What's the idea?

LivaNova operates in a highly specialized field and manufactures products of recognized quality. The company feels confident in its market niche despite the presence of large competitors.

The target markets of the company's two key business segments are projected to grow at a compound annual growth rate of 5% to 9% over the next few years.

Different segment profiles contribute to the stability of the company: the Cardiopulmonary segment is characterized by higher sales growth, while the Neuromodulation segment provides higher profitability.

LivaNova is restructuring its business, strengthening its focus on key areas and reducing costs. Despite temporary losses from write-downs and revaluation of assets, the restructuring optimizes the company's operations and improves the overall business profile, ensuring stable growth and higher profits in the future.

The increase in the company's financial guidance during the year reflects the success of LivaNova's new products and allows us to expect good momentum for the company's performance in 2025.

Based on improving margins and cash flow generation, we expect the discount to the current valuation of the stock to gradually narrow.

About Company

LivaNova (LIVN.US) is a medical technology company that develops specialized innovative equipment for professional use in medicine. LivaNova was created in 2015 through the merger of Sorin S.p.A., a player in the treatment of cardiovascular diseases, and Cyberonics, a company with key expertise in neuromodulation.

LivaNova operates in the following business segments: Cardiopulmonary, which develops, manufactures and markets products for cardiopulmonary surgery; Neuromodulation, which specializes in devices for neuromodulation therapy for epilepsy and depression; and Advanced Circulatory Support, which manufactures temporary life support systems.

Why do we like LivaNova PLC?

Reason 1: Highly specialized products targeting markets with attractive growth prospects

LivaNova is a medical technology company that manufactures highly specialized devices for cardiopulmonary surgery and neuromodulation.

The Cardiopulmonary segment includes the development, manufacture and sale of the following equipment:

- ventilators;

- heating and cooling systems that regulate the patient's body temperature during surgery;

- oxygenators to oxygenate the blood;

- autotransfusion systems for circulatory support;

- perfusion tubing systems, cannulas, and other accessories.

Circulators are used to perform heart and lung functions during surgery when the patient's own heart is temporarily shut down. Heating and cooling systems maintain optimal body temperature, oxygenators replace respiratory function, and autotransfusion systems maintain blood flow. Such a range of products allows LivaNova to cover to a great extent the needs in equipment for cardiovascular operations, providing a high level of specialization and authority of the company in this field.

The market for cardiac surgical devices is specialized but quite large: it is estimated at $28.7 billion in 2024 and could grow to $43.4 billion by 2031 at a compound annual growth rate (CAGR) of 5.3%. Other sources estimate the market size at $17.1 billion in 2023, but a similar CAGR of 5.5% through 2030. This confirms that LivaNova's target market has prospects for dynamic development.

The Neuromodulation segment specializes in systems that stimulate specific parts of the nervous system to achieve a positive effect in the patient. LivaNova manufactures the VNS Therapy system, which stimulates the vagus nerve with an implantable pulse generator for the treatment of drug-resistant epilepsy (DRE) and treatment-resistant depression (DTD). The segment also includes surgical equipment for performing implantation and related products. The VNS Therapy system is available in several device variations with different features. It was the first product approved by the FDA for the treatment of DRE, and it remains the only product authorized for use in children 4 years of age and older in the United States. In many other countries, the device has no age restrictions.

Following the acquisition of ImThera in 2018, LivaNova began development of aura6000, a new implantable neurostimulation system for the treatment of obstructive sleep apnea (OSA). The new system is undergoing clinical trials and offers prospects for the company to enter a new market in the future.

