What's the idea?

Nice offers three unique platforms for different usage scenarios, but united by common capabilities: optimisation, automation and AI-based analytics presentation. These solutions significantly increase productivity in labour-intensive areas such as contact centres, police, justice and financial compliance. The company's products are recognised as leaders in their respective fields.

The target market for Nice solutions is estimated at $11 billion and is expected to grow at a compound annual growth rate (CAGR) of 21.8% from 2023 to 2028.

A strong partner network helps the company to maintain a leadership position in its fragmented industry.

Nice is transforming its business towards cloud services with a growing share of recurring revenue, moving the company's profile closer to a pure SaaS (Software as a Service) model.

Following the announcement of the departure of a long-serving CEO, Nice's shares plummeted. The company has since found a worthy successor and, with a well thought-out handover process, will be able to continue its successful operations. However, Nice's shares are still trading at a low level, providing an attractive entry point for investors.

Nice has double-digit sales growth, strong earnings and cash flow, and a lower market valuation than its peers.

About Company

Nice (NICE) is an international enterprise software provider of cloud platforms powered by artificial intelligence (AI). The company operates in two main areas: Customer Experience and Financial Crime & Compliance. The first segment offers solutions to optimise workflows and improve operational efficiency in contact centres, which ultimately improves the customer experience and increases sales. The Financial Compliance segment focuses on enterprise risk management, anti-money laundering, fraud prevention and compliance. Nice stands out for its application of AI in both areas, offering its solutions both in the cloud and through licensing. Approximately 83% of the company's revenue comes from the US.

Nice was founded in 1986 and is headquartered in Tel Aviv, Israel. NICE shares have been traded on the Tel Aviv Stock Exchange since 1991 and its American Depositary Receipts (ADRs) on the NASDAQ since 1996.

Why do we like Nice Systems Ltd ADR?

Reason 1: Market-recognized products targeting several large and fast-growing segments

Nice is a global enterprise software provider offering AI-enabled cloud platforms for two key areas: Customer Experience and Financial Crime & Compliance.

In the Customer Experience segment, which represents 83% of total revenues, Nice's main product is the CXone platform (Contact Centre as a Service, CCaaS). It is a cloud-based platform that integrates a wide range of customer experience applications, including a specialised AI-based application, Enlighten. It enables the creation and coordination of seamless customer experiences by combining automated services and human interaction capabilities:

- AI helps customers to solve some basic issues in an automated way.

- Employee performance is supported by specialized solutions.

- Elements of workflow optimization improve operational efficiency.

- AI-powered analytics takes a detailed look at the customer, creating a complete profile of their characteristics and needs, which provides transparency when interacting across channels.

- Ultimately, this improves the quality of the customer experience when interacting with the company.

Optimizing manual labor is critical for service organizations, where labor costs can be as high as 90% of total costs.

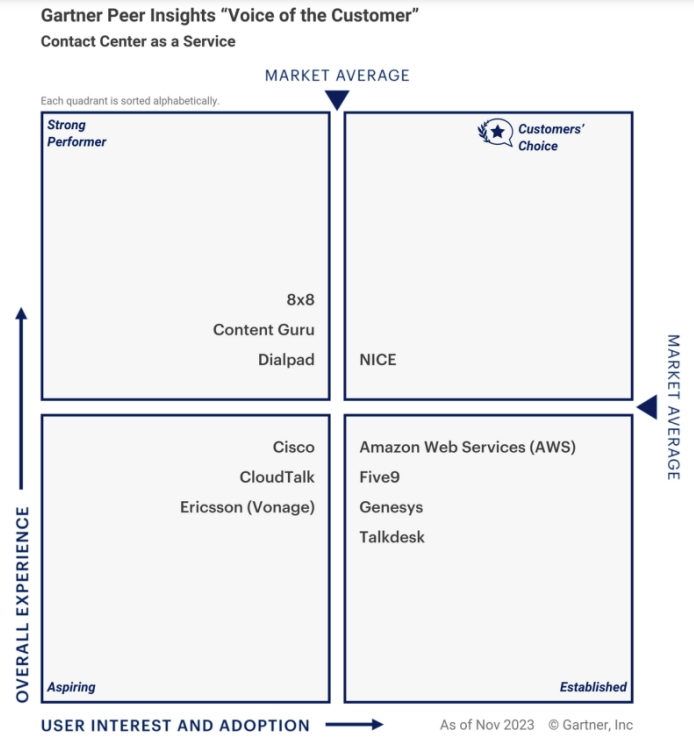

Nice is recognized as a leader in the Contact Center as a Service (CCaaS) segment: in the October Magic Quadrant study by consulting firm Gartner, the CXone platform is named the undisputed leader (its closest competitor Genesys is a private company). In addition, Nice is recognized in the Customer Choice category, which means that the product is recognized based on positive feedback from end users.

