What's the idea?

- Marvell has a better revenue mix than other companies in the semiconductor industry, with the consumer market accounting for less than 15% of its total revenues.

- Thanks to the transformation of existing data centres as well as the emergence of new ones, the company is facing high demand in the relevant segment.

- Given Marvell's strong positioning and the integration of digital technology into the automotive industry, we expect the automotive segment to provide a significant tailwind.

- In the long term, MRVL is expected to grow at an average annual rate of 15%-20%, with operating margins reaching 38%-40%.

- According to the Wall Street consensus, the upside potential for the MRVL stock price exceeds 60%.

About Company

Marvell Technology (MRVL) specialises in supplying infrastructure semiconductor solutions. The company designs and sells Specific Integrated Circuits (ASICs), electro-optics, fibre channel adapters, and processors and memory controllers. Marvell was founded in 1995 and is headquartered in Wilmington, Delaware.

Why do we like MARVELL TECHNOLOGY INC?

Reason 1. Low exposure in the consumer market

Amid tighter monetary policy and declining consumer spending, PC sales fell by a whopping 19.5% in Q3 2022, while smartphone sales fell 9% to their lowest level in eight years. As a result, the Philadelphia Semiconductor index, made up of the 30 largest semiconductor companies in the US, has lost more than 30% since the start of the year. The main drivers of the decline were companies specialising in semiconductors for consumer products, such as Nvidia and Advanced Micro Devices.

Philadelphia Semiconductor Index

The Marvell stock also performed worse than the index. The company has lost more than half of its market capitalisation since the beginning of the year. However, Marvell has a better revenue mix — the company serves five target markets:

- Data centres

- Carrier infrastructure

- Enterprise networking

- Cars (Automotive/Industrial)

- Consumer

It is worth noting, however, that the consumer segment accounts for less than 15% of total revenue.

Company revenue structure

At the end of the last reporting period, the data centre segment was up 48.4% year on year, the carrier infrastructure segment was up 45%, enterprise networking was up 52.8% and automotive/industrial was up 45.6%. Only the aforementioned consumer segment decreased by 0.6%.

Typically, corporate clients are characterised by high inertia — capital investment plans that have gone through several stages of approval and approval will not be adjusted momentarily. At the same time, the average duration of recessions is 10 months, and the long-term outlook for target markets remains high. Thus, low consumer market exposure will support Marvell's earnings in a period of market uncertainty.

Reason 2. Demand in the Data centre segment

Global trends such as the development of cloud services, video streaming, 5G wireless networks and machine learning have catalysed the demand for higher bandwidth and lower power consumption network connections. As a result, data centres everywhere have begun to migrate to 200G, 400G and 800G Ethernet, the latest standard for high-speed connectivity.

Marvell is following in the footsteps of this trend: with DSP PAM4 processors, the company offers a proven solution for high-speed optical connectivity. In March 2022, Marvell began mass delivery of DSP 800G PAM4. In addition to DSP PAM-4, the mass adoption of 200G, 400G and 800G Ethernet will provide increased demand for 400G ZR interconnects, SSD controllers and application specific integrated circuits (ASICs).

In addition to the transformation of existing data centres, we will also see the emergence of new ones. The data centre market in North America is expected to grow at a compound annual growth rate (CAGR) of 21.98% through 2026, with a combined growth rate of a whopping $615.96 billion. These trends are the main driver for the data centre segment, which has doubled in the past two years, with revenue reaching $1.78 billion in 2022 versus $823.8 million in 2020. It is worth noting that Marvell is the second fastest growing company in the data centre segment, behind only Advanced Micro Devices. The figure below shows the companies' revenues in the respective segment for the first half of 2022 and 2021.

Comparison with peers

Marvell has significantly improved its competitive moat through significant spending on research and development and strategic acquisitions. In May, the company acquired Tanzanite, a startup specialising in Compute Express Link (CXL) design. Already in November, the company introduced the Marvell CXL development platform for cloud data centre operators. This solution will enable operators to optimise their infrastructure and simplify the process of memory scaling.

Reason 3. Long-term potential of the automotive segment

The automotive segment accounts for only 6% of total revenue, but is one of Marvell's main long-term growth drivers. According to Allied Market Research, the automotive semiconductor market was valued at $37.99 billion in 2020 and is expected to reach $113.94 billion in 2030, a CAGR of 11.8%.

Although the segment's revenues were up an impressive 67.1% year-on-year in the first half of 2022, management said the company was underperforming due to supply chain issues. Indeed, automotive companies have experienced severe semiconductor shortages in the recent past and some industry giants have been forced to suspend plant operations. However, during the latest conference call, management noted that the situation is improving.

