPO level. Lithuanian fashion resale startup Vinted has just reported its first profitable year with net earnings of €17.8 million compared to a loss of €20 million in 2022. For comparison, its British competitor Depop recorded a loss of 59 million pounds sterling in 2023.

All companies in the second-hand clothing market are facing financial problems. In the UK, companies are ceasing operations due to high labor costs and a decrease in the quality of the clothes they receive. Moreover, the emergence of mass-market segment brands has led to a sharp increase in clothing production worldwide, as a result of which consumers throw away clothes after just a few uses. A 2023 study showed that a major Swedish charity has to pay to recycle 70% of donated clothes because the quality is too low for selling or exporting.

In addition, the processing of second-hand goods is labor-intensive and costly. In some cases, the cost of labor can make second-hand clothing more expensive than new items of similar quality. In a recent article, The Telegraph called shopping in thrift stores in the UK "rightful robbery", because a used Primark sweater cost more than a new one. Therefore, to improve their business models, some companies are changing their acquisition schemes of used clothing. For example, ThredUp now charges consumers and brands a fee for recycling old clothing.

Thus, it is expected that in the coming years the second-hand clothing market will grow at double-digit rates. However, companies need to implement innovations to build a sustainable and efficient business in a competitive market. Some experts advocate for funding capital-intensive sorting and recycling infrastructure to reduce labor costs, similar to subsidies provided for other "green" initiatives.

Reason 2. Vertically integrated business model and competitive advantages

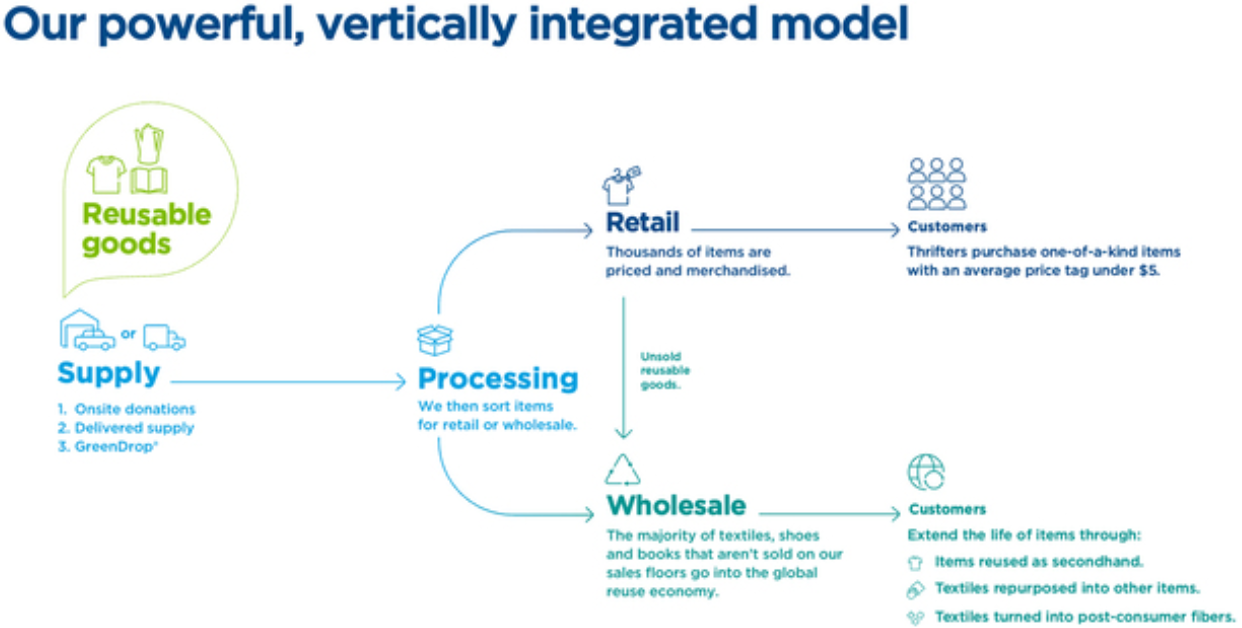

SVV's operational business includes three main stages: procurement and processing, retail trade and wholesale sales. To effectively integrate these complex components, the company has invested significant resources in developing a strong vertically integrated business model.