As the company points out, the CCaaS market has significant potential for further expansion: currently only 24% of services have moved to the cloud and only 5% are supported by AI. The company's strategy is to further develop AI capabilities to maintain the product's leading position, and to add new solutions to the cloud package to attract new customers and migrate existing on-premises users to the cloud.

Within the same segment, Nice offers a separate software solution, Evidencentral, for the police and justice system. It is an information management system that optimises the investigation process at all stages: from collecting evidence to solving crimes and preparing for presentation in court. All data is automatically collected in one place to provide a holistic and unified digital representation of the case, increasing the productivity of the investigation and the presentation of the case in court.

In the Financial Crime & Compliance segment (17% of annual revenue), Nice focuses on risk identification, fraud and money laundering prevention, and sanctions list verification. Through the use of AI, the platform automates high-volume routine tasks, allowing staff to focus on more complex and strategic issues while maintaining the quality of compliance. The X-Sight platform is focused on large companies, while the Xceed product offers an easier-to-use solution for the mid-sized segment.

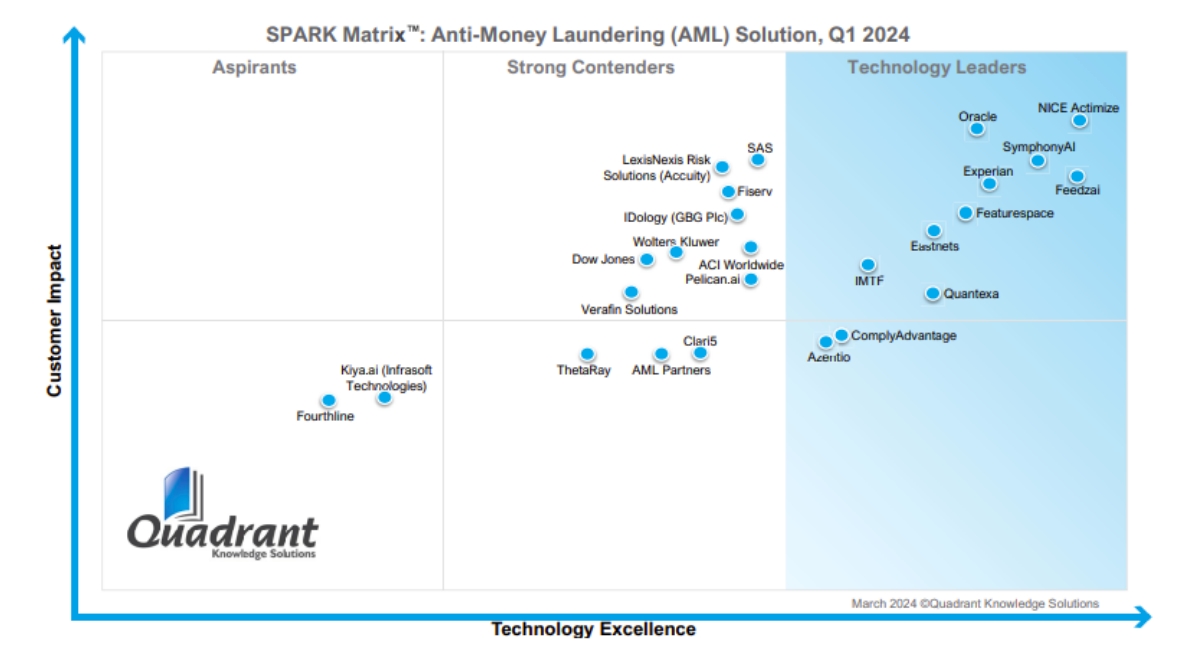

Nice products are also recognized as leaders in this area as well: Nice Actimize is rated by Forrester as one of the best solutions for fraud prevention and by Spark as one of the best solutions for money laundering prevention, along with solutions from companies such as Oracle and SymphonyAI.

