What's the idea?

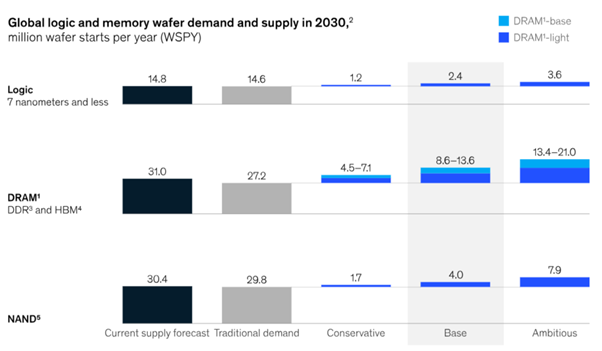

The active training of neural networks requires a qualitative increase in computing power, which leads to higher demand for Rambus' products. McKinsey predicts that the global economy will need 8.6 million to 13.6 million new memory chips by 2030 just to develop neural networks, which implies a growth rate of nearly 50%.

Market Research estimates that the global market for memory interface chips will grow from $1.04 billion in 2023 to $3.58 billion by 2029, representing a compound annual growth rate (CAGR) of 22.77%. In late 2023, Rambus launched a new generation of memory interface chips that increased chip bandwidth by 50%.

In addition, last year the company optimized chip power consumption with DDR5 chips (PMICs) and introduced a new solution for quantum cryptography. Rambus is implementing a share buyback program with an authorized amount equal to 6.32% of the company's market capitalisation.

About Company

Rambus (RMBS) is a manufacturer of components for advanced, high-performance microchips used in a variety of computing devices. The company was founded in 1990 and is headquartered in California, USA.

Why do we like Rambus Inc?

Reason 1. Data center chip market growth

Rambus manufactures components of modern high-performance microchips that are used in various computing equipment. The company's management estimates that more than 75% of its current revenue is generated in the data center chip market.

In particular, Rambus develops and manufactures:

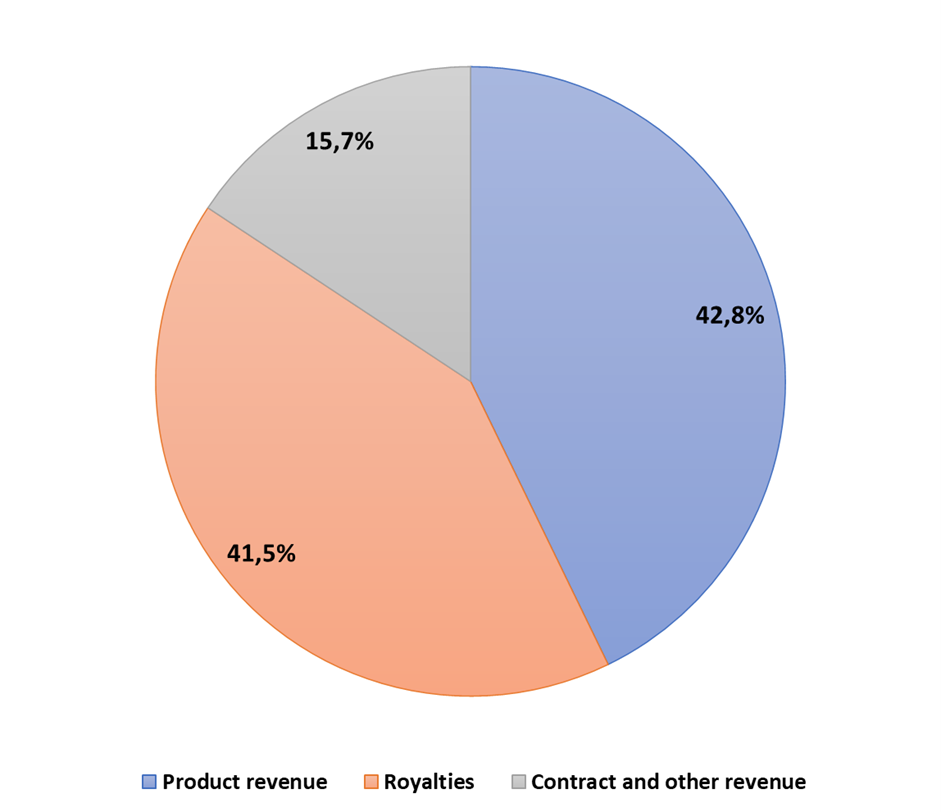

Memory Interface Chips (MIC) are special chips that enable communication between a server's processor and its RAM. MIC performance growth is one of the key drivers of the industry, as without MIC progress, processors have limited processing power that is held back by the so-called "memory wall." Revenues from this product category are reported in the Product Revenues segment and represented 42.8% of the company's total revenues in H1 2024.