Diagram of SVV's vertically integrated model

Procurement and processing. SVV acquires second-hand goods donated by non-profit partners (NPPs), using three different purchasing models:

- Delivery of goods donated by non-profit partners to SVV stores or its sorting centers (Centralized Processing Centers, CPCs).

- On-Site Donations (OSDs), which are donations made by non-profit partners at community centers located in SVV stores.

- GreenDrop stations, which are mobile donation points located in convenient and bustling locations near SVV stores.

SVV purchases used textiles, footwear, accessories, dishes, books, and other goods from non-commercial partners. The average annual growth rate of in-store donations in comparable stores has averaged 3.5% from 2019 to 2023, resulting in an increase in the proportion of in-store donations in the total volume of sorted goods (in pounds) from 53.0% to 65.2% for the same period.

Most of the company's retail stores have facilities for sorting received goods, which are then put on sale in the same stores. To improve efficiency, SVV is moving to sort at warehouses, stores with excess capacity and special sorting centers. Currently, the company is betting on the development of sorting centers. A sorting center is a semi-automatic sorting enterprise using conveyor belts, robotics, sensors, and other technologies for the mechanization of sorting clothes, accessories, and shoes. As of December 30, 2023, SVV had five such enterprises, and during 2023 they sorted 984 million pounds of goods compared to 985 million pounds in 2022 and 860 million pounds in 2021.

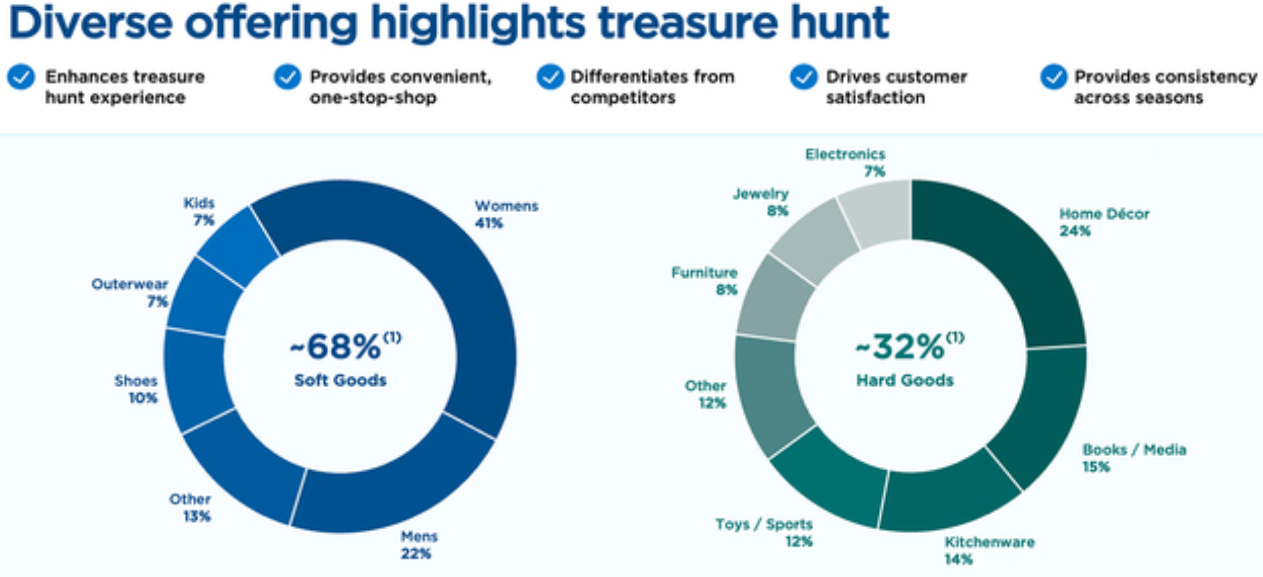

Retail trade. SVV sells most of its goods to retail and wholesale buyers. The company's stores offer a wide range of quality goods: clothing, home goods, books, and other items. The average retail price per unit (Average Unit Retail, AUR) is about $5. Throughout 2023, each store sold over 35 thousand goods every week. The stores also regularly update their inventory, with stock turnover occurring approximately 17 times a year, providing customers with a vast, constantly changing selection at competitive prices.