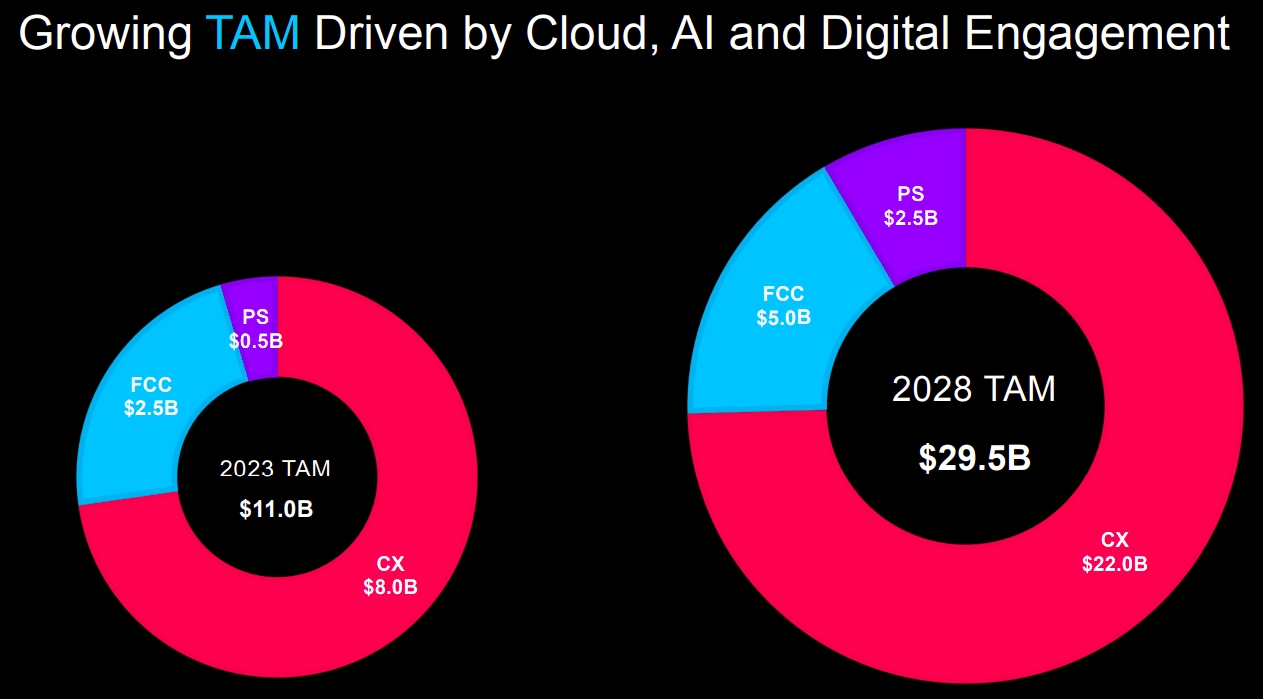

Nice's products target an $11 billion market, the bulk of which is the customer experience segment (total addressable market (TAM) $8 billion in 2023), which is expected to grow at a CAGR of 22.4% and double in five years. The financial compliance segment (TAM $2.5 billion) will also double by 2028 (CAGR 14.9%), and the smallest market for police and court solutions (TAM $0.5 billion) will quadruple over the same period.

We pay particular attention to the quality and market impact of a company products, as industry recognition creates a self-perpetuating marketing effect. Nice is a recognised leader in its segments and offers its customers products of outstanding value. The combination of a strong product with promising expansion rates in all target markets provides a solid basis for the company's investment growth.

Reason 2: Growing share of cloud business strengthens the company's profile through recurring revenues

Nice is actively developing ecosystems for customers of all sizes, but highlights that its solutions are used by 85 out of 100 Fortune 500 companies. Nice's financial segment serves the top 10 banks in the US and EU, 10 global investment banks and 4 of the top 5 banks in the Asia Pacific region (APAC). CXone is one of only two CCaaS platforms with over one million users.

One of Nice's key success factors is its extensive network of partnerships with leading technology companies, communications providers and global system integrators. In a fragmented market, seamless integration with other technology solutions and joint marketing efforts with partners are critical to the company's long-term leadership and revenue generation on a global scale. Nice's technology partners include Google, Amazon, Microsoft, Oracle and SAP, while its integrators include KPMG, IBM, Accenture and other well-known brands.