Silicon interface IP solutions — modules developed and patented by Rambus, or so-called prefabricated blocks used in chip manufacturing. In this category Rambus creates memory modules and controllers.

Silicon security IP solutions — include one of the most comprehensive data center security chip offerings in the industry. The company's products include cryptographic security products, hardware security products, etc. Revenues from this and previous product categories are reported in the Contract and Other Revenues segment and represented 15.7% of total revenues in H1 2024.

Other chip components that Rambus develops and further leverages to enter into license agreements with third-party companies that use Rambus solutions to manufacture computing equipment. The company currently has license agreements with most industry participants, including AMD, Broadcom, IBM, Micron, Micron, NVIDIA, Qualcomm, Samsung and others. Revenues from this product category are accounted for in the Royalty Revenue segment and represented 41.5% of total revenues in 1H 2024.

Company's revenue structure in H1 2024

Given Rambus' specialization in serving the data center equipment market, the economic environment is currently in the company's favor.

For example, McKinsey notes that the active development and scaling of neural networks has given an additional impetus to the demand for computing power. Against this background, industry leaders have increased investments in the expansion of data processing centers, as well as the construction of new plants for the production of relevant equipment, including microchips.

The increased demand for computing equipment at the current stage is explained by the fact that neural networks require much more information at the training stage compared to the operation of a ready-made generative model. Today, neural networks are being actively trained by a number of companies, so the industry requires rapid growth of computing power of data processing centers.

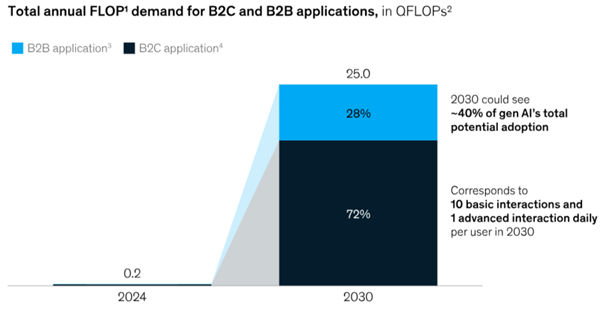

McKinsey estimates that these trends in the baseline scenario will result in total demand for artificial intelligence (AI) computing could reach 25x10³⁰ Floating Point Operations (FLOP, a unit of measure for processor performance) by 2030, representing a 125x increase from 2024.

Growing demand for AI computing

According to McKinsey, the growth in demand for computing power will increase the need for components of data center equipment, including DRAM (DDR) memory chips, which Rambus produces. According to the agency's baseline forecast, the industry will need 8.6–13.6 million new memory chips by 2030, a growth rate of nearly 50%.

Expected growth in the number of different chips

On the Q2 2024 investor conference call, Rambus management expressed confidence that the development of AI will drive data center investment over a long period of time.

In monetary terms, the target markets for Rambus products will also show significant growth. Market Research estimates the global memory interface chips market to reach a volume of $3.58 billion by 2029 from $1.04 billion in 2023, which implies growth at a CAGR of 22.77%.

Markets and Markets forecasts that the chip intellectual property market will also show growth to reach $11.2 billion by 2029 versus $7.5 billion in 2024, assuming a CAGR of 8.5%.

Thus, with the active development of neural networks, the global economy requires increased computing power for the training and continuous use of generative AI models. Analysts estimate that the available computing power is insufficient to meet the growing demand, which will increase the need for Rambus' data center solutions.

Reason 2. Launch of new products

At the Q2 2024 investor conference call, Rambus management said that the company is focused on continuing to scale memory chip bandwidth and capacity to achieve the best customer offering in the industry.

As noted above, improving memory interface chip bandwidth remains a hot topic for the industry, as the growth of overall data center performance depends on it. According to Rambus, while processor performance is increasing, memory interface chip bandwidth is not keeping pace with comparable growth rates, slowing the entire data center industry.