The segment's high growth rate is driven by the growing adoption of Ethernet technology in the automotive industry. In the first quarter, company executives shared that Marvell's Ethernet design solutions are used by 8 of the top 10 Original Equipment Manufacturer (OEM) companies worldwide and 36 OEMs overall. Notably, Marvell solutions are suitable for both internal combustion engine vehicles and electric vehicles, expanding the potential target market. Given the company's strong positioning among the largest OEMs and the growing integration of digital technology in the automotive industry, we expect this segment to provide Marvell with significant tailwinds.

Financial indicators

The company's results for the past 12 months can be summarised as follows

- TTM revenue stood at $4.46 billion, a 50.3% increase on 2022.

- Gross profit rose by 36.2%: from $2.06 billion to $2.81 billion. Gross margin increased from 46.26% to 50.94%.

- Operating profit rose from -$348 million to $110 million. The operating margin was 2% compared to -7.79% at the end of the year.

- Net profit was -$218 million compared to -$421 million for the year. The net profit margin rose from -9.43% to -3.95%.

Trends in the company's financial results

Company margin dynamics

Marvell's operating loss is driven by high R&D spending, which accounts for about 30% of the company's revenue. The R&D-adjusted operating margin would have been 33.8%.

MRVL is expected to grow at an average rate of 22.9% over the next three years and achieve stable profitability from 2023. In addition, during the last conference call, the company's management reiterated its long-term goals, according to which revenue will grow at an average annual rate of 15%-20%, gross margins will reach 64%-66%, operating margins will reach 38%-40% and free cash flow margins will exceed 32%.

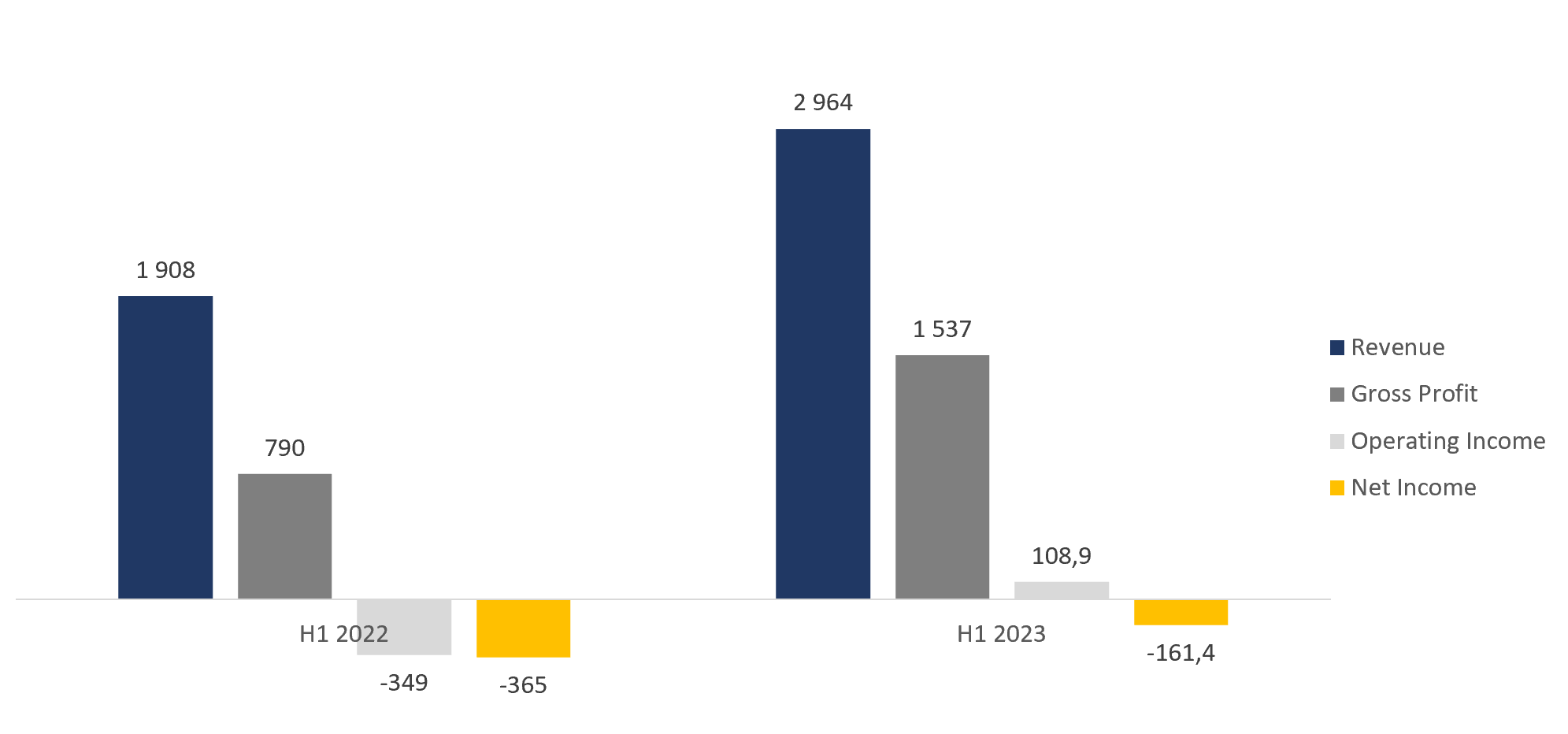

The financial results for H1 2023 are as follows

- Revenue rose 55.3% year on year, from $1.91 billion to $2.96 billion.