Like many other companies that have been in the market for a long time, Nice provides some of its customers with perpetual licenses. At the same time, the company is actively working to migrate these customers to the cloud platform, turning individual license holders into subscribers to cloud solutions.

However, the presence of two divergent trends in the company's segments — cloud and individual license — slows down the overall revenue momentum somewhat. For example, in the first nine months (9M) of 2024, cloud revenues grew by 25.8% compared to the same period in 2023. At the same time, licence revenue (which the company classifies as 'products') fell by 4.4%, and service revenue associated with those licences fell by 6.8%.

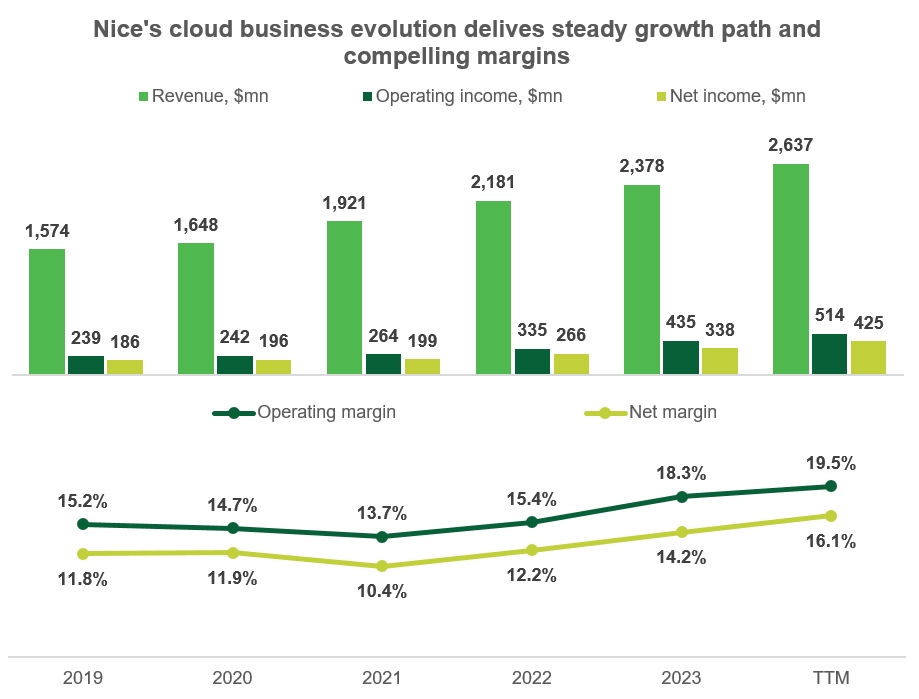

The cloud business is also showing significant growth in other metrics, with its annualized recurring revenue (ARR) surpassing the $2 billion mark in the last reported quarter. The business's share of the company's recurring revenue will increase from 53% in 2021 to 67% in 2023 and 72% in the third quarter of 2024. As the company's cloud business performance increasingly defines its profile and moves it closer to an absolute SaaS model, its valuation will become more transparent and predictable.

Reason 3: CEO change turmoil created attractive entry point for investors

Nice shares fell sharply in May 2024 following the announcement that Barak Eilam, the CEO who has led the company for the past 10 years, will step down at the end of the year.

Eilam has played a key role in Nice's successful transformation. Under his leadership, the company made the most profitable acquisition in its history when it bought inContact in 2016, making the customer experience platform its core product and radically changing its business profile. During Eilam's tenure, Nice has become a leader in CCaaS and its market capitalization has more than quadrupled.

Eilam's successor was not announced immediately and the reasons for his departure were not clearly explained, which the market took as a negative signal. As a result, by summer Nice shares had lost 40% of their 2024 highs.

In August 2024, Nice announced that a new CEO, Scott Russell, would take over in January 2025. Russell was previously chief revenue officer and a member of the executive board at German software maker SAP, where he ran several of its divisions. Russell has more than 25 years' experience in the enterprise software industry and his most recent roles have involved managing global sales and partnerships, which is critical to Nice's success. We believe that, despite some haste, Nice has selected the right candidate with a breadth of experience that will allow the company to continue to thrive under his leadership. Importantly, the current CEO will remain in an advisory role until mid-2025, easing the transition process for both the team and the new leader.