However, there are players in the market who have been developing higher performance products that have already become the new standard in the industry. One of them is Rambus, which launched its next-generation Gen4 DDR5 (RCD) chips at the end of 2023.

This product has become an industry leader in terms of throughput, which has increased by 50% from 4,800 to 7,200 megatransactions per second. As Rambus CEO Shane Rau noted in the company's press release, Gen4 DDR5 (RCD) are critical to supporting the performance, power and signal integrity requirements of AI servers.

In this regard, demand for the new chip is likely to be driven by the dynamics of development of high-performance data centers used for training neural networks. According to McKinsey's forecast, this market segment will grow strongly until 2030.

In April 2024, Rambus introduced another new product, the ultra-modern DDR5 power management ICs (PMICs), to complement its Gen4 DDR5 (RCD) solution. The company noted that equipment in AI data centers is subjected to extreme loads and is designed to operate for 24 hours a day. As such, the issue of overheating of computing power is extremely important to industry players.

A new Rambus DDR5 chip (PMICs) designed specifically for servers running neural networks has managed to maintain the previous level of power consumption despite an increase in the performance of on-board elements. With this new product, Rambus was able to offer customers a comprehensive memory interface chipset that supports multiple generations of DDR5 server platforms.

Another interesting piece of know-how that Rambus has recently brought to market is an IP solution for quantum cryptography, the Quantum Safe Engine. The relevance of this product is explained by the rapid development and growth of quantum computers, which allow multiplying computing power compared to conventional computing devices. However, the increase in performance of quantum computers is not a clear benefit: the technology can be used to decrypt (crack) the classical cryptographic methods used today. Quantum Safe Engine uses special quantum-resistant algorithms to protect data centers from cyber-attacks in the post-quantum computing era.

Thus, new Rambus products prove that the company is able to offer the market relevant solutions demanded by the market at the current stage. This is confirmed by the growth of the company's financial indicators, which will be described in more detail below.

Reason 3. Share buyback program

Rambus is currently implementing a share buyback program adopted in 2020, under which the company can buy back 6.8 million of its own shares, the current value of which is $298.59 million, or 6.32% of the company's market capitalization. The share buyback may have a positive impact on the company's capitalization in the short term.

Financial performance

Rambus' financial results for the trailing 12 months (TTM) can be summarized as follows:

- Revenue totaled $477.53 million, a 3.56% increase over 2023.

- Operating income increased from $153.64 million to $210.46 million. Operating margin improved from 33.32% to 44.07%.

- Net income was $230.70 million compared to $333.90 million at the end of last year.

The growth in revenue and operating profit was mainly due to an increase in royalty income, which in turn was due to changes in the structure and timing of license renewals. This also had a favorable impact on the company's results for H1 2024. The decrease in net income was due to the receipt of income tax benefit in 2023.

Dynamics of the company's financial indicators

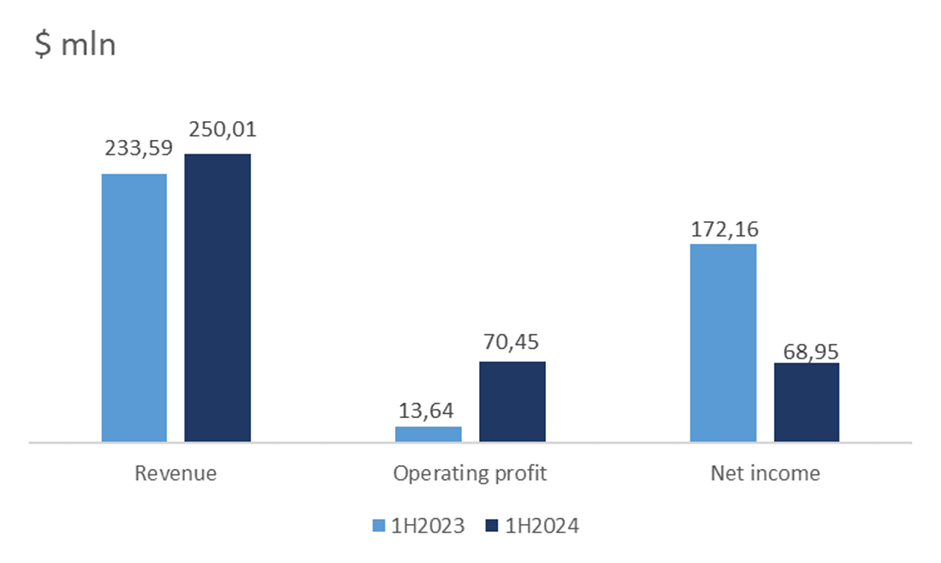

Rambus' results for H1 2024 are summarized below:

- Revenue increased 7.03% year-over-year (YoY) to $250.01 million.