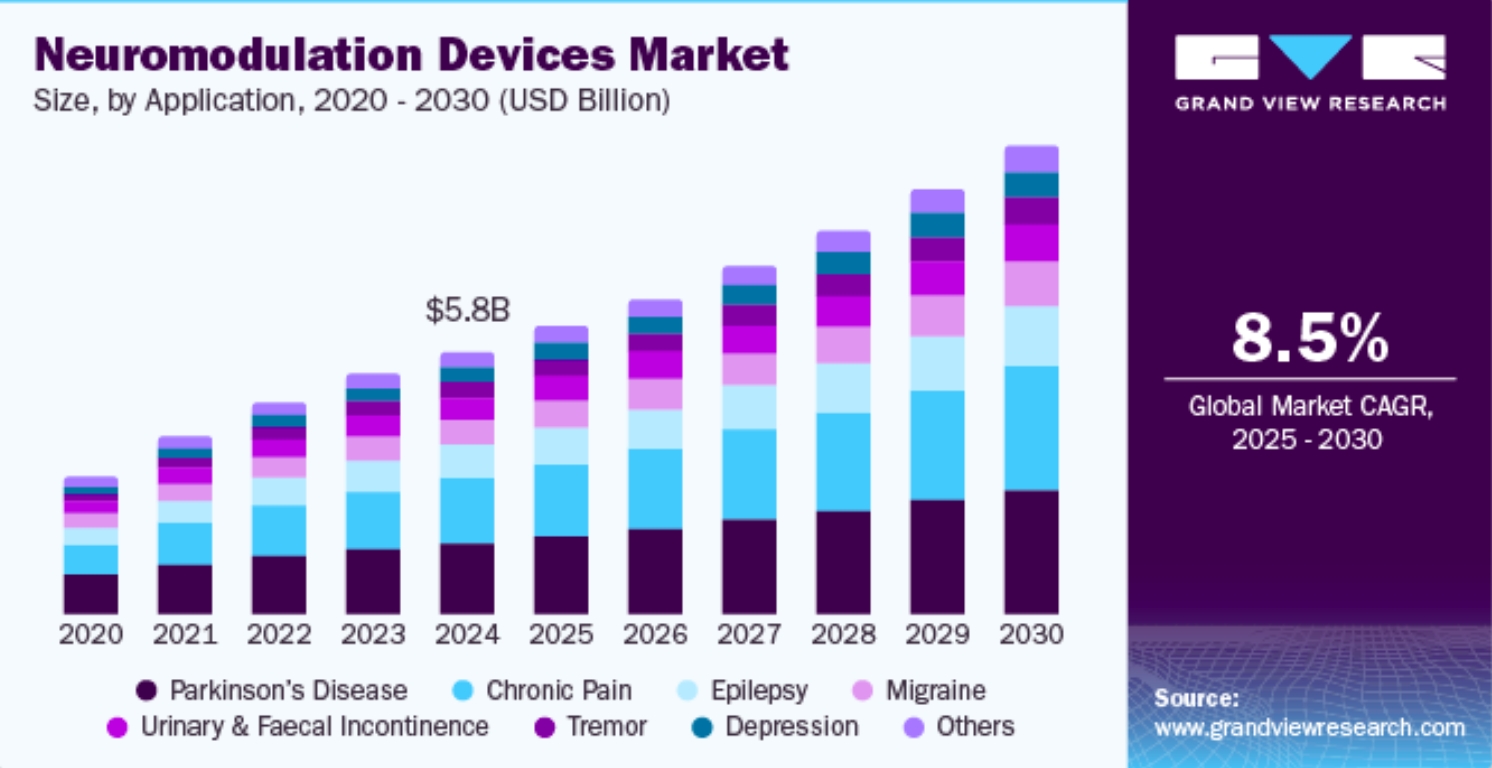

The neuromodulation market remains a niche market. Its size is estimated at approximately $5.8 billion with an attractive CAGR of 8.51% through 2030. The unique specialization of devices limits competition in this field.

Obstructive sleep apnea (OSA) is a condition that affects about 1 billion people worldwide and is not always correctly diagnosed. According to WHO, 2/3 of apnea cases are associated with obesity or being overweight, and these problems affect one in eight people on the planet. With increasing awareness and accuracy in diagnosing sleep apnea, the OSA treatment devices market, estimated at $9.7 billion in 2024, could reach $18.3 billion by 2032 at a CAGR of 8.3%.

The Advanced Circulatory Support (ACS) segment previously included products for temporary life support as well as consumables such as cannulas. In January 2024, LivaNova decided to focus on its two main segments (cardiopulmonary and neuromodulation) and cease operations in the ACS segment by the end of 2024. Starting in 2024, consumables have been included in the cardiopulmonary segment and other products are being phased out.