The instability caused by the CEO change reinforced the negative reaction of Nice investors to future competition from Microsoft, which has announced that it will enter the CCaaS market with its AI-based Dynamics 365 solution. Nice representatives said that so far they have not faced any active competition from Microsoft, and that Dynamics' current share of the related Customer Relationship Management (CRM) segment is only 5.9%, and that mutual reinforcement of Microsoft products does not pose an existential threat to the company.

However, the possible consequences of this competition are still uncertain. On the one hand, Microsoft can use its massive resources and coproductions to promote a new product. In particular, the acquisition of speech recognition software developer Nuance Communications in 2022 has strengthened Microsoft's contact centre expertise. On the other hand, for a customer to switch products after a successful multi-year relationship with the current vendor is a major inconvenience, and the benefits should be significant enough to justify the cost. We believe that Nice customers are unlikely to migrate to a Microsoft solution and that new users will choose a vendor based on the quality of the product, experience and expertise of the vendor. Salesforce is a good example: despite its bigger size, Microsoft has not been able to gain a significant share of the CRM market.

As Nice offers an excellent product that is already recognised in the highly saturated CCaaS market, the threat from Microsoft remains limited. Overall, we expect the pressure on investor sentiment to ease once the transition period for the new CEO is over and the stock returns to previous levels.

Financial performance

Nice's financial results for the trailing 12 months (TTM) through the end of Q3 2024:

- Revenue grew 10.9% over 2023 to $2.6 billion.

- Operating profit increased 18.2% to $514 million, with operating margin widening 1.2 p.p. to 19.5%.

- Net income soared 25.6% to $425 million (16.1% of revenue) and margins increased by 1.9 p.p.

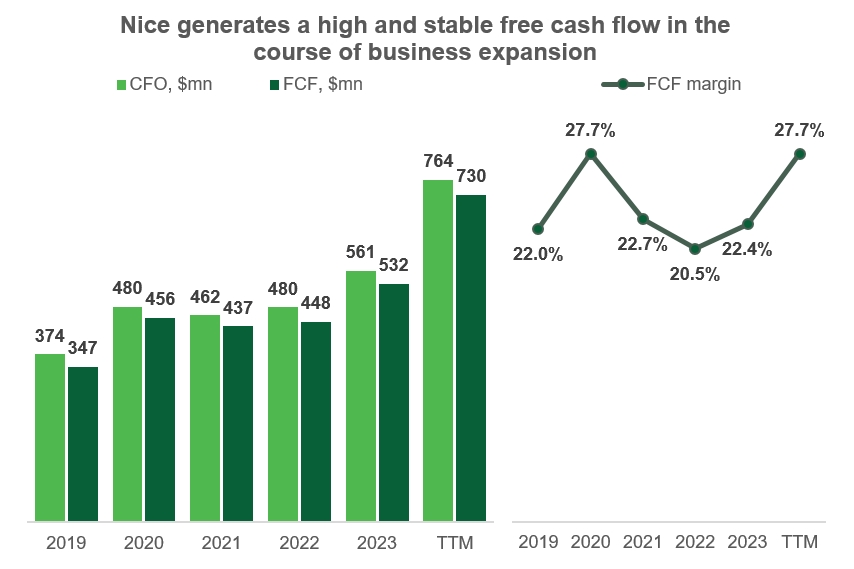

Cash flow from operating activities (CFO) grew by 36% to $764 million, while free cash flow (FCF) increased by 37.2% to $730 million. This growth was due to higher net income, accumulation of deferred revenue and changes in other assets and liabilities. Free cash flow margin reached its previous record level of 27.7%, which is 5 p.p. higher than in 2023.

Nice has $458.4 million of short-term debt with $666.7 million of cash and $860 million of short-term investments on the balance sheet.

