What's the idea?

Stable high oil prices have sparked renewed interest in offshore projects, particularly in deepwater hydrocarbon exploration and production, driving long-term demand for related services. Helix Energy offers a suite of services that are in demand with increasing capital and operating expenditures in the offshore industry. The company provides complementary and diversified services to both the oil and gas and renewable energy industries.

Increased capital expenditures by customers for production enhancement and trenching provide a strong growth impetus for the company's two main segments, boosting both revenue and operating margins. Management notes the long-term nature of the trends observed, supported by a solid order book. The discount at which Helix Energy’s stock is trading reflects the company's protracted recovery from a period of low capital expenditures in the offshore industry, as well as the current difficulties faced by the decommissioning segment, which is putting pressure on margins. As the long-term capex trend in the sector strengthens, margins are expected to improve, which will be reflected in the company's valuation.

Revenue growth driven by freight rate increases and an expanding order backlog, along with the company's limited capital expenditure requirements and low valuation multiples, make Helix Energy an attractive investment.

About Company

Helix Energy Solutions (HLX) provides services for offshore oil and gas and renewable energy projects. The company specializes in well work to enhance production, as well as services related to construction, repair and maintenance, trenching, and more recently, decommissioning and abandonment. Helix Energy owns a fleet of specialized vessels and equipment that it also leases to its clients. The company operates globally, generating approximately 50% of its revenues in the US.

Why do we like Helix Energy Solutions Group Inc?

Reason 1: New cycle of investment in the offshore industry

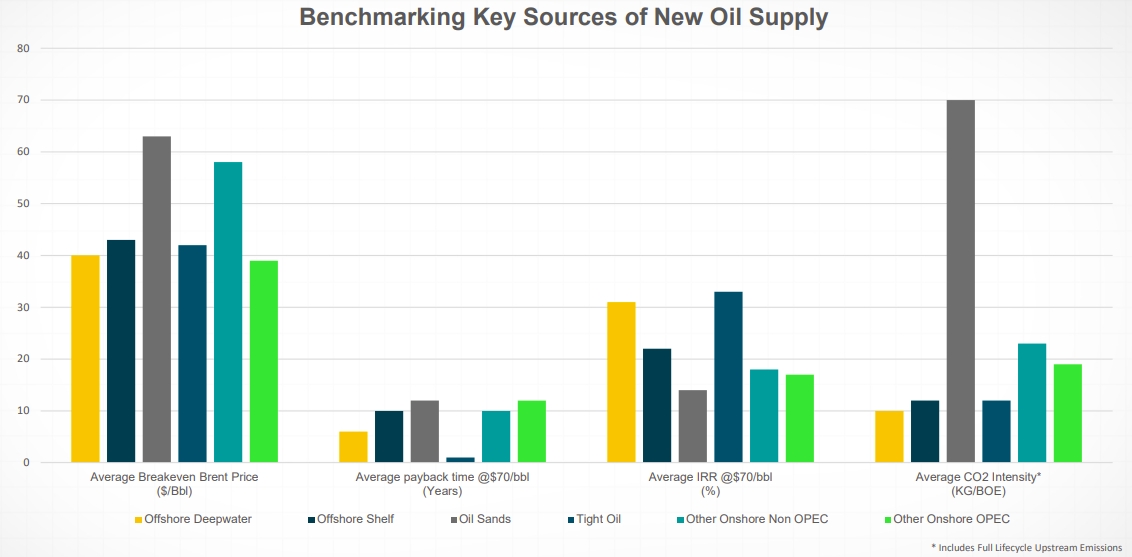

Offshore drilling companies have gone through several difficult periods over the past decade, especially in 2015–2016 and 2020, when oil prices plummeted, leading to the bankruptcy of many market players. Following a severe consolidation in the industry, companies have emerged from the crisis with a stronger financial position, and the current oil price is creating an attractive environment for a new investment cycle. With oil prices above $70 per barrel, even investments in deepwater projects can pay off in six years. S&P Global forecasts that exploration and production (E&P) investment for offshore projects will reach 35% of total E&P spending, above the historical average of 30%.

Besides oil prices, several other factors support the industry's current situation:

Partial shift of priorities from US shale oil projects with a short life cycle and an average annual production decline rate of 35%–40% to offshore projects with a long life cycle, where the production decline rate is 10%–15%. The discovery of large resource-rich fields such as Stabroek in Guyana and Mopane in Namibia, which are estimated to have particularly attractive cost profiles.

Lower carbon emissions from deepwater projects compared to production of hard-to-recover oil, which reduces risks in case of possible tightening of environmental regulations. The average break-even point for new deepwater fields is about $40 per barrel of Brent, and the internal rate of return (IRR) can exceed 30% at an oil price of $70.

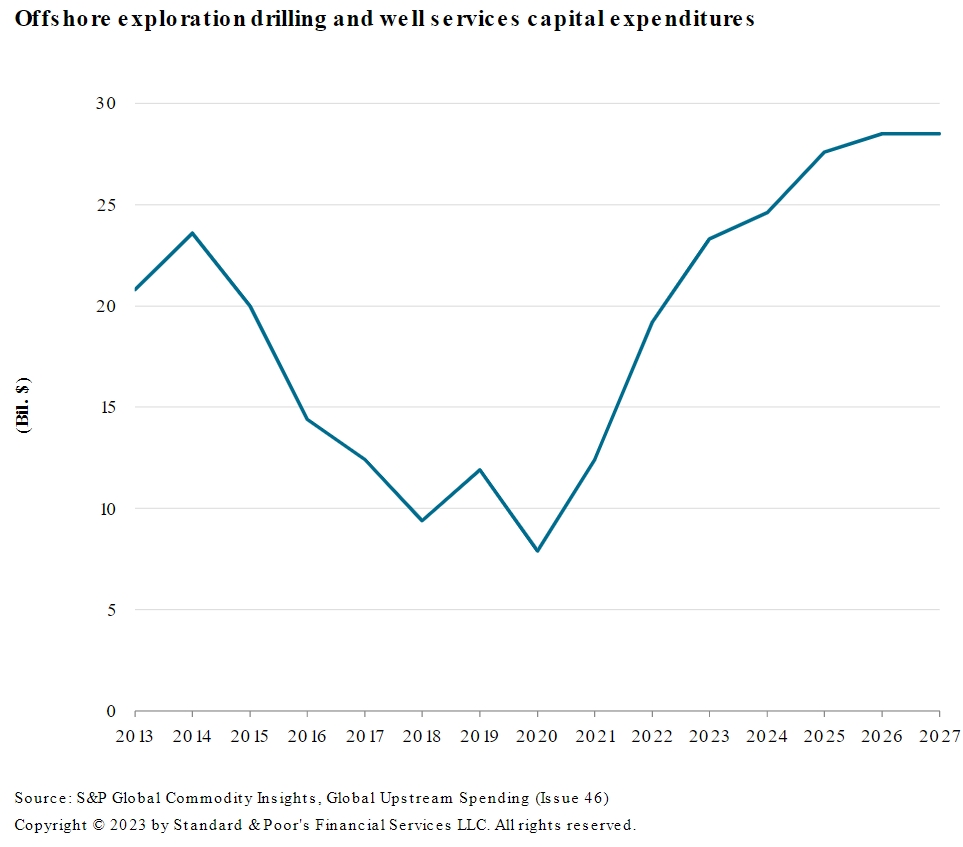

According to a recent Rystad Energy review, capital expenditures associated with deepwater drilling projects will peak in 2024 and continue to rise to $130.7 billion by 2027, up 30% from 2023 levels.

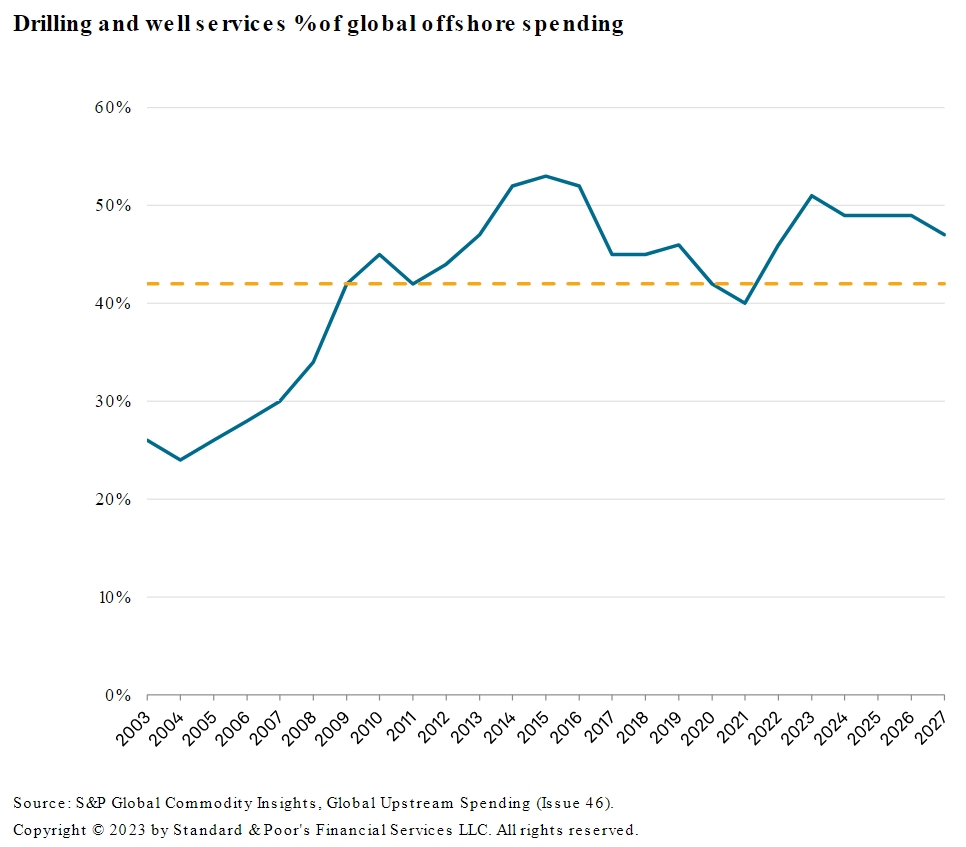

While it is difficult to predict the profitability of such developments, it is possible to speculate which companies will benefit from increased capital investment in offshore projects. In particular, drilling and servicing costs are estimated to account for 51% of offshore investment in 2023 and remain high compared to the historical average of 42% until at least 2027.

Reason 2: Broad range of services to the offshore industry and upturn in core businesses

Helix Energy provides services for offshore oil and gas and renewable energy projects. The company specializes in well life extension, end-of-life decommissioning of oil and gas fields, and provides various types of support during construction, repair, and maintenance activities. The Company divides its operations into four segments:

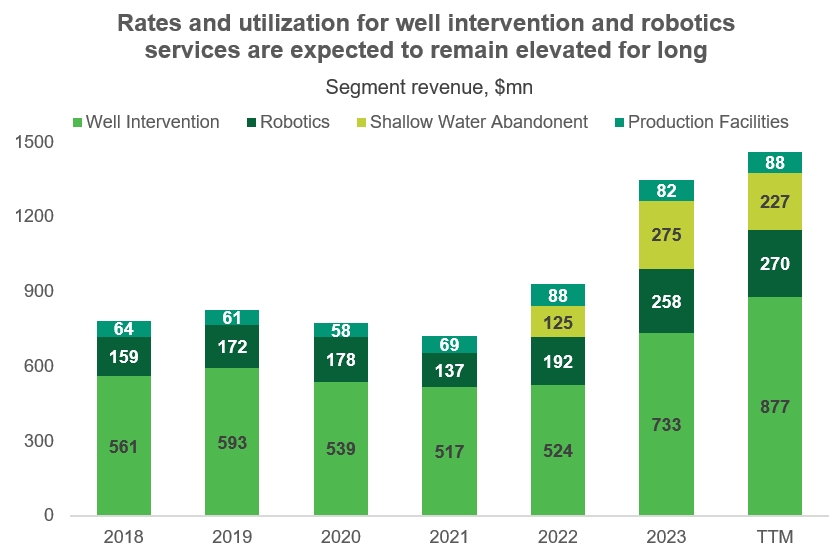