Thus, LivaNova operates in several areas characterized by high demands for scientific capabilities, which forms a barrier to entry for new players, yet the company's target markets have an attractive growth profile.

Reason 2: Recovery of growth and positive momentum in key segments allow company to raise guidance

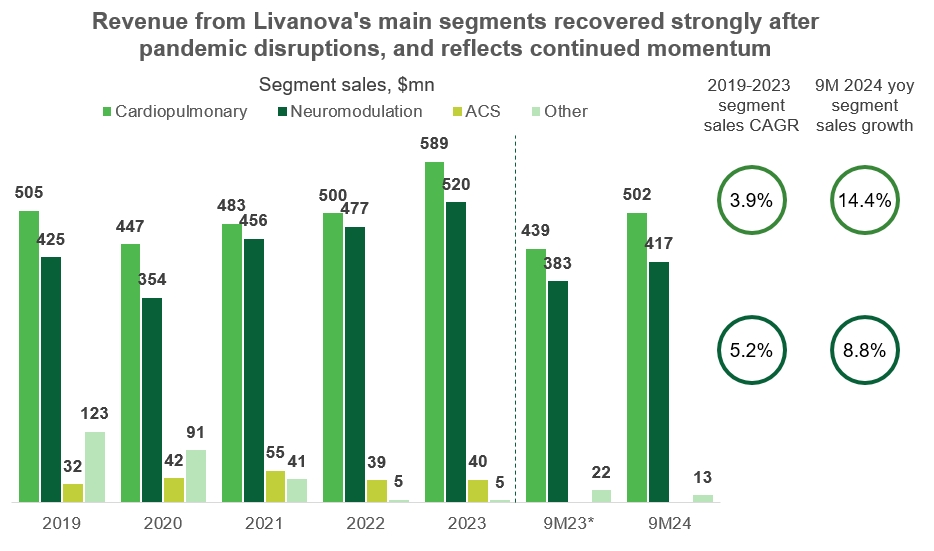

Livanova's business was significantly impacted by the restrictions imposed by COVID-19, which resulted in delays and postponements of heart surgeries and reduced purchases of related equipment. The company has now fully recovered. In 2023, its sales grew 12.9% year-on-year (YoY) and two key segments are also showing attractive growth rates, with cardiopulmonary sales up 14.4% YoY in the first nine months (9M) of 2024. Although the neuromodulation segment grows more slowly — +8.8% over the same period — it generates significantly higher revenues. While the cardiopulmonary segment increased its margin to 11.2% in 9M 2024, the neuromodulation segment has been generating operating margins of around 30% or more for the past four years. Taken together, this combination of segments represents a fairly attractive business profile.

In 2024, the Cardiopulmonary segment will receive an additional boost from the inclusion of the ACS cannula sales. The graph below shows the sales growth already including the reallocation of cannulae to the Cardiopulmonary segment in the revised 9M 2023 results.

Note: revenue segmentation for 9M 2023 has been changed to include cannula sales in the Cardiopulmonary segment. In 2021, the company exited the heart valve business and this revenue is included in the Other segment.