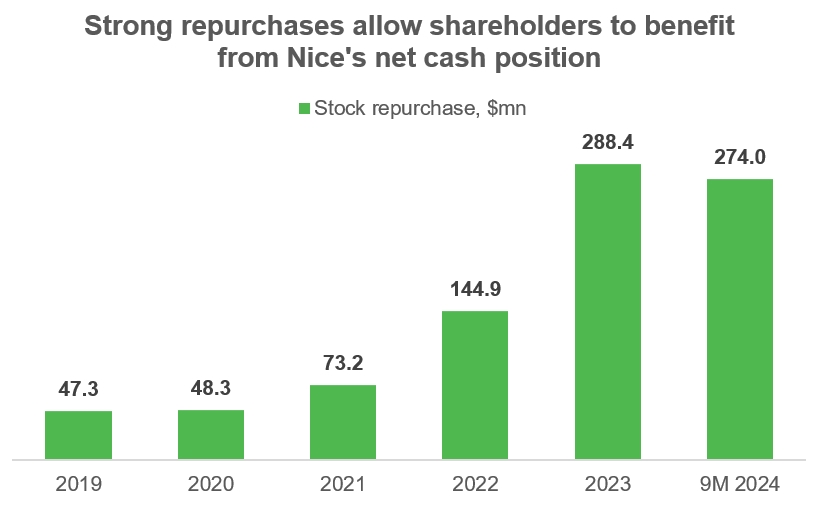

This strong net cash position, together with strong cash flow generation, allows the company to buy back its own shares. Nice has repurchased more than $270 million of its own shares in 9M 2024 and is likely to exceed the 2023 buyback record for the full year. The current $300 million buyback program, launched in November 2023, is almost complete, and Nice is expected to announce a new program soon as the stock is undervalued. In addition, the cash can be used to acquire complementary products and companies to strengthen Nice's platform offering.

