What's the idea?

The crude oil tanker market is expected to face heightened demand and longer routes as a result of geographic demand-supply differences among regions. Another current driver is political instability that reshuffles global fleet routes and contributes to growth of needed charter times. As the average mileage remains at historic highs, oil tanker companies’ revenues will benefit.

Supply of oil tankers remains rigid due to price rise and length of investment cycle in the ship construction industry. The aging fleet contains supply growth as well. Northern American has a strict specialization on Suezmax-type vessels, which contains its operational and maintenance costs and provides operational flexibility.

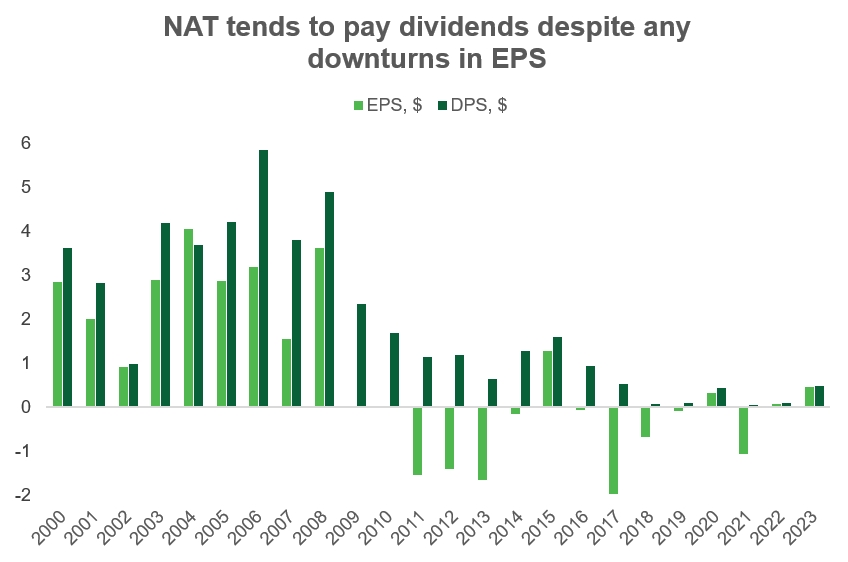

The company targets regular dividend payments, despite its inherent business volatility and manages to pay dividends even in the negative-EPS years. We believe that the stock is overlooked relative to the larger peers and that the current market trends will allow the company stock to grow more this year. In addition, dividend yield will enhance the total stock performance for the investor.

About Company

Nordic American Tankers is a specialized crude oil tanker operator. It runs a fleet of 20 Suezmax-type tankers of approximately the same freight capacity and operates internationally, with prevalent exposure to the spot market or short-term charter as its key business strategy.

The company was incorporated in Bermuda in 1995 and its stock is listed on NYSE.

Why do we like Nordic American Tankers Limited?

Reason 1: Global oil shipment spot prices benefit from global instability, and demand pressure supports them in the longer run

Starting with the long-term demand drivers, we should highlight that in the nearest future Asian countries will be the center of global energy demand growth. Chinese and Indian economies are now the defining force on the oil market, in addition to other countries. In particular, in China coal consumption is projected to stop growing in 2025, while oil consumption peak is expected later on, closer to 2027, and even then demand is not expected to fall rapidly due to wide-spread oil use in petrochemicals, aviation, and shipping.

While most production happens in North America, Middle East and Russia, crude transportation services are going to have a strong fundamental basis in the long-term period.

Returning to near-term, in 2024 oil demand is projected to grow by 1.7 mn b/d, and the source of demand growth are Asian countries. While OPEC+ countries sustain production cuts, non-OPEC producers lying in the Atlantic Basin are expected to increase production by 1 mn b/d, reshaping the marine routes (Source: S&P Global Commodity Insights).