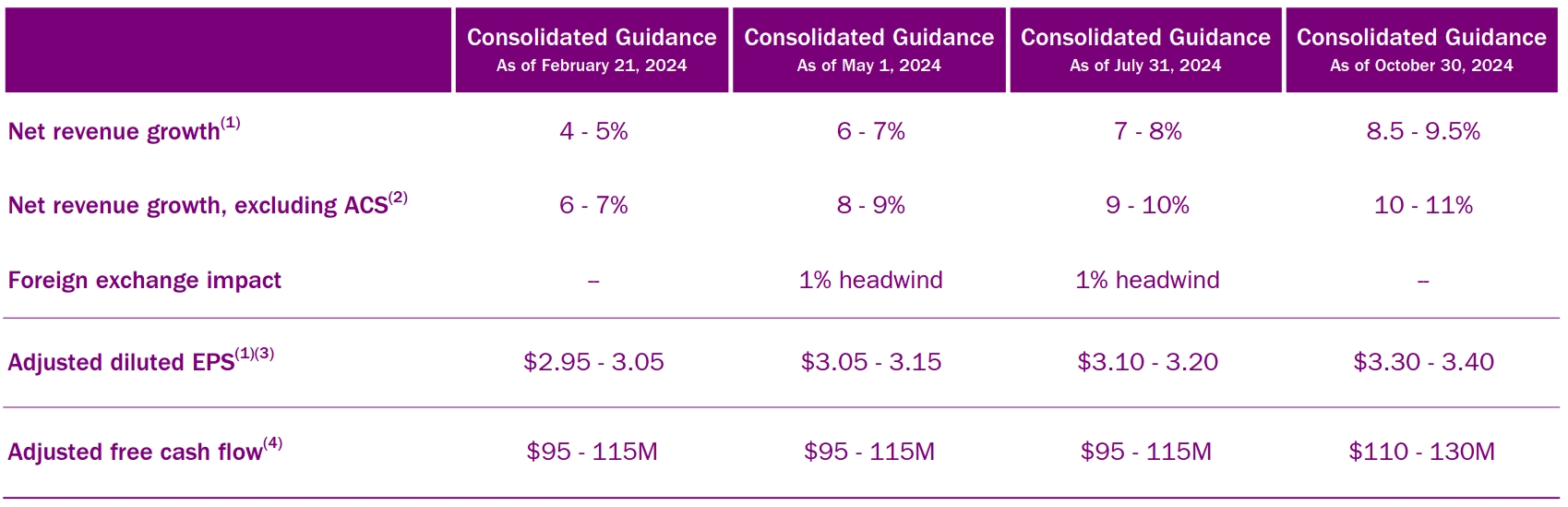

During 2024, LivaNova revised its annual financial results forecasts upward several times. In Q3, the annual revenue growth forecast was raised to 8.5%–9.5%, well above the original 4%–5% forecast. Earnings per share (EPS) guidance was raised 11.6% to a range of $3.30–$3.40, and free cash flow (FCF) guidance was raised 14.3% to $110–$130 million relative to the very first guidance. Thus, the company is well on track to deliver a combination of revenue and margin growth that is likely to continue to improve through 2025.

Reason 3: Colossal innovation potential drives revenue growth and target market expansion

Although LivaNova has not yet provided a forecast of financial indicators for 2025, the key segments of the company's business demonstrate attractive growth rates, which is due to the accumulated results of innovations and research at different stages. Research-based growth is a long-term trend, and the company benefits from the accumulated research potential in several directions at once.

In the cardiopulmonary segment, the supply of oxygenators exceeds demand worldwide, which contributes to price increases. LivaNova is expanding its production capacity and has already increased its market share: from just over 30% at the beginning of 2023 to approximately 35% in 2024. To maintain the growth rate, the company is developing a new generation of oxygenators.

The Essenz perfusion system, introduced in early 2023, has been extremely successful. It assists perfusionists during artificial circulation procedures. Essenz has a modular design, includes a next-generation artificial circulation machine, and a monitoring and safety system for convenient patient monitoring. This product has been a significant driver of the company's sales growth, contributing approximately 4 percentage points of revenue growth in 2024. Management expects Essenz to account for 40% of all orders placed for circulators this year.

In the neuromodulation segment, sales growth rates are more moderate but stable. Shipments of implants for new surgeries and replacements accounted for 8.8% growth in 9M 2024. Among the drivers of growth in this segment in the near future is the introduction of the aura6000 implantable hypoglossal neurostimulator for the treatment of patients with moderate to severe OSA, clinical trials of which the company is currently conducting.

In November, studies showed that the new device met basic safety standards and had a significant clinical impact. In randomized controlled trials, after just six months of treatment with aura6000, the median apnoea-hypopnoea index decreased by 66.2% and the oxygen desaturation index decreased by 63.3%. These results will be used to support the submission of a Premarket Approval Application (PMA) for the system to the US Food and Drug Administration (FDA). Results from studies following 12 months of therapy are expected in 2025 to show the long-term benefits of the device for patients.