Range of goods in SVV stores

In addition, SVV offers customers an environment where they are maximally involved in the shopping process and in the search for rare items. This is a strong driver of customer base growth: as of March 30, 2024, the total number of active loyalty program users in the US and Canada reached 5.5 million, increasing by 14.6% from 4.8 million in December 2022. As a result, the number of active users made up 70.3% of the total volume of purchases in the company's stores in 2023. Throughout 2023, these customers purchased 274 million different items in SVV stores.

Wholesale sales. SVV displays about 50% of all received goods in its stores, approximately 50% of which are sold to retail customers. Most of the unsold goods are sold to wholesale customers - mainly recycling companies and small business owners. Textile products that are not suitable for reuse are recycled into other textile products (such as rags) and various materials (such as insulation materials and carpet coverings).

This may seem like a standard business model for second-hand store operators, but SVV has several competitive advantages that distinguish it from traditional retail companies:

- SVV receives goods from non-commercial partners, with contracts lasting from one to three years. The company's collaboration with its ten largest partners has been ongoing for over 27 years. Over the past five years, SVV has paid partners over $530 million for used goods.

- SVV offers high-quality goods with large discounts and creates an environment for customers where they are fully engaged in the shopping process and the search for rare items. In addition, the Super Savers Club loyalty program offers various bonuses, allowing members to earn and spend points and other bonuses.

- SVV constantly improves its supply reception, sorting, and retail trading processes. Recent initiatives include self-service checkouts in stores and an automated book processing system that effectively identifies, evaluates, and sorts books by genre, author, and price. In addition, the previously mentioned sorting centers also enhance SVV's competitive advantages.

Thus, SVV has developed a reliable business model that easily integrates internal business processes. The comprehensive approach the company takes at every step of its operations sets it apart in the second-hand clothing market and creates new opportunities for growth.

Reason 3. Improved forecast for 2024, backed by a clear growth strategy

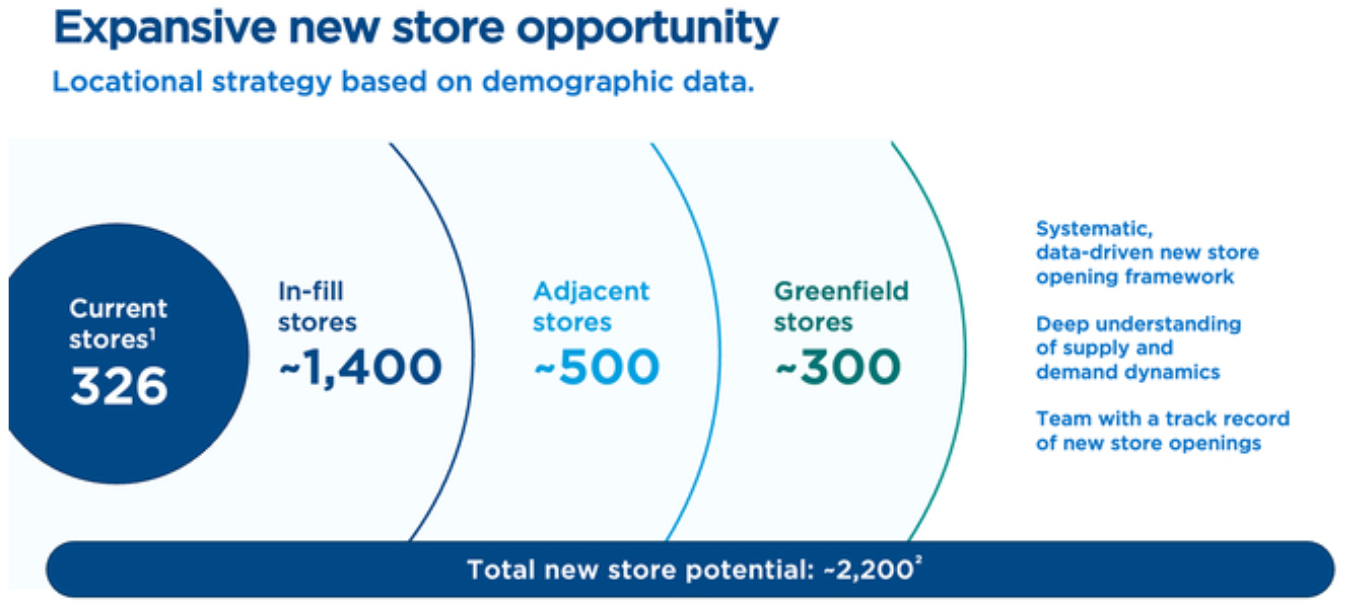

The SVV growth strategy includes three key components. First and foremost, it involves expanding the store network. The company has identified about 2,200 potential new locations in the US and Canada. In 2023, 12 stores were opened, and this year plans to open another 22 new stores (lease agreements have already been signed for 21 stores). For the period 2025-2027, the pace of opening new stores is expected to be at least 25 stores per year. SVV will use various opportunities to achieve such growth:

- Searching for attractive locations in existing markets and where the company has advantages in both supply and demand.