The political instabilities have an impact on another factor: the length of routes. As Russian oil now flows to China and India, instead of a shorter way to Europe, and European countries source the needed crude and products in Saudi Arabia and the US, increase in delivery time is supportive for tanker companies. In addition to this, any further Red Sea trade disruptions will make the tankers spend 40 days on their way from the Middle East to the Mediterranean (via the Cape of Good Hope) instead of the usual 13 days (via Suez canal). (Source: Argus)

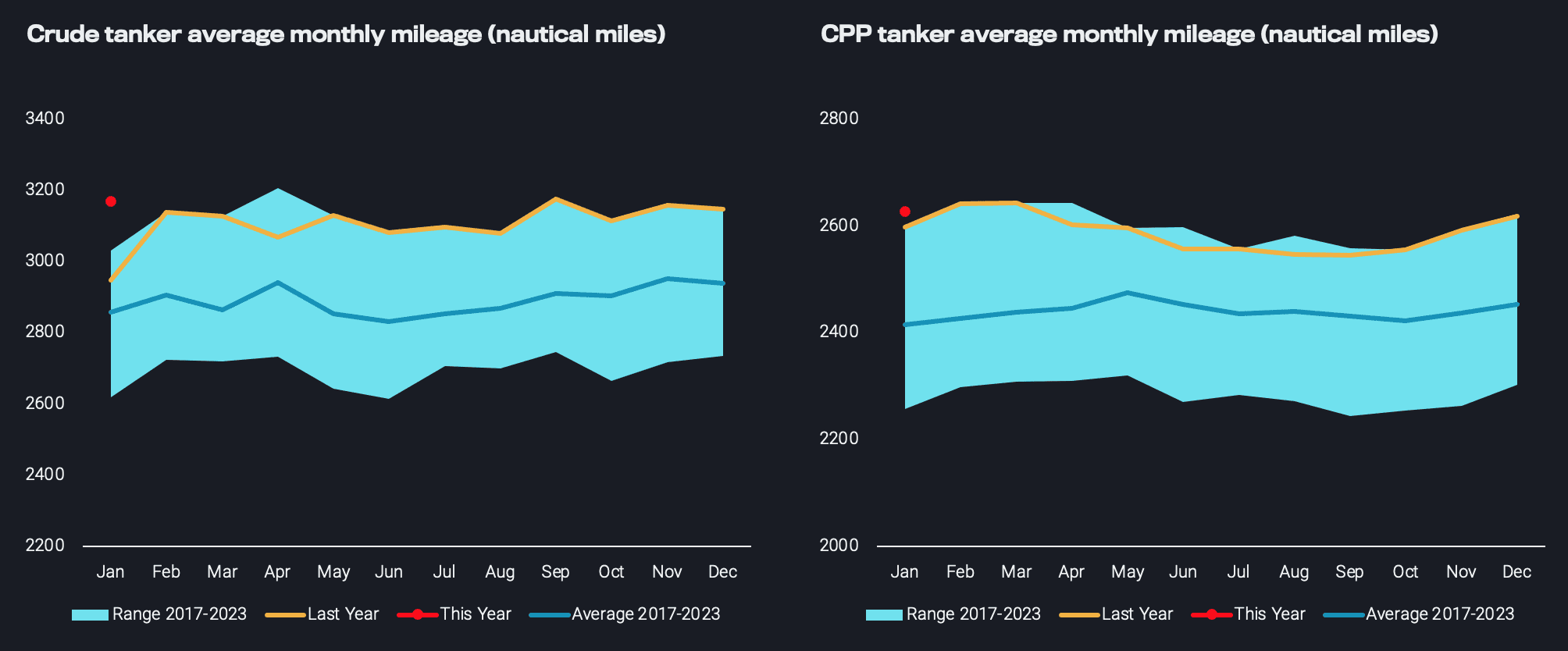

The chart below shows that the average crude tanker mileage has increased since 2017, moreover, the current 2024 mileage is even higher than in the year before.