LivaNova's innovation potential is also focused on improving existing products in the neuromodulation field. For example, the company is currently developing an improved VNS therapy system with updated communication functionality.

The continuous development of LivaNova's scientific base supports the company's financial results. We expect the positive impact of both current developments and initiatives to enter new markets to be reflected in the share price for the foreseeable future.

Reason 4: Restructuring will free up resources and allow the company to focus on key segments

LivaNova's restructuring plan for 2024 aims to optimize the business and increase the focus on two main business areas: cardiopulmonary and neuromodulation.

The ACS segment experienced difficulties in 2022 due to a decrease in the number of patients requiring extracorporeal oxygenation as a result of a decrease in the number of severe COVID-19 cases. Segment sales decreased by 29% compared to 2021. The segment incurred a goodwill impairment charge of $129 million in 2022 and an additional $102.6 million in 2023 due to the impairment of goodwill and inventory resulting from the restructuring decision.

Overcoming the negative dynamics of the segment, which represents only 4% of total sales, would have required a strategic effort disproportionate to its importance. The negative financial result due to the segment's write-downs put pressure on the company's overall financial statements and created tension for investors and management.

As a result, the company decided to redirect management's efforts and resources to strategically important areas and completely shut down the troubled business. Restructuring costs will range from $15 million to $20 million in 2024, of which $14.3 million has already been utilized in 9M 2024.

The restructuring of LivaNova is expected to have a positive impact on the company's sales growth and profitability. Towards the end of 2024, the impact of the initiative will become more visible and the associated costs will no longer weigh on the company's operating profit.

Financial results

LivaNova's financial results for the trailing 12 months (TTM) as of the end of Q3 2024:

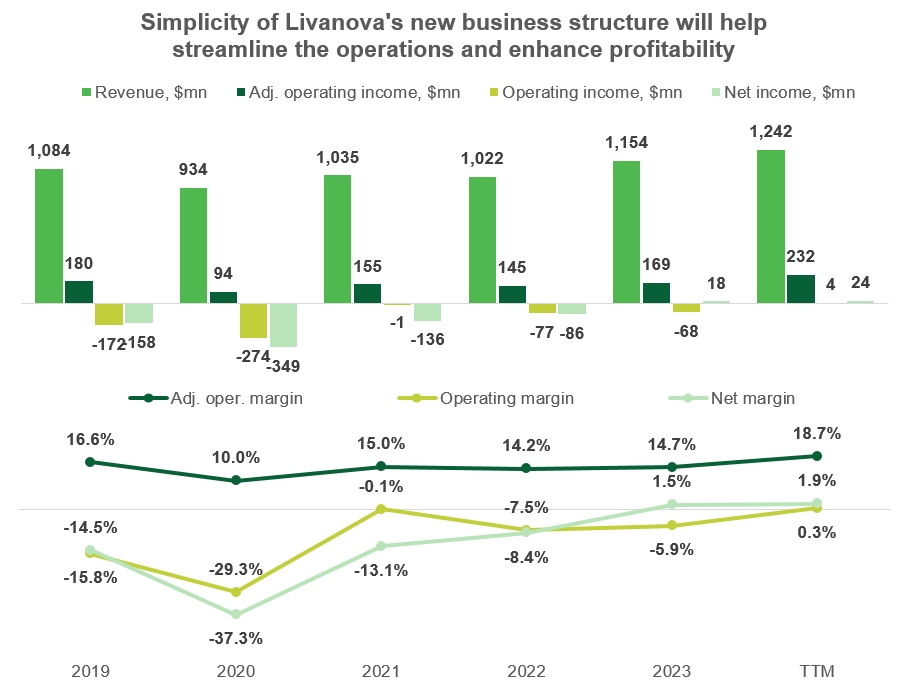

- Revenue grew 7.6% compared to 2023 to $1.24 billion.

- Operating income improved to $4 million from -$68.5 million. For 9M 2024, operating income was $92 million versus $19 million a year earlier. Margin remains close to zero, just 0.3%, but improved from -5.9% in 2023.

- Net income rose 34.8% to $23.6 million and net margin improved 0.4 p.p. to 1.9%.