- Expanding presence in adjacent regions and states where the company can leverage existing operational capabilities and local market knowledge.

- Entering new markets, including such important regional markets as the southern and western states of the US and central Canada.

New SVV stores typically take an average of four years to reach necessary efficiency in sorting, turnover of donations, and retail demand. The company also has an alternative store format designed for regions with expensive real estate, through smaller-sized stores.

SVV's forecast for opening new stores

The second component of the strategy is comparable store sales growth. SVV aims to maintain a quality offering for customers, offering a wide range of quality used goods. To contribute to comparable sales growth, management plans to implement the following strategies:

- Ensure an adequate supply of quality goods to increase the frequency of purchases among existing customers and attract new customers.

- Invest in store upgrades to improve the consumer experience, implement new technologies to optimize store operations, and develop alternative store formats.

- Develop personalized email communications and targeted offers to increase engagement and purchase frequency among the growing base of loyalty program participants.

Enhance brand recognition to attract new customers.

Thirdly, SVV plans to selectively leverage opportunities for inorganic growth. Recognizing the fragmented nature of the second-hand clothing market, management intends to adhere to a disciplined approach to potential acquisitions. Key selection criteria for potential acquisitions include significant regional presence, access to quality supplies, strong brand recognition, and alignment with SVV's corporate values.

In the first quarter of 2024, SVV has already completed its first M&A deal of the year. In May, the company acquired 2 Peaches Group LLC - a second-hand store chain with seven locations in the Atlanta metropolitan area, Georgia. Thanks to this deal, SVV will enter the market of Georgia and will be able to further expand its presence in the southeastern states of the USA, where the company is virtually non-existent. While considering the local demographics and the attractiveness of the property, these states have significant growth potential. In addition, the 2 Peaches stores also provide an attractive and important supply base. However, the impact of the acquisition on SVV's financial indicators will only be significant in reporting periods after 2024.

Management recently presented an updated forecast for the 2024 financial year, increasing several target indicators:

- Store network: growth by 29 stores, including the opening of 22 new stores (unchanged) and seven stores due to the acquisition of 2 Peaches.

- Revenue: from $1.57 billion to $1.59 billion (unchanged).

- Comparable store sales: growth of 2%-3% (unchanged).

- Net income: from $85 million to $92 million (revised upward from $78 million earlier).

- Adjusted net income: from $126 million to $133 million (revised upward from $123 million earlier).

- Adjusted EBITDA: from $330 million to $340 million (revised upward from $340 million earlier).

- Capital expenditures: from $105 million to $115 million (unchanged).

Thus, SVV is a leading second-hand clothing store operator due to its successful business model and commitment to sustainable development. The company has good prospects for 2024, which include plans to expand the network of stores and improve financial performance. If these goals are achieved, shareholders will be able to share this success with the company. However, this will require innovative thinking and breakthrough decisions from the management, as the second-hand goods market is still very young and business models of companies need constant improvement.

Financial Performance

The financial results of SVV for the last 12 months (TTM) can be summarized as follows:

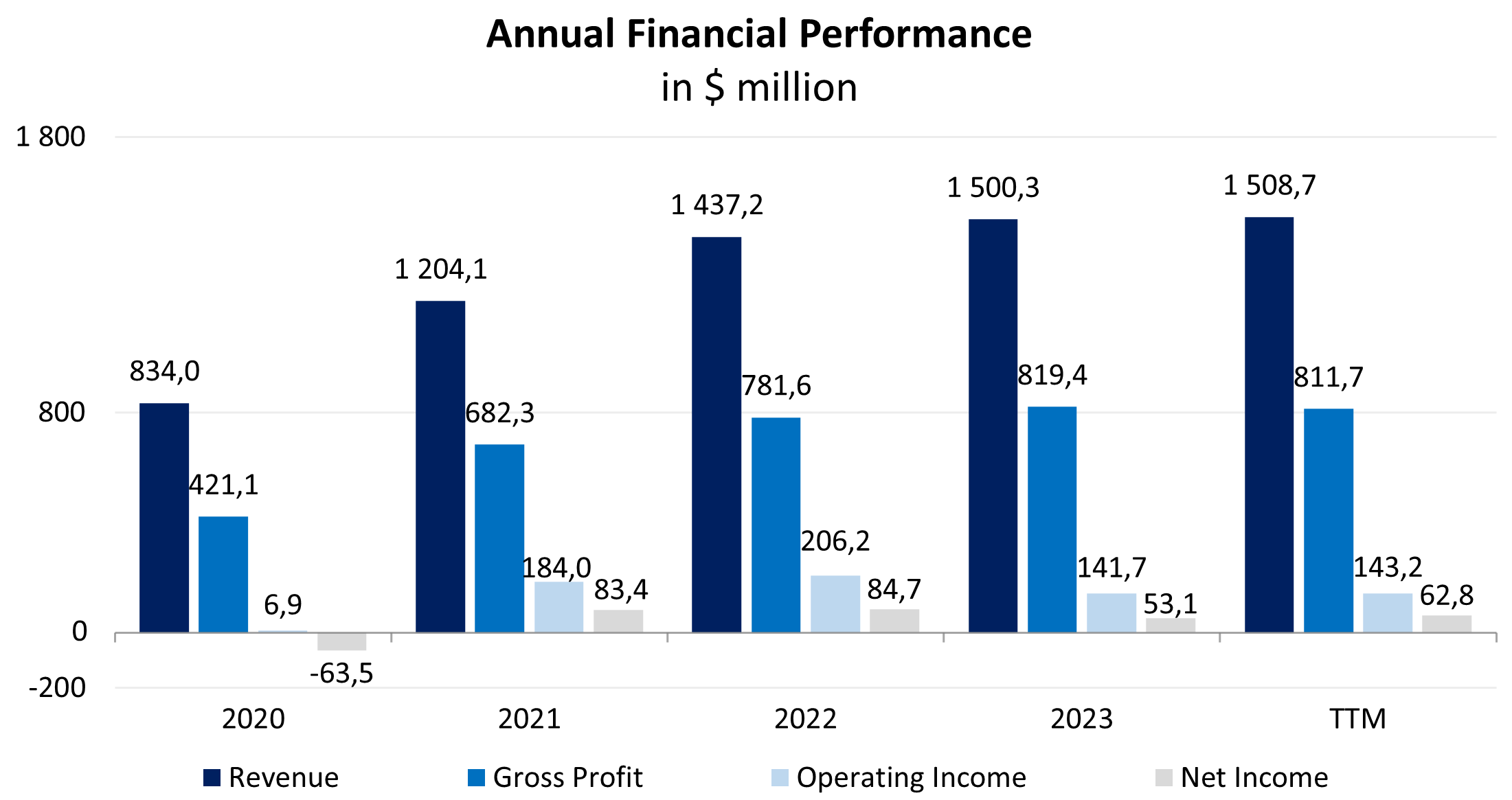

- Revenue has almost remained the same, reaching $1,508 million, increasing by 0.6% compared to 2023. The weak revenue growth is explained by the challenging macroeconomic conditions in Canada. As a result, while comparable sales in the U.S. increased by 2.3%, Canada saw a decrease of 2.6%.

- Gross profit also did not show significant dynamics, slightly decreasing from $819.4 million in 2023 to $811.7 million TTM due to the cost of goods sold. Gross profitability decreased from 54.6% to 53.8%.

- Operating income increased by 1.1% and amounted to $143.2 million thanks to the optimization of commercial and administrative expenses. Operating profitability remained at the same level - 9.5%.

- Net profit grew by 18.3%, from $53.1 million in 2023 to $62.8 million TTM. This improvement is due to a decrease in interest expenses and other one-time expenses related to early repayment of lease liabilities. Net margin increased from 3.5% to 4.2%.