Citing BIMCO Tanker shipping Market Overview and Outlook, crude tanker demand is expected to grow by 6.5%-7.5% in 2024 and 2%-3% in 2025. (Source: S&P Global Commodity Insights)

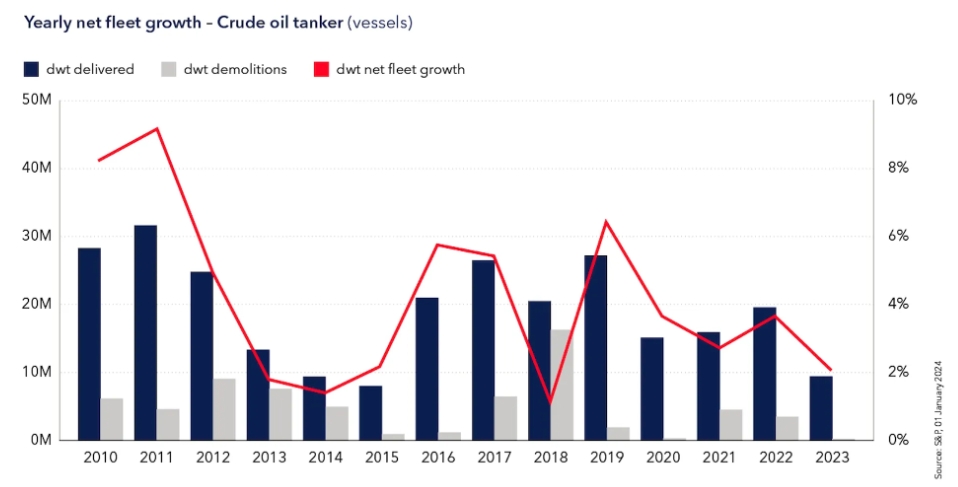

Tanker supply growth remains limited. In 2023 ship deliveries have been on historic lows, with market capacity in dwt adding only 2%, and are expected to reach record low in 2024. Namely, all capacity added in 2024 will be only about 3.6 mln dwt and the fleet will expand by 1%. (Source: Danish Ship Finance, DNV)

It is true that contracting volumes started to rise in 2023, reaching 16 mln dwt, and additional 11 mn dwt were already contracted in 2024. The amount of orders represents 7% of the current fleet. However, it takes 2 or more years to build a tanker.With heightened demand, newbuilding prices have risen by 40-48%, while the price of secondhand vessels has grown between 60% and 210%, as market participants tried to capture the freight prices. The long investment cycle makes supply rigid, and ensures that higher demand results in price rises.

Additionally, as Nordic American Tankers highlights in the Annual report of 2023, basing on Fearnleys’ research, by the end of 2023, about 37% of Suezmax fleet were represented by modern vessels, so the need for replacement capex is constraining the potential supply expansion.

All in all, stale tanker supply and shifts of marine routes create a steady upward pressure on prices and length of routes, both factors generating more revenue for oil tanker companies.