- Operating income rose to $70.45 million from $13.64 million.

- Net income was $68.95 million, compared with $172.16 million a year earlier.

Dynamics of the company's financial results for H1 2024

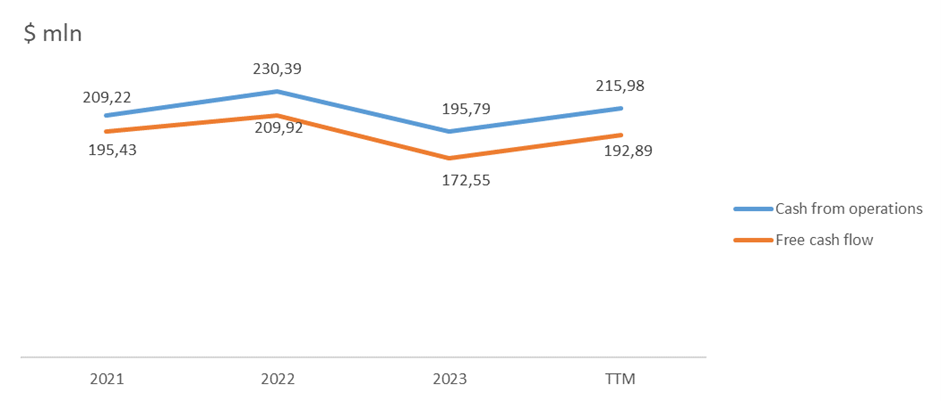

- TTM operating cash flow rose to $215.98 million versus $195.79 million at the end of 2023.

- Free cash flow increased to $192.89 million from $172.55 million.

The increase in operating and free cash flow is mainly attributable to the increase in operating efficiency.

Company cash flow

Rambus has a perfectly healthy balance sheet:

- The debt consists solely of lease obligations and amounts to $30.81 million.

- Cash equivalents and short-term investments accounted for $432.88 million.

This level of debt load indicates excellent financial stability of the company. The high liquidity reserve allows Rambus to develop new projects and participate in M&A transactions without significant external financing.

Stock valuation

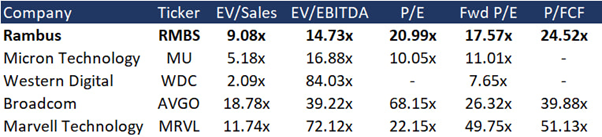

Rambus is trading at a discount to the industry average with EV/Sales at 9.08x, EV/EBITDA at 14.73x, P/E at 20.99x, Fwd P/E at 17.57x and P/FCF at 24.52x.

Comparable estimate

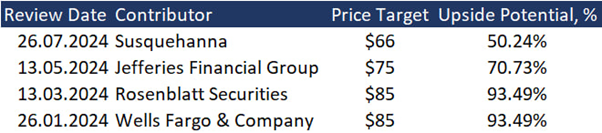

The average price target from the top-4 Wall Street investment banks is $77.8 per share. According to our consensus, the company is undervalued by industry average multiples; the stock’s fair market value is $60.5, which implies a 49% upside potential.

Price targets of investment banks

Key risks

Possible decline in interest in neural networks. The primary growth driver in Rambus' target market is the rapid development of neural networks worldwide. However, if the interest in AI generative models declines, the forecasts for the increase in the production of related computing equipment may materialize in a negative scenario, which could lead to a decrease in investor interest in Rambus.

High competition. Although Rambus has introduced several next-generation products with high scalability potential in the past year, the company may at any time face the introduction of even more efficient products developed by its competitors. If Rambus is unable to continuously improve its products, it could face declining revenues.

Approximately half of Rambus' revenues are derived from licensing agreements that allow customers to manufacture components of chips based on Rambus' architecture. If certain customers refuse to renew their agreements, the company could experience a decline in revenue.