What's the idea?

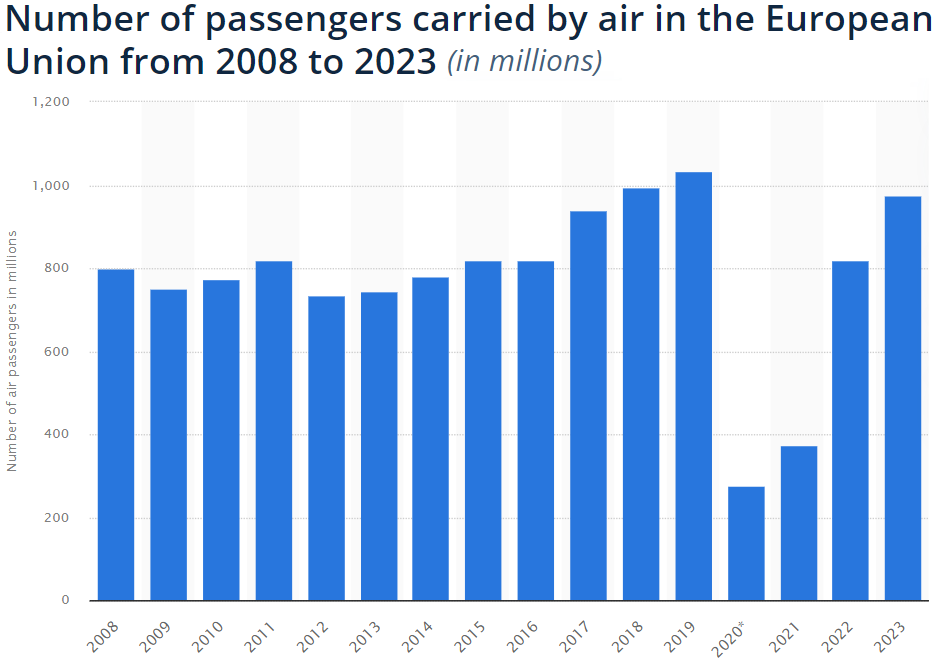

Deutsche Lufthansa AG is one of Europe's leading airline groups. In addition to its own brand, Lufthansa Airlines, the group owns several other airlines, including SWISS, Austrian Airlines, Brussels Airlines and Eurowings. Air passenger transport in the EU reached 976.4 million passengers in 2023, up by 19% year-over-year (YoY). However, the figure remains 5.7% below the pre-pandemic level in 2019. In 2024, passenger traffic in European airports may surpass the 2019 level by 3.2%.

Operationally, Lufthansa faced challenges in Q1 2024, including widespread strikes. Nevertheless, traffic revenue in the Passenger Airlines segment increased by 7% YoY, driving total revenue up by 5% to €7,392 million. Lufthansa has significantly improved its financial position following the Covid-19 crisis, achieving strong liquidity and reducing debt. This has allowed the company to resume dividend payments in 2023, distributing €0.30 per share. For 2024, the potential dividend yield could be around 4.1%–4.9%.

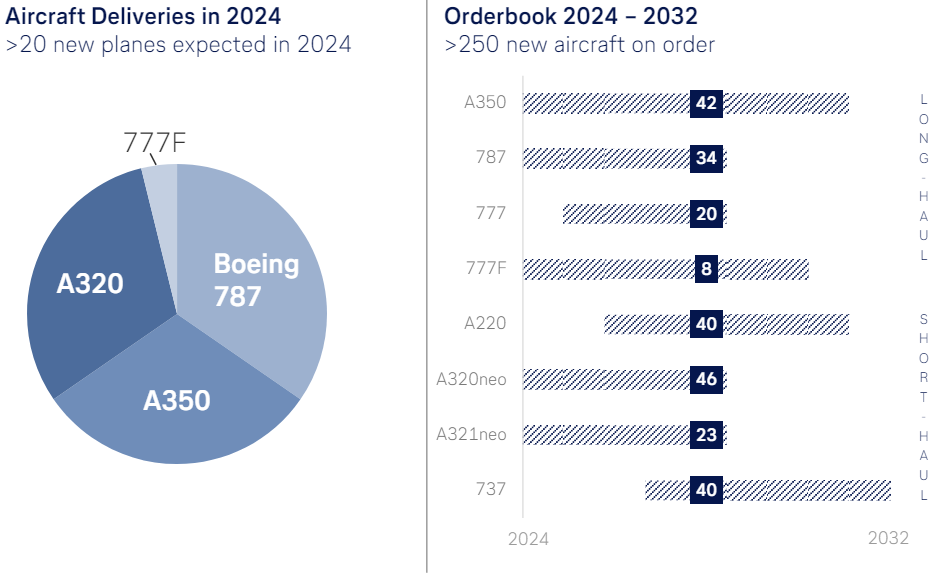

Despite certain short-term challenges, Lufthansa remains committed to creating value for shareholders through dividend payments and an ambitious fleet modernisation strategy. The company plans to significantly expand its fleet by 2032, with more than 250 new aircraft on order, representing a 35% increase over the current fleet size.

About Company

Deutsche Lufthansa AG (LHA) is engaged in the provision of passenger, freight and air transport services. In addition to its own brand, Lufthansa Airlines, the company owns several other airlines, including SWISS, Austrian Airlines, Brussels Airlines and Eurowings. Together with its subsidiaries, Lufthansa ranks second in Europe in terms of passengers carried. The company was founded in 1926 and is headquartered in Cologne, Germany.

Why do we like Deutsche Lufthansa AG?

Reason 1. Passenger traffic recovery in European airports drives operating results

Deutsche Lufthansa AG (LHA) is engaged in the provision of passenger, freight, and air transport services. In addition to its own brand, Lufthansa Airlines, the Lufthansa Group owns several other airlines, including SWISS, Austrian Airlines, Brussels Airlines and Eurowings. This makes it one of Europe's leading airline groups: together with its subsidiaries, Lufthansa ranks second in Europe in terms of passengers carried.

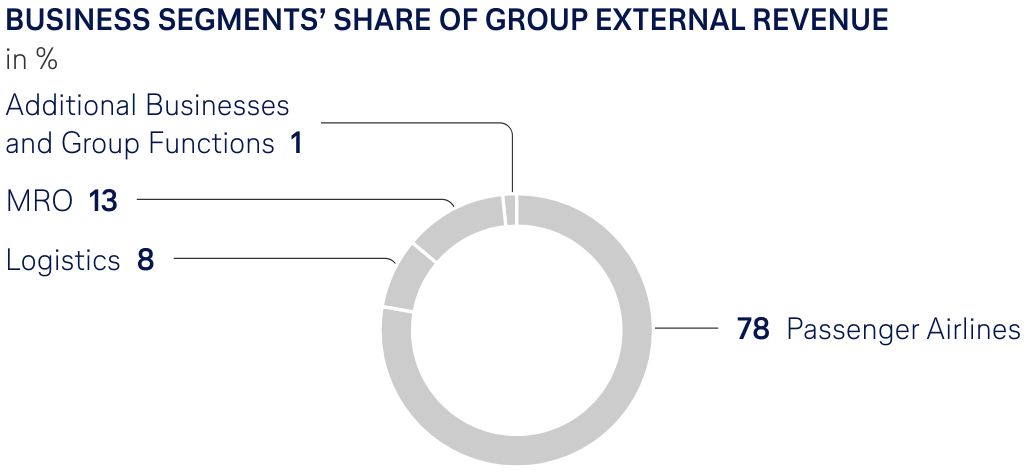

Most of Lufthansa's revenue comes from the Passenger Airlines segment, which accounted for 78% of total revenue in 2023. The Maintenance, Repair and Overhaul (MRO) segment contributed 13%, Logistics 8% and Other Businesses and Group Functions 1%. Geographically, Lufthansa generates most of its revenue from flights in Europe and the US, with Europe contributing 63.7% and the US 17.0% of 2023 revenue, for a total of 80.7%.

Lufthansa’s revenue breakdown by business segment

According to Statista, air passenger traffic in the EU reached 976.4 million passengers in 2023, a significant increase of 19% compared to 2022. However, the figure remains 5.7% below the pre-pandemic level of 2019. The ongoing impact of the coronavirus pandemic, the cost-of-living crisis, as well as increasing energy and jet fuel prices have combined to put pressure on both airlines and passengers.

Moreover, ACI EUROPE, which publishes a monthly Airport Traffic Report that compiles data from over 450 member airports representing more than 95% of European airport traffic, recently forecast that passenger traffic at European airports in 2024 will be 3.2% higher than in 2019. This is a significant improvement on the October 2023 forecast of 1.4%. The upward revision is attributed to strong traffic in the last two quarters, a shift in consumer behavior with increased demand from Visiting Friends & Relatives (VFR), and continued capacity expansion by ultra low-cost carriers and full-service carriers.

However, performance at the country level remains fragmented, with some countries exceeding pre-Covid forecasts while others lag behind. Several factors, including economic problems, geopolitical risks, social unrest (strikes) and delays in aircraft deliveries and spare parts shortages, could lead to the pessimistic scenario of passenger traffic growth of only 1.4% in 2024.

Number of passengers carried by air in the EU

Driven by the continued recovery in flight demand in the EU, Lufthansa's operating performance improved significantly over 2023. However, in Q1 2024, the operating and financial performance deteriorated YoY, primarily due to widespread strikes by various employee groups within the company and at system partners in Germany. The strike ended in April 2024, when Lufthansa and the flight attendants' union UFO agreed a pay rise for the airline's 19,000 cabin staff. Employees will receive a 16.5% total pay rise in three stages, as well as an inflation compensation bonus of €3,000 and an increase in other allowances. The agreement runs until the end of 2026.

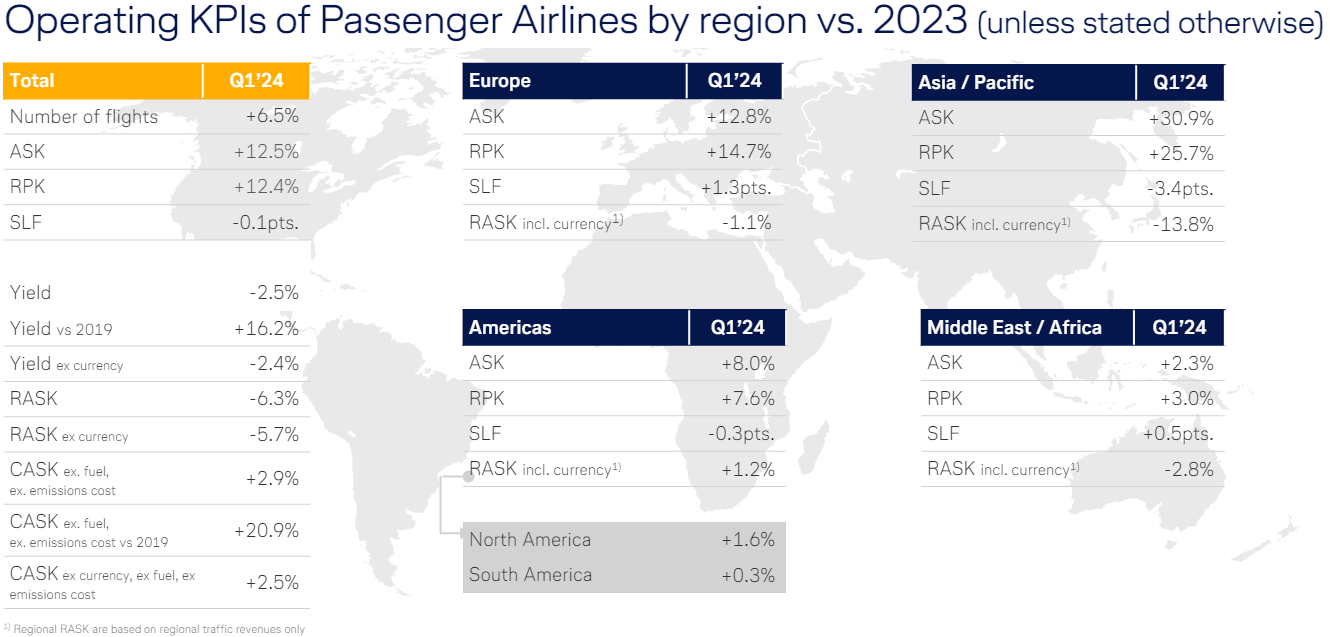

Nevertheless, the capacity offered by Passenger Airlines in Q1 2024 was 12% higher than in the previous year, reaching 84% of its pre-crisis level in 2019. The number of flights increased by 6.5% YoY, with Available Seat Kilometres (ASK) up by 12.5% compared to the same period in 2023. Revenue Passenger Kilometres (RPK) also grew by 12.4% YoY, and the passenger load factor remained stable at 79.7%.

The Logistics segment's operating performance declined in Q1 2024 due to a challenging airfreight market, strikes, and a strong comparison base from the previous year. Capacity increased by 7% YoY, primarily due to the expansion of passenger flight operations and the resulting rise in belly capacities. Sales grew by 10% YoY, and the cargo load factor improved by 2.1 percentage points to 63.3% (versus 61.2% in Q1 2023). However, yields fell across all of Lufthansa's traffic areas, decreasing by 25% overall compared to the previous year.

Besides, Lufthansa Technik (MRO segment) saw an increase in Q1 2024 revenue due to the continued rise in flight numbers, leading to higher demand for maintenance and repair services. Consequently, the segment’s revenue grew by 15% YoY to €1,770 million, or €1,188 million excluding revenue with companies of the Lufthansa Group. However, work stoppages due to strikes negatively impacted revenue development.

Q1 2024 operating results of Lufthansa’s Passenger Airlines segment

The 2024 operational and financial outlook for Lufthansa is subject to a high degree of uncertainty due to short booking cycles in the passenger business, a freight business driven mainly by the spot market, and uncertainties in the macroeconomic and geopolitical environment. Despite these challenges, the management expects strong demand in 2024, leading to continued sales growth. Demand in the private travel segment is forecast to exceed pre-crisis levels, and there is anticipated further recovery in business travel demand. As a result, flight capacity is planned to be expanded, with overall available capacity for Passenger Airlines expected to reach around 92% of its pre-crisis level of 2019.

In the long term, Lufthansa's operational business is poised for significant expansion due to the largest fleet modernization in its history. Lufthansa Group's order book for 2024–2032 includes over 250 new aircraft, representing a 35% increase compared to 721 aircraft as of December 31, 2023. In 2024, the airlines within the Lufthansa Group anticipate receiving up to 30 new aircraft. However, this target may face challenges due to production issues and delays in certification. The aviation industry has experienced repeated postponements in planned aircraft deliveries, leading to uncertainties in the company's capacity forecast despite already reducing initial assumptions.

Lufthansa's order book for 2024–2032

Reason 2. Strong financial results overshadowed by strikes and lower cargo yields

In Q1 2024, Lufthansa posted overall strong results, despite being impacted by strikes from various employee groups within the Lufthansa Group and its system partners, which led to outcomes lower than expected. Traffic revenue in the Passenger Airlines segment increased by 7% YoY, reaching €5,146 million, up from €4,806 million the previous year, largely due to the rise in traffic. Conversely, traffic revenue in the cargo business declined by 16% to €757 million, down from €902 million in the previous year, primarily due to lower yields.

As a result, total traffic revenue at Lufthansa Group airlines rose by 3% to €5,903 million in Q1 2024, compared to €5,708 million in Q1 2023. Additionally, other revenue saw a significant increase of 14%, reaching €1,489 million, up from €1,309 million, driven by higher business activities and increased income in the MRO business segment. Consequently, total revenue, which includes both traffic revenue and other revenue, rose by 5% to €7,392 million.

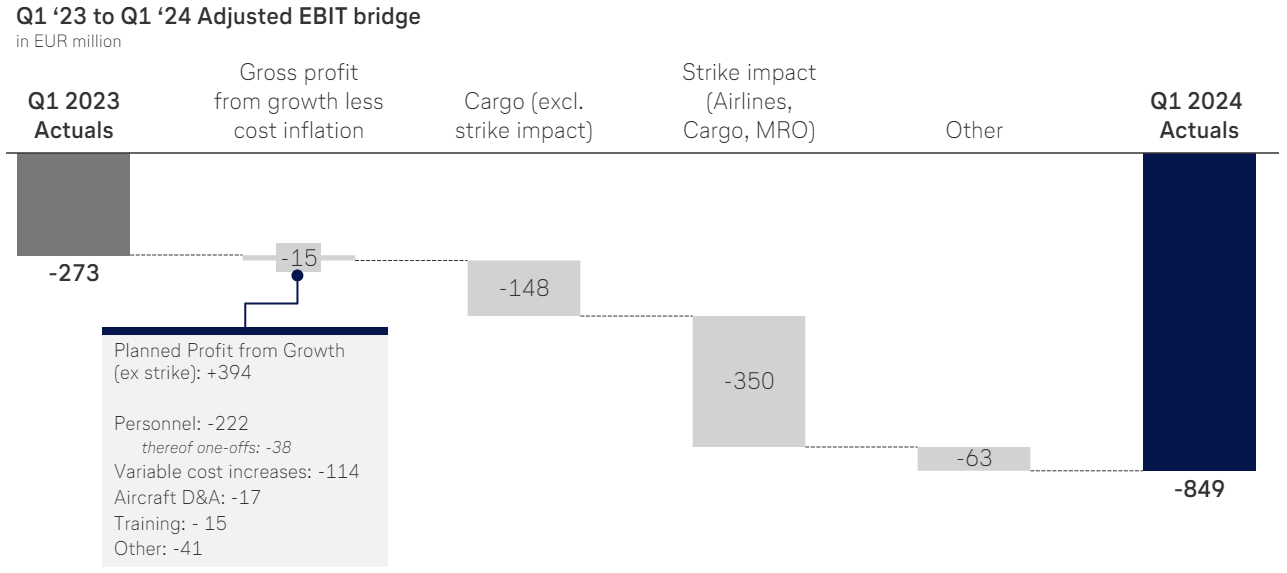

Lufthansa’s Q1 2023 to Q1 2024 adjusted EBIT bridge

However, Lufthansa's adjusted EBIT fell to € -849 million in Q1 2024, compared to € -273 million a year earlier, primarily due to strikes at various Lufthansa Group companies and external system partners, which had a direct and indirect negative impact on earnings of around €350 million. Consequently, the adjusted EBIT margin decreased to -11.5%, down from -3.9% in the previous year.

The management anticipates that revenue growth in 2024 will be offset by ongoing cost inflation. Furthermore, the additional strain caused by various strikes during Q1 2024 is expected to lead to a YoY decline in earnings. Overall, the management projects a FY2024 adjusted EBIT of around €2.20 billion, representing a 22% decline compared to €2.68 billion in 2023. Despite these challenges, Lufthansa remains committed to its goal of achieving a sustainable adjusted EBIT margin in excess of 8%.

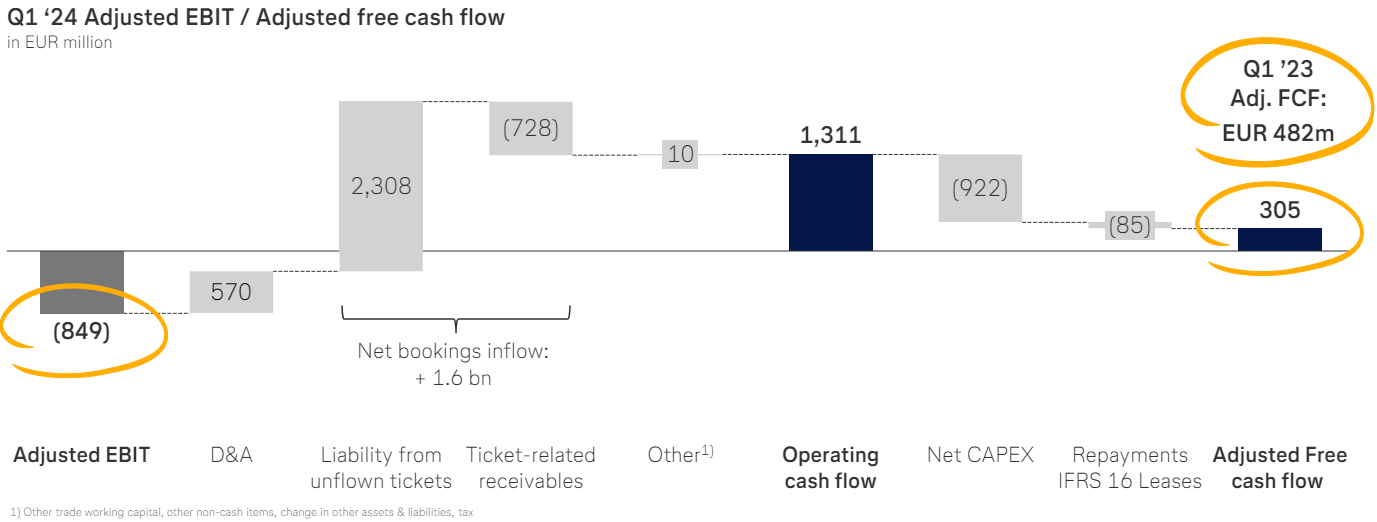

Lufthansa’s Q1 2024 adjusted FCF conversion

Despite negative operating results, Lufthansa generated a positive operating cash flow of €1,311 million in Q1 2024. However, this was 17% below the prior-year level of €1,581 million, primarily due to a decrease in EBITDA. Additionally, adjusted free cash flow remained positive at €305 million but fell by 37% compared to €482 million the previous year. Inflows from advance ticket payments, in particular, compensated for the negative result.

Reason 3. Resumption of dividend payments and low valuation

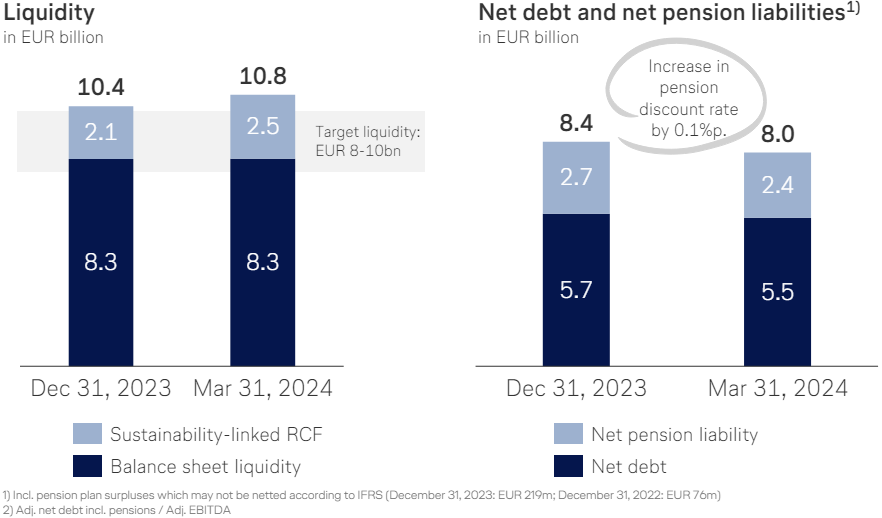

Despite short-term challenges, Lufthansa has significantly improved its financial health since the Covid-19 crisis and its aftermath for airlines. As of March 31, 2024, balance-sheet liquidity, comprising cash, current securities, and fixed-term deposits, totaled €8.27 billion. In addition, the company had unused credit lines amounting to €2.55 billion, bringing total available liquidity to €10.82 billion, up from €10.36 billion as of December 31, 2023.

Moreover, as of March 31, 2024, total debt decreased to €13.80 billion, down 17.3% from its peak of €16.69 billion in 2021. With €8.27 billion in cash and short-term investments, net debt stood at €5.53 billion, which is 38.7% lower than in 2021. Besides, the current net debt/EBITDA ratio is 1.33x, an improvement over the pre-pandemic level of 1.52x in 2019.

Lufthansa’s liquidity and debt metrics

A strong balance sheet has enabled Lufthansa to resume dividend payments. According to the company’s dividend policy, it aims to distribute 20% to 40% of net profit, adjusted for non-recurring gains and losses, to its shareholders. A key condition for dividend payment is that the net profit for the year, as shown in the individual financial statements of Deutsche Lufthansa AG prepared under German commercial law, must allow for the relevant distribution.

For 2023, Lufthansa paid its shareholders a dividend of €0.30 per share, representing a total dividend of €359 million, or 21% of the net profit for 2023. This resulted in a dividend yield of 3.7%, based on the Lufthansa share’s closing price for the year.

In 2024, Lufthansa’s margins are expected to be lower compared to 2023, with trailing twelve months’ (TTM) net margin as of Q1 2024 standing at 3.9%. If this margin is sustained by the end of 2024, net income could reach €1.40 billion for the full year. With a distribution ratio of 20% to 40%, this would result in a total dividend of €280 to €560 million. At the lower end of this range, the dividend per share would be €0.23, leading to a 4.1% dividend yield relative to the current stock price.

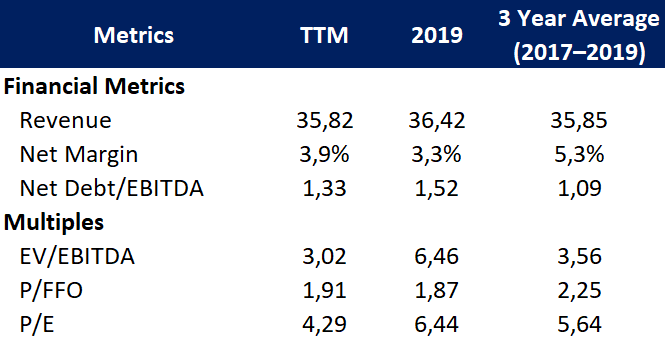

While Lufthansa has achieved its pre-pandemic operating and financial results, the company is currently valued more cheaply compared to historical multiples:

- TTM EV/EBITDA ratio stands at 3.02x, significantly lower than the 6.46x seen in 2019 and the three-year average of 3.56x from 2017 to 2019.

- TTM P/FFO ratio is 1.91x, slightly below the 1.87x in 2019 and the three-year average of 2.25x from 2017 to 2019.

- TTM P/E ratio is 4.29x, compared to 6.44x in 2019 and the three-year average of 5.64x from 2017 to 2019.

Comparison of Lufthansa’s selected historical financial metrics and multiples

This lower valuation is partly explained by the dilution of shareholders' stakes. During the Covid-19 crisis in 2020–2021, Lufthansa had to issue additional shares to avoid bankruptcy, which led to a 150% increase in the number of outstanding shares, from 478.2 million in 2019 to 1,196.6 million in Q1 2024. This significant increase in shares has diluted shareholders' equity.

However, despite this dilution, Lufthansa remains financially sound, maintains good margins and aims to create value for shareholders through the resumption of dividend payments and plans to realize an ambitious fleet modernisation strategy.

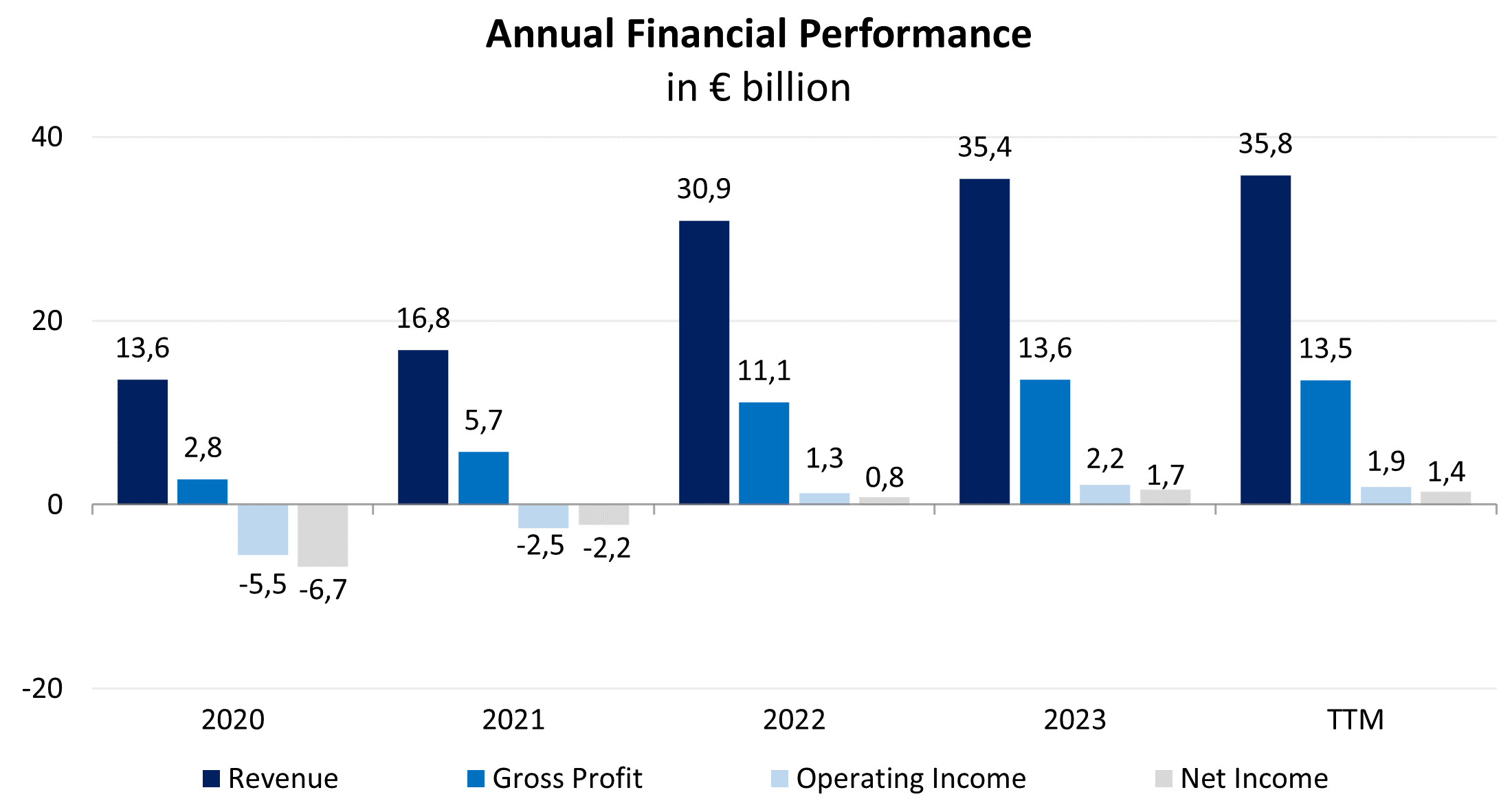

Financial performance

Lufthansa’s TTM financial results can be summarized as follows:

- Revenue increased to €35.82 billion, up by 1.1% compared to 2023.

- Gross profit slightly declined by 0.4%, from €13.58 billion in 2023 to €13.53 billion TTM, with gross margin decreasing from 38.3% to 37.8%.

- Operating income declined by 13.2% and accounted for €1.90 billion. Operating margin worsened from 6.2% to 5.3%.

- Net income plummeted by 16.0%, from €1.67 billion in 2023 to €1.41 billion TTM. Net margin decreased from 4.7% to 3.9%.

Revenue increased largely due to the rise in passenger traffic, higher business activities and increased income in the MRO business segment. However, as mentioned previously, the company’s margins were negatively impacted by widespread strikes in Germany.

Dynamics of annual financial results

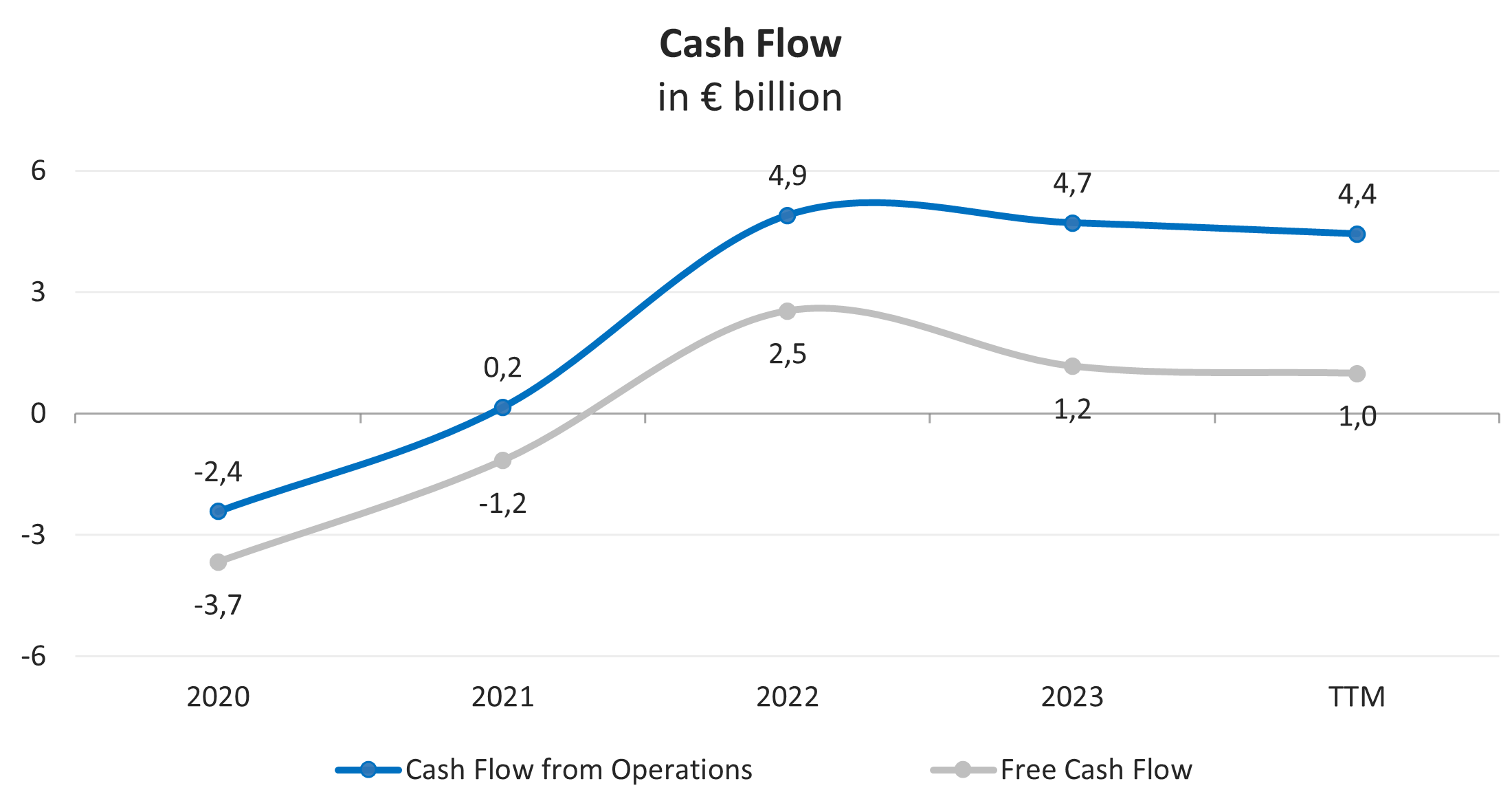

Lufthansa’s cash flows have rebounded from the deep witnessed in 2020 and are maintained at stable levels. Its TTM operating cash flow (FFO) accounted for €4.44 billion, down by 5.8% compared to 2023, largely because of decreased net income. Free cash flow (FCF)decreased by 15.3%, from €1.17 billion in 2023 to €0.99 billion TTM.

Dynamics of annual financial results

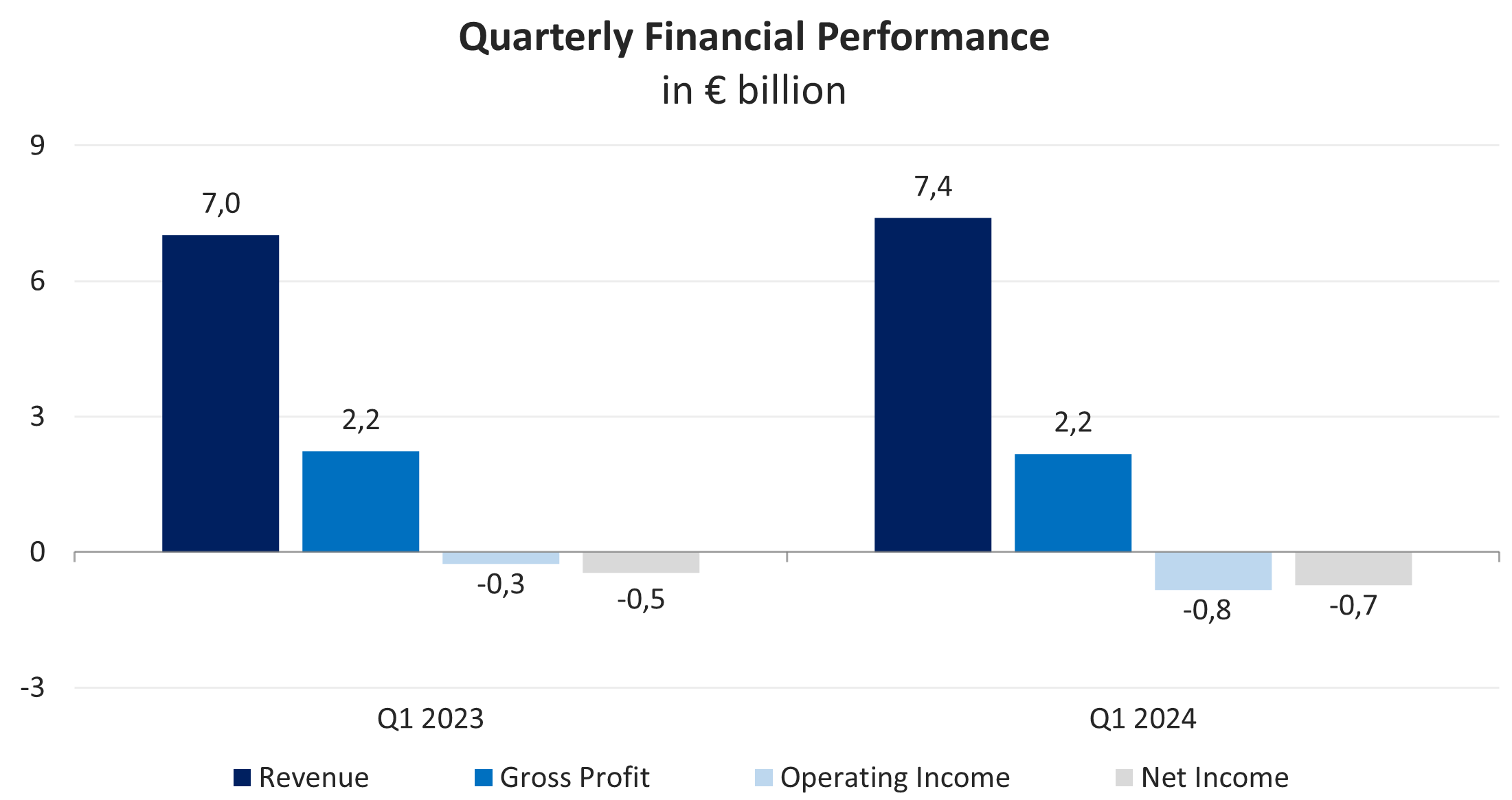

Lufthansa’s financial performance for Q1 2024 is presented below:

- Revenue increased by 5.3% YoY, from €7.02 billion to €7.39 billion.

- Gross profit decreased by 2.4% YoY, from €2.23 billion to €2.17 billion.

- Operating loss rose YoY, from € -0.26 billion to € -0.84 billion.

- Net loss also worsened YoY, from € -0.47 billion to € -0.73 billion.

Dynamics of quarterly financial results

Lufthansa maintains a robust balance:

The leverage ratio, defined as the ratio of total debt to assets, stands at 29%, which is much better than the industry average of 40%. As of March 31, 2024, total debt accounted for €13.80 billion, down by 1.0% compared to the end of 2023. With reported cash and short-term investments of €8.27 billion, net debt accounts for €5.53 billion.

The company earned €4.15 billion of TTM EBITDA, and, consequently, the net debt to EBITDA ratio equals 1.33x. This proves that the company is financially healthy and is not likely to face credit risk in the foreseeable future. TTM interest expenses increased by 19,5% to €0.61 billion compared to 2023. With TTM EBIT of €1.90 billion, interest coverage ratio amounts to 3.13x.

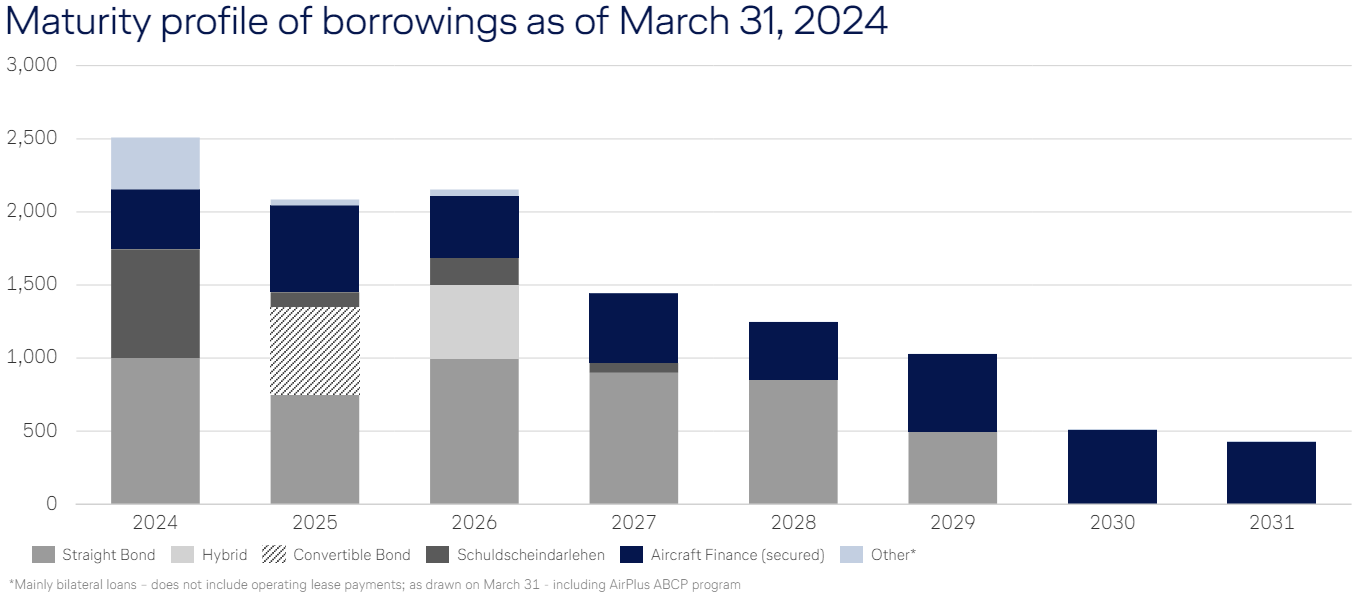

The company has to pay off around €6.6 billion of debt maturities in 2024–2026, which is approximately 48% of its total debt. However, there is enough cash on the balance sheet and generated cash flows to cover future debt payments.

Maturity profile of Lufthansa's borrowings

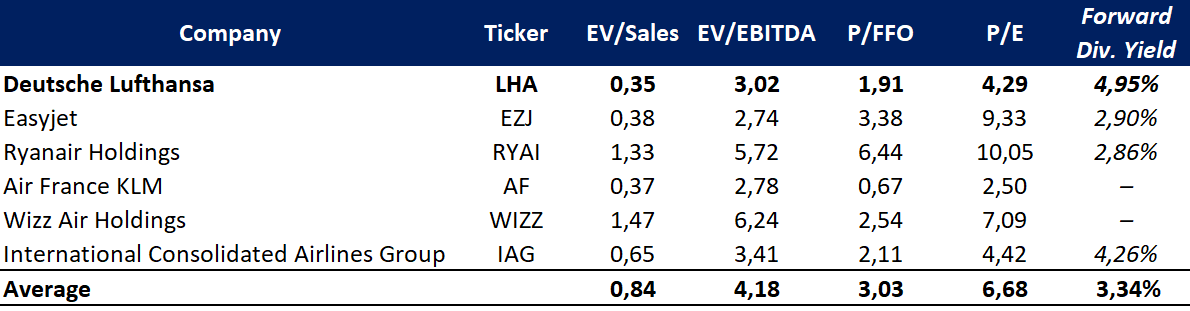

Stock valuation

Lufthansa trades at a discount to its peers based on the average multiples: EV/Sales — 0.35x, EV/EBITDA — 3.02x, P/FFO — 1.91x, and P/E — 4.29x. However, the company demonstrates strong operating and financial results, has resumed dividend payments and has promising growth opportunities once fleet modernization plans are realized. Thus, it offers better return per unit of risk taken.

Comparable valuation

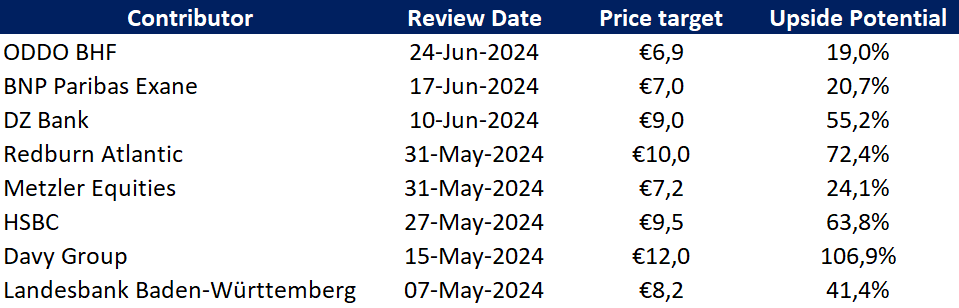

The minimum price target set by ODDO BHF is €6.9 per share, while Davy Group values Lufthansa at €12.0 per share. According to the Wall Street consensus, the stock’s fair market value stands at €8.0, implying a 34.1% upside potential.

Price targets of investment banks

Key risks

Lufthansa's forecast for 2024 is based on the assumption that future macroeconomic conditions and industry developments will be in line with its forecasts. If the global economy performs worse than forecast, this is expected to have a negative impact on the company's business. The growth of the aviation sector is highly dependent on the global political situation and correlates with macroeconomic developments. Ongoing changes in demand related to the Covid-19 pandemic, military conflicts and the impact of the climate debate mean that long-term market growth may be lower than in the past.

Supply-side bottlenecks, such as limited infrastructure and supply chain constraints, also slow down air traffic. In addition, problems experienced by aircraft manufacturers may lead to delays in the delivery of orders placed by Lufthansa. There is a general risk of labor disputes as a result of pending collective bargaining agreements with various groups of employees within Lufthansa. While a long-term collective agreement has been concluded with the pilots' union Vereinigung Cockpit for the cockpit crews of Deutsche Lufthansa AG and Lufthansa Cargo, the risk of strikes is higher in the flight operations of Eurowings Germany, Lufthansa Cityline and Discover Airlines.

Lufthansa is increasingly exposed to risks arising from problems with materials in components of Pratt & Whitney PW1000G engines. The impact extends to the Airbus A320neo and Airbus A220 fleets. For the airlines in the Lufthansa Group that use these engines, this problem entails the risk of operational disruptions, a shortage of spare parts and higher maintenance costs.