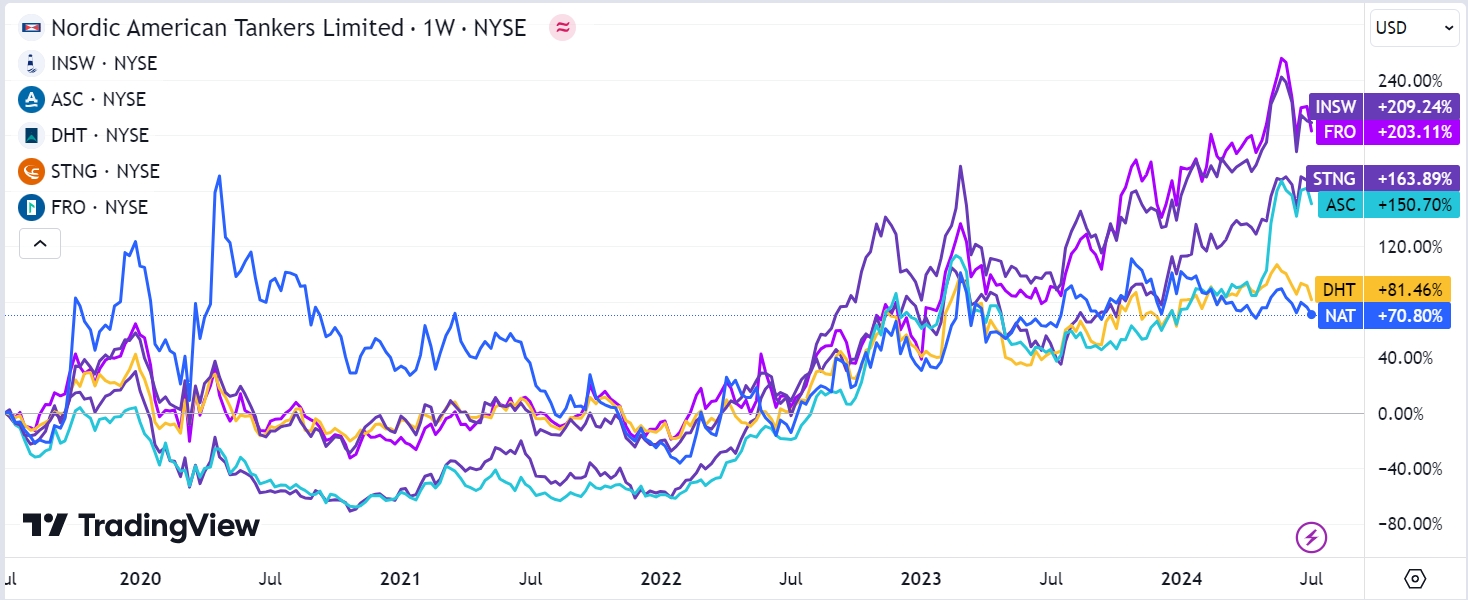

Among the oil transportation stocks we would like to highlight the less-known small-cap Nordic American Tankers company that has not yet realized the full market upswing in its stock price.

Reason 2: A focused business model allows for flexibility and cost optimization

Nordic American Tankers strictly specializes its business on running Suezmax vessels and leaves the fleet mainly open to spot market price swings. Suezmax tankers can carry about 1 million barrels of crude oil and they are flexible as they are proper for long-haul as well as for medium-haul trades. Suezmaxes are applicable for transportation of oil from the Mediterranean, Black Sea, West Africa, South America and Arabian Gulf towards a variety of destinations such as India, Far East, Europe and US.

As all the ships are equal in type and capacity, they are interchangeable and cheaper to operate and maintain, and their breakeven rates are average among the existing ship types. As a result, Nordic American Tankers has an operating cash breakeven rate of $9 000, which it considers low in the industry.

At NAT, out of 20 Suezmaxes only 2 vessels are chartered out on time agreements that expire only in 2028. The charters of another two vessels expire in the latter part of 2024. Occasionally the company charters out its vessels on short-term agreements, but the main amount of capacity remains in the spot market. All in all, prevalence of spot charters imply that all the risk and reward of market spot rate fluctuations rests with the company.

NAT focuses on maintaining relations with “Big Oil companies”, as it calls them, meaning large international and independent oil companies as well as traders. It has some reliance on a single unnamed customer, which provided 11.3% of voyage revenues in 2023 - the share of this client though has contracted from 12.5% in 2021, which we consider a beneficial development.

Reason 3: The company balances inherent volatility of its business by targeting stable dividend payments

Nordic American Tankers’ financial performance is inherently unstable as an exact consequence of its spot-reliant business model. Nevertheless, the company openly declares regular dividend payments as the key point of its capital strategy. As of 1Q 2024 NAT has paid a quarterly dividend since mid-1997 for 107 quarters in a row.

There certainly is a caveat that NAT has made additional equity offerings in the period, but stopped doing so. This is the reason why we would not recommend holding the stock for a very long term, but limit the exposure to 6-9 months.

Since the start of 2024, NAT has already declared two dividend payments sized $0.12 each. Historically, the dividends are not evenly distributed through the year, and median 1H dividends constituted 57% of the total annual sum.