- Gross profit rose by 94.5% year-on-year: from $790 million to $1.54 billion. Gross margin increased by more than 10% : from 41.40% to 51.86%.

- Operating profit was $109 million compared to -$349 million a year earlier. The operating margin increased from -18.29% to 3.67%.

- Net profit was -$161 million compared to -$365 million a year earlier. Net margin increased from -19.11% to -5.45%.

Trends in the company's financial results

TTM operating cash flow stood at $1.14 billion in the latest reporting period, compared to $819 million for the full year. Free cash flow to equity rose from $632 million to $755 million. The increase was driven by higher net income.

Company cash flow

Marvell has a healthy balance sheet: total debt is $4.60 billion, cash equivalents and short-term investments account for $617 million and net debt is $3.98 billion, which is 1.8 times TTM EBITDA (Net debt/EBITDA — 1.8x).

Evaluation

Marvell trades at a premium to peers: EV/Sales — 7.51x, EV/EBITDA — 25.34x, P/Cash flow — 32.93x. The premium is driven by significant profitability growth potential, which is well reflected in the forward P/E multiple of 16.32x versus the industry average of 17.18x.

Comparable estimate

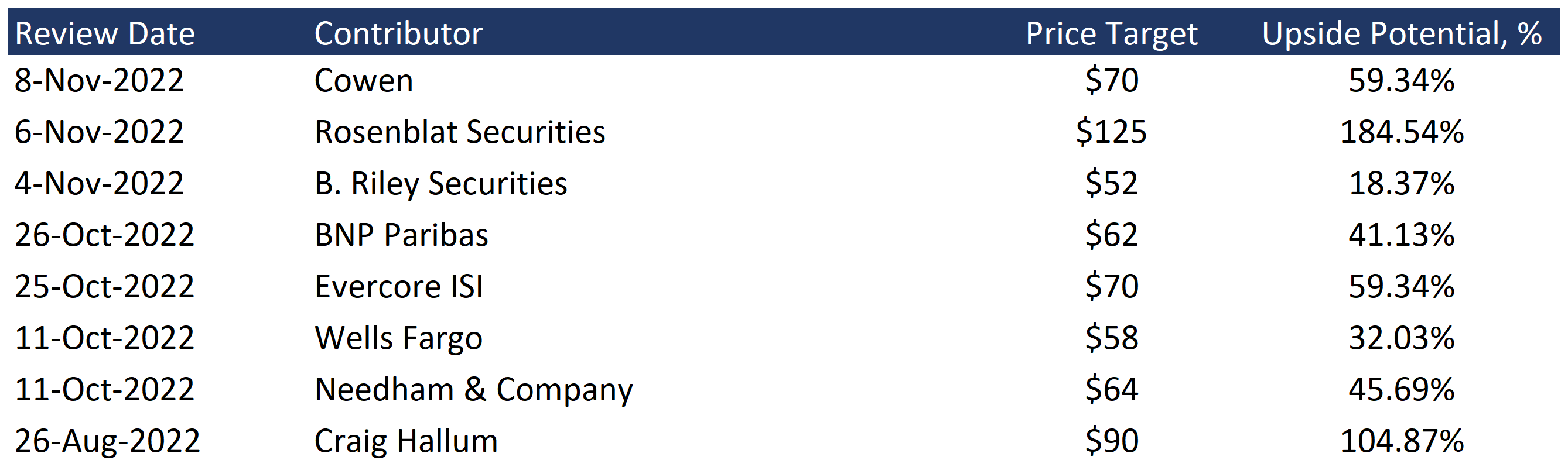

The minimum price target from investment banks set by B. Riley's is $52 per share. Rosenblat Securities, on the other hand, values MRVL at $125 per share. According to the consensus, the fair market value of the stock is $71.80 per share, which suggests an upside of 63.5%.

Price targets of investment banks

Key risks

- Marvell is valued by the market as a growth company and trades at appropriate multiples. A slowdown in the growth rate could lead to a significant revaluation of the company's stock.

- Although the company is currently facing strong demand for its solutions, there is a risk that demand will decline, due to the deteriorating global macroeconomic environment.

- Marvell operates in a highly competitive market with major players such as AMD, NVIDIA and Broadcom. This factor could affect the company's ability to grow organically in the long term.