Company's financial performance dynamics

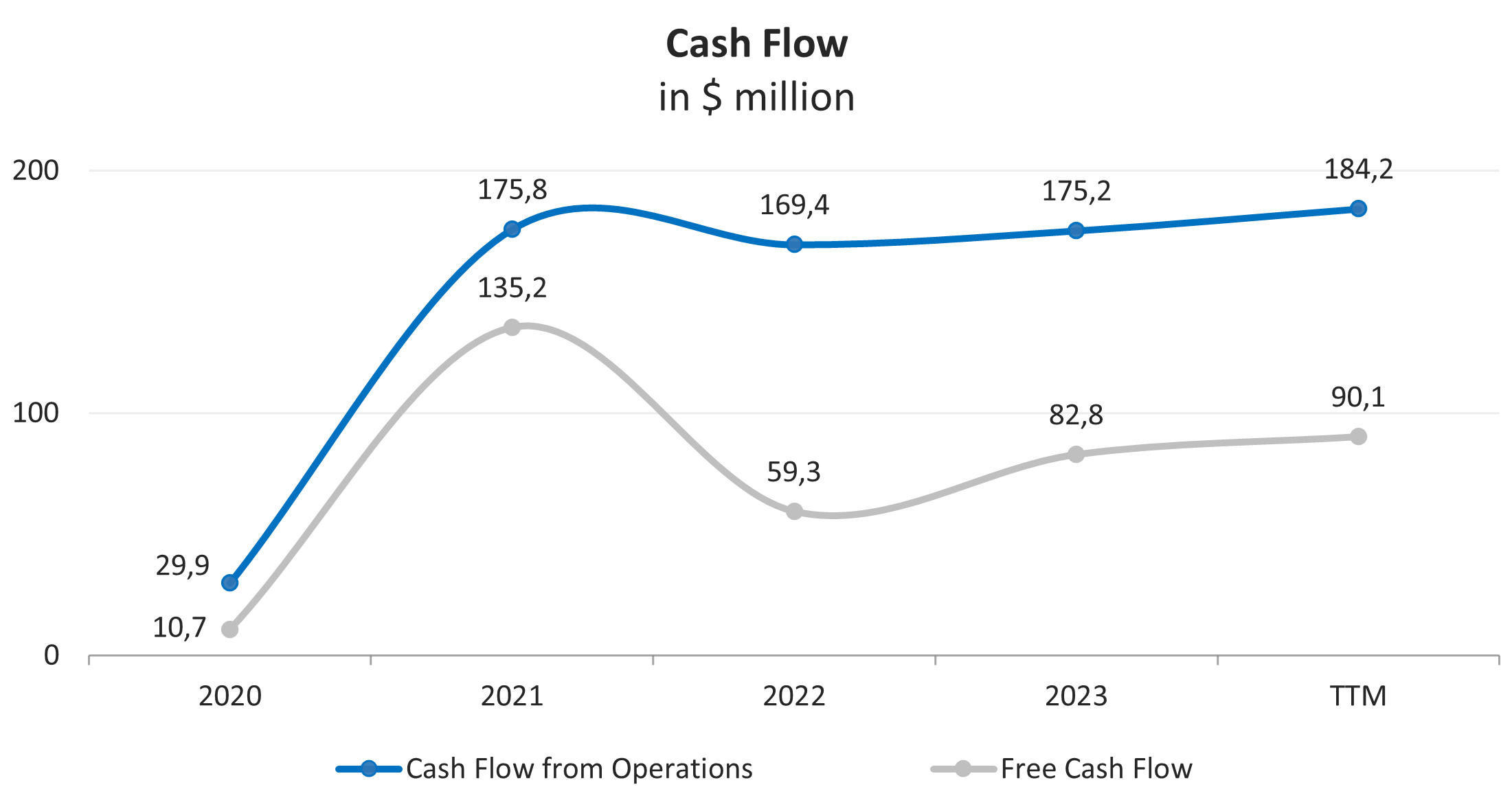

SVV's cash flows have been stable over the past few years. Operating cash flow (FFO) amounted to $184.2 million TTM, which is 5.1% more than in 2023 due to net profit growth. Free cash flow (FCF) amounted to $90.1 million TTM, up 8.9% compared to 2023.