- Adjusted operating income increased 36.8% to $231.6 million and adjusted operating margin widened 4 p.p. to 18.7% of revenue TTM.

Adjusted operating income takes into account restructuring charges, legal fees and reserves, non-cash stock-based employee bonuses, amortization of acquired intangible assets and write-downs of assets classified as held for sale. While such measures are useful for assessing the sustainability of the underlying business, we view GAAP measures as more reflective of the entire company, including the restructuring of the business portfolio.

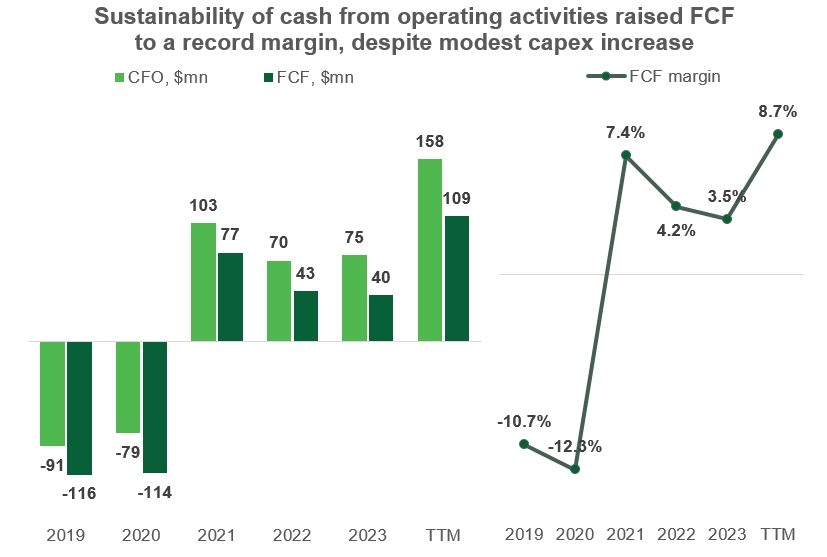

TTM cash flow from operations (CFO) more than doubled compared to 2023 to $158 million. Free cash flow (FCF) increased 172% to $109 million. The primary impact was a combination of higher net income and the effect of larger but non-operating effects, such as the loss on debt extinguishment in 2024 and the absence of derivative revaluations that supported net income in 2023. These factors make the current level of net income more sustainable. In addition, LivaNova has reduced its investment in inventories compared to last year. Together, these effects have increased FCF from 3.5% of revenue in 2023 to 8.7% of revenue over the past 12 months, despite a slight increase in capital expenditures.

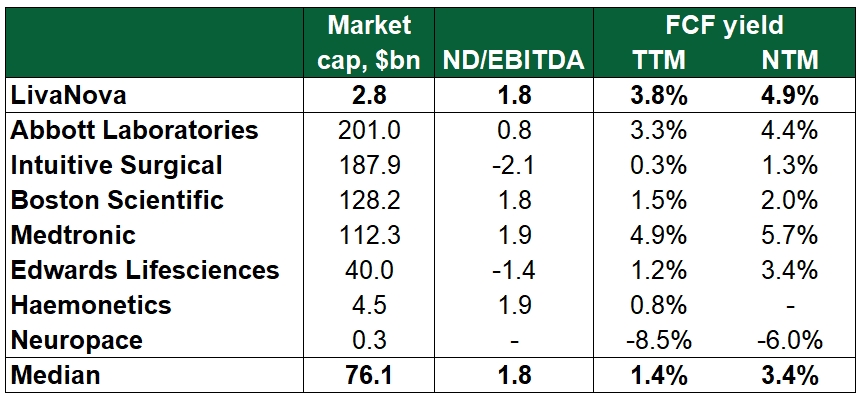

LivaNova has $626.3 million of debt, of which only $22 mln is short-term. Cash reserves total $346.4 million, which provides for a moderate debt burden of 1.78x EBITDA. In addition, the company has $320 million of restricted cash on its balance sheet as collateral for loans. The interest expense coverage of normalized EBIT is approximately 2.12x. Thus, the company's debt position is quite stable and is not a source of risk for the company.