Stock valuation

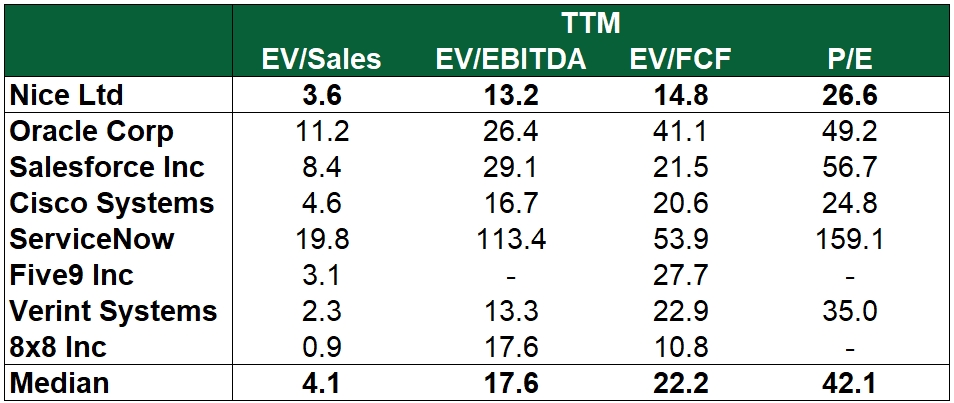

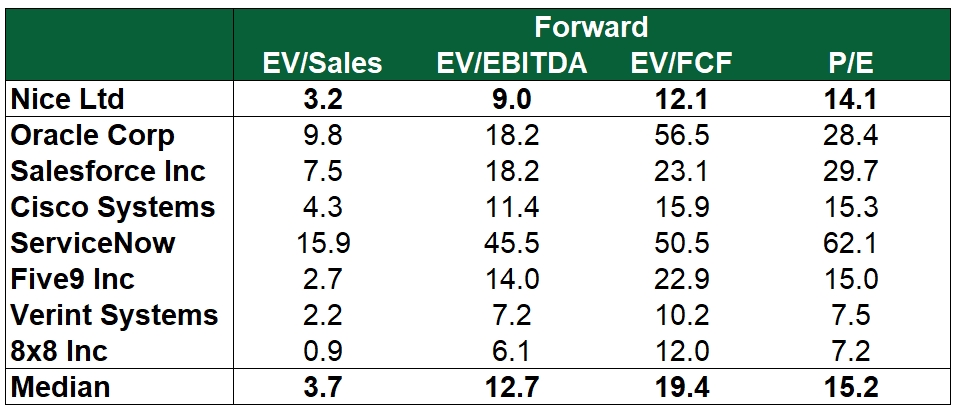

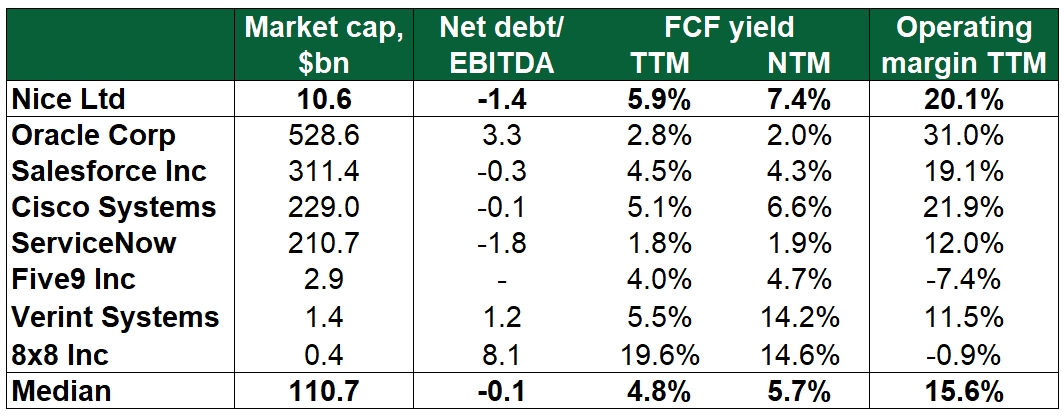

Nice stock presents an attractive valuation compared to its peers in the enterprise software industry. Current valuation multiples are discounted by 11% to 37%, while forward multiples show even greater discounts, ranging from 7% to 38%. This strongly suggests that the stock is undervalued relative to the revenues it generates.

One standout metric is the EV/FCF (Enterprise Value to Free Cash Flow) multiple, which assesses the company's performance based on its historical and forecasted free cash flow generation. Nice demonstrates the most significant discounts in this area: 34% on historical values and 38% on forecasted values.

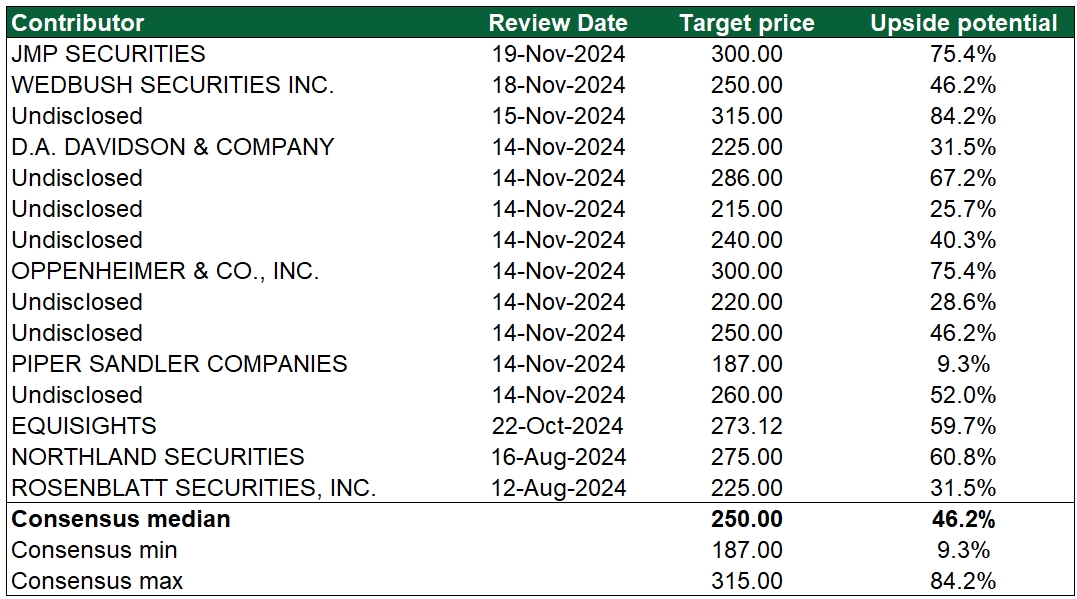

Wall Street analysts anticipate that the transitional effects of the recent CEO change will ease within the next 12 months, alleviating pressure on the stock. They project that the stock price will recover to levels seen prior to the CEO's departure announcement. The median price target of $250 per share suggests an upside potential of over 45%, while even the most conservative estimates indicate further gains. We consider $250 per share to be a realistic and attainable target, representing a potential upside of 36% for the stock.

Key risks

Intensifying competition from Microsoft: Competition from Microsoft could be stronger than anticipated, potentially constraining Nice's sales growth in the CCaaS segment.

Highly competitive and fragmented markets: Nice operates in dynamic markets characterized by intense competition and fragmentation. Failure to sustain the quality and competitiveness of its products may result in loss of market share and hinder revenue growth.

Management transition uncertainty: The leadership transition may not proceed as smoothly as expected. If the new management team fails to match the company's previous performance, investor confidence could waver, leading to a potential decline in the stock price.