Company's financial performance dynamics; source: compiled by the author

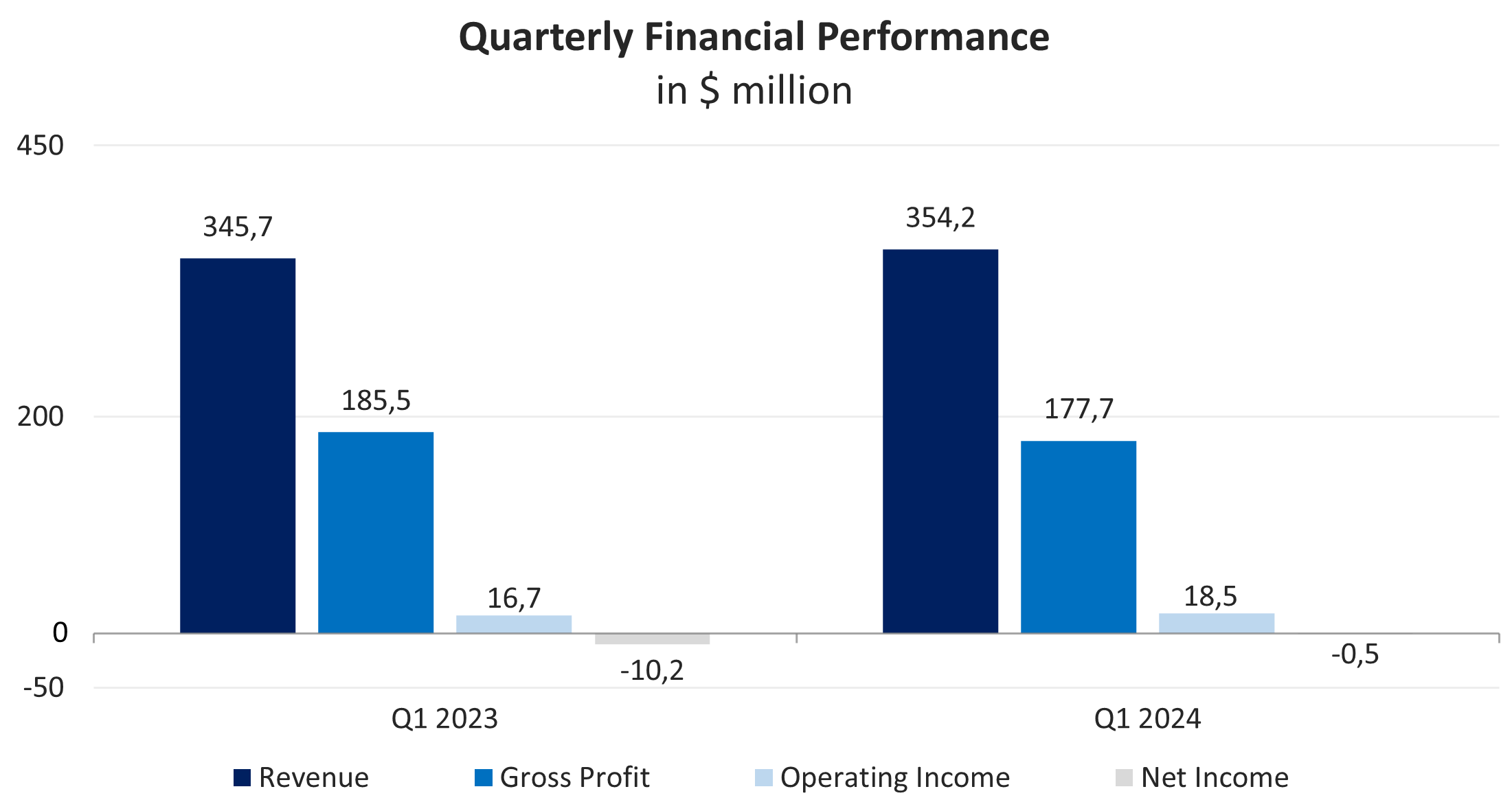

Below are the company's financial results for the 1st quarter of 2024:

- Revenue increased by 2.5% y/y, from $345.7 million to $354.2 million.

- Gross profit decreased by 4.2% y/y, from $185.5 million to $177.7 million.

- Operating profit increased by 10.8% y/y to $18.5 million.

- Net loss decreased by 95.4% y/y, from $ -10.2 million to $ -0.5 million.

Company's financial performance dynamics

SVV has a fairly high debt load, but the company's balance remains stable:

- The debt load ratio, defined as the ratio of total debt to assets, is 69%, which is slightly higher than the average competitor ratio of 60%.