Stock valuation

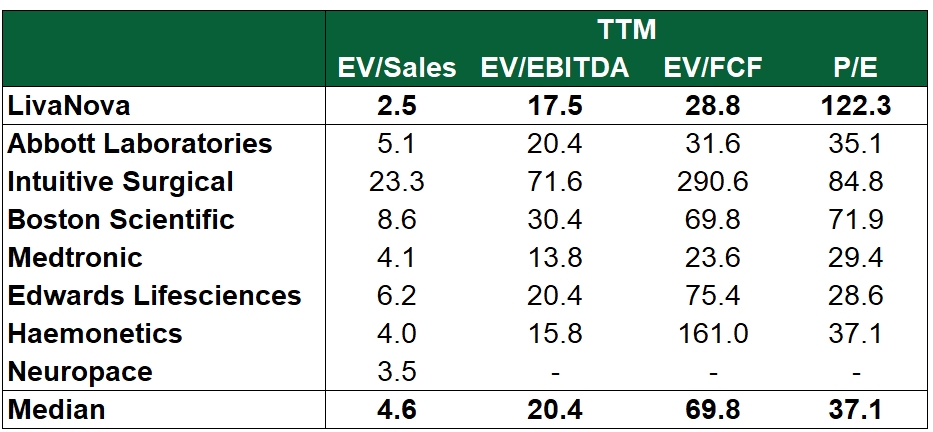

LivaNova is a strong niche player. At the same time, some of its competitors are large diversified medical device companies with high margins, which supports the valuation of their shares. Therefore, it is important to consider the limitations of comparative valuation in this case due to the different growth stages of the company.

LivaNova is one of the most moderately valued companies in its peer group. Multiples on sales reflect a discount of more than 40%, while the current EV/EBITDA multiple shows a discount of 14% to the group. The EV/EBITDA discount widens to 41% for the forward multiple. While the current EV/FCF and P/E multiples are volatile for both LivaNova and a significant part of its peer group, the forward multiples also confirm the undervaluation of LivaNova's shares. Despite weak GAAP operating margins, the company already generates strong cash flow. We believe the discount should narrow over time as the business achieves stable margins.

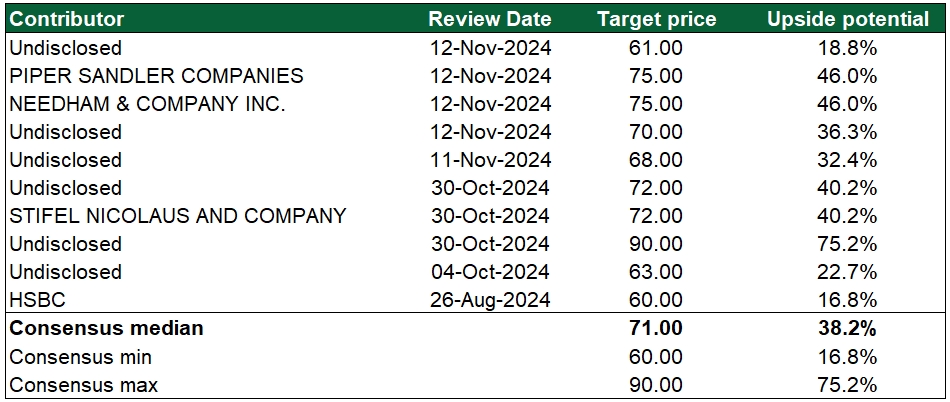

LivaNova’s stock has a large upside potential as the median target price from Wall Street analysts is $71.0 per share, which is more than 40.6% above the current stock price. The full range of estimates covers growth scenarios from 17% to 75%.

Key risks

Clinical trial risks are an inherent part of doing business in the medical device industry. If LivaNova's current trials are less successful than expected, or if the FDA does not approve new products, the share price could suffer.

The company has several pending lawsuits. Despite provisions for payments, unexpected changes in the course of the proceedings could affect the net result and delay the achievement of stable profitability.

The lack of production capacity in the oxygenator market may limit LivaNova's sales potential. However, the same constraints also apply to its competitors, giving LivaNova the opportunity to increase its market share.