Approximating this way, we can obtain the expected annual sum of $0.4191 per share, which brings the annualized dividend yield to an attractive 10.6% at the current price.

Financial performance

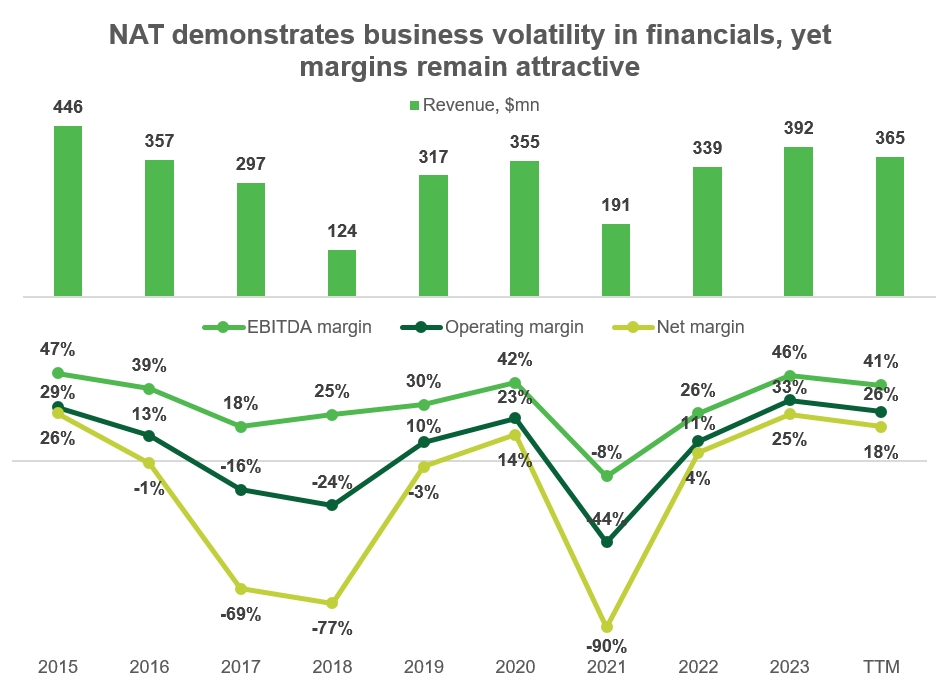

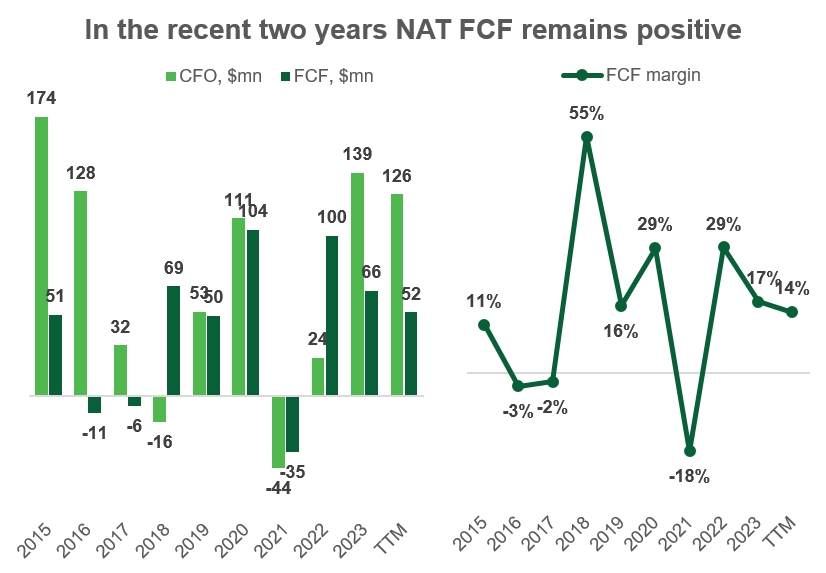

Oil logistics business cannot be called stable, as fluctuations in tanker freight rates can be wide. The company also manages to maintain positive margins and FCF in the past years as rates remain attractive.

We should highlight though that the first quarter performance was not attractive: it showed the inherent business volatility and made the stock price fall. The key TTM metrics are:

- Revenue was $365 mn, down 6.8% from $392 mn in 2023FY.

- Operating income was $96.3 down from $127.9 mn; operating margin contracted from 33% to 26%.

- TTM net income fell to $66.9mn, or 32% from $98.7mn. Net margin lost 7 pp to 18%

The reason was contraction in freight rates below the extremely-high rates in 1Q 2023. Although the effect on revenue was partially mitigated by more vessels in operation, this was not enough to reach the previous level of revenues.

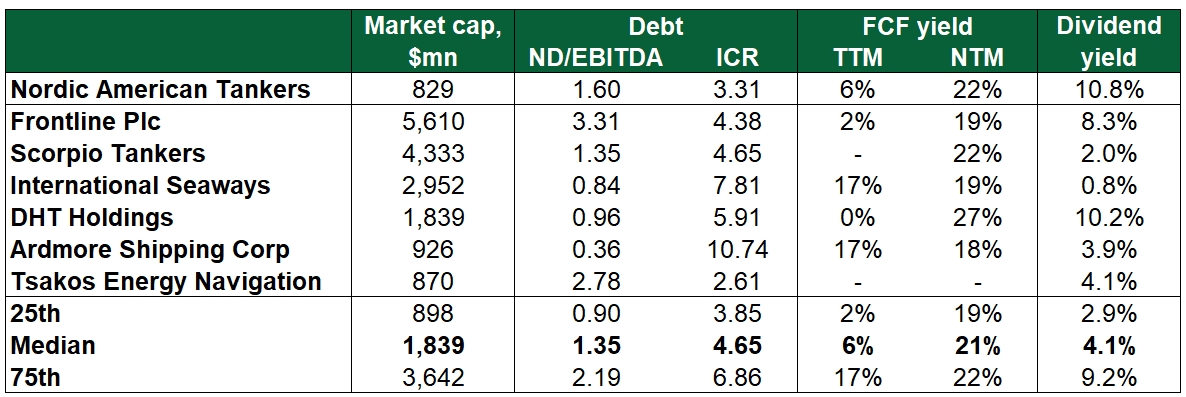

A positive FCF delivers a basis for both dividend payments and debt service. Nordic American holds $293.7 mn of debt, of which $101.5 mn is payable within this year. Cash reserves are $50 mn, and TTM FCF is $52 mn, which allows to cover debt payments, but taking the dividend focus into account - the company will likely refinance.

Overall debt situation looks stable, with Net Debt / EBITDA = 1.6x and interest coverage ratio of about 3.3x. The company holds variable interest debt, which can expose it to interest rate risk in case of adverse moves. On the other hand, the market expectations imply interest rate decrease, which will only be beneficial for future EPS.

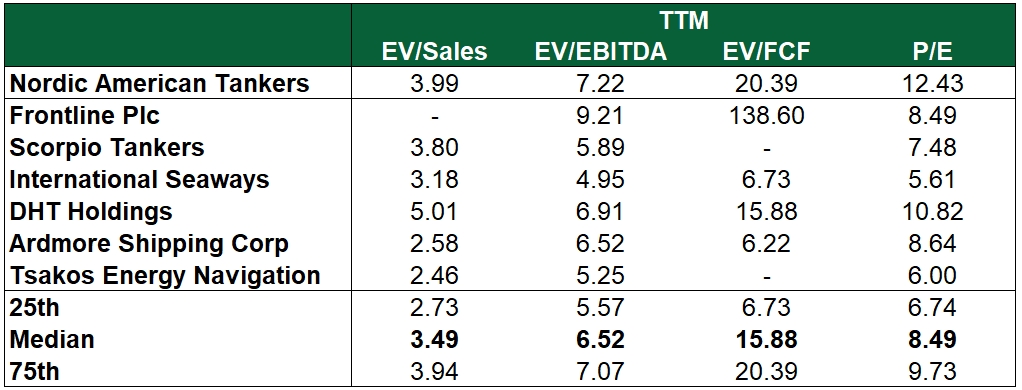

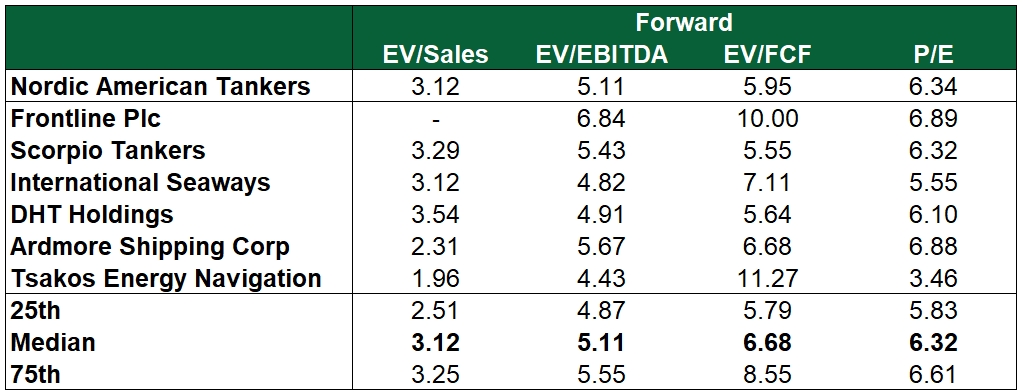

Valuation

Currently NAT stock cannot be called cheap, with almost highest TTM EV/EBITDA and the highest TTM P/E valuations. On the other hand, its forward multipliers are median or lower, showing that the stock is not too expensive relative to the company’s earnings potential. Outstanding is its dividend yield relative to less-paying industry peers.

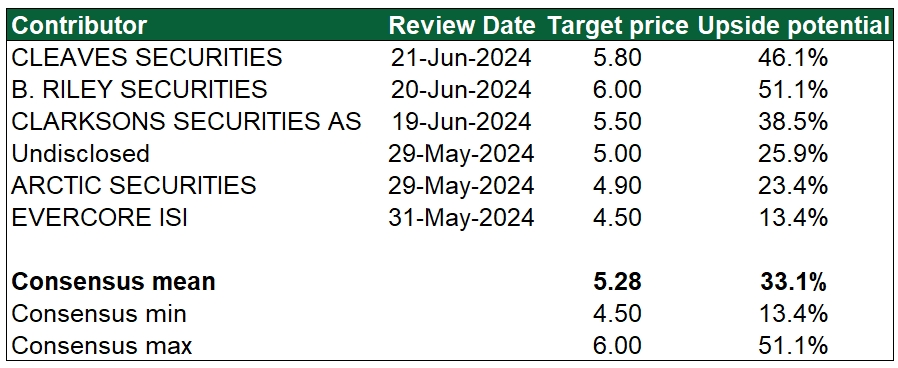

The NAT company is not extensively covered, but all available Wall Street recommendations imply that an upside potential is left in the stock. The average target price is $5.28, implying 40% for the stock, and the range of recommendations is between $4.50 and $6.00 per share. With the current price of $3.97 the upside potential varies from 13.4% to 51.1%.

Key risks

The company has a high spot prices exposure. As oil tanker freight is a turbulent market, in certain moments price volatility in the short term can make a stronger impact on the stock than the long-term supply-demand balance underpinning the market growth potential. Demand growth keeps being supported by regional instabilities and sanctions on Russian oil. Unwinding some of the conflicts earlier than expected can bring to an end the heightened spot prices and lower the company’s attractiveness.

Northern American has a history of attracting equity capital, which can dilute the value of the stock, if it is held long. Operations are held outside the US, and instabilities in some regions represent the risk for the fleet to become the target of terrorist attacks.

Add new comment