- As of March 30, 2024, the total debt was $741.9 million, which is 6.0% less than the same indicator a quarter earlier ($789.1 million as of December 30, 2023). With cash and cash equivalents of $102.2 million, the net debt is $639.7 million.

- The company earned TTM EBITDA of $208.2 million, and therefore, the net debt to EBITDA ratio is 3.07x. Such a debt ratio is moderate and demonstrates the company's financial stability. However, investors need to monitor its financial situation in case of potential debt increase or cash flow problems.

- Interest expenses decreased by 9.7% compared to 2023 to $80.1 million TTM. With TTM EBIT of $143.2 million, the interest coverage ratio is 1.79x.

- The inventory turnover ratio in 2023 was 24.92x - this means that the company turned over inventory every 15 days on average during the year. Over the past five years, the average inventory turnover was 16 days. In Q1 2024, SVV increased inventories by 40.4% YoY, and turnover increased to 18 days TTM.

Evaluation

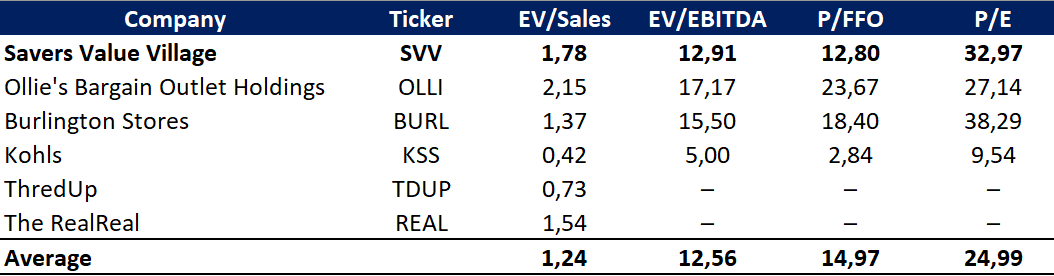

SVV is trading at a premium to its competitors on the main multipliers: EV/Sales - 1.78x, EV/EBITDA - 12.91x, P/FFO - 12.80x, P/E - 32.97x. However, the company operates in a promising market, has an ambitious development strategy, and its business is already profitable unlike some competitors. Thus, SVV offers better profit per unit of risk taken.

Comparable valuation

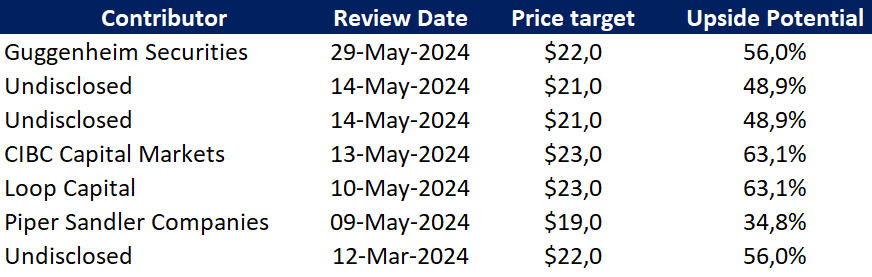

The minimum price target set by Piper Sandler Companies is $19.0 per share. In turn, CIBC Capital Markets values SVV at $23.0 per share. According to the Wall Street consensus, the fair market value of shares is about $20.0, implying a growth potential of 45%.

Price targets of investment banks

Key Risks

The SVV business model is based on supplies from local charities, so it depends on the ability to receive a sufficient amount of quality goods at attractive prices. If the company fails to achieve cost reductions and favourable prices, its profitability will suffer.

SVV's business depends on recruiting and retaining talented key management personnel and team members, as the second-hand industry faces high staff turnover, workforce shortage, and wage growth.

The retail second-hand business is subject to economic conditions at both global and local levels. Various factors, such as unemployment, high consumer indebtedness and economic downturn, can negatively affect retail spending.

SVV uses an Automated Book Processing System (ABP) and the Corporate Processing Centre (CPC) technology, which were developed by Valvan Baling Systems NV. Exclusive usage rights are regulated by special agreements. If SVV cannot extend the relevant agreements with Valvan, it could negatively affect SVV's business and its operational results.

The second-hand clothing market is competitive and rapidly changing. If SVV cannot effectively compete with existing companies or with new entrants, or cannot develop strategic relationships with non-profit partners, it could adversely affect the company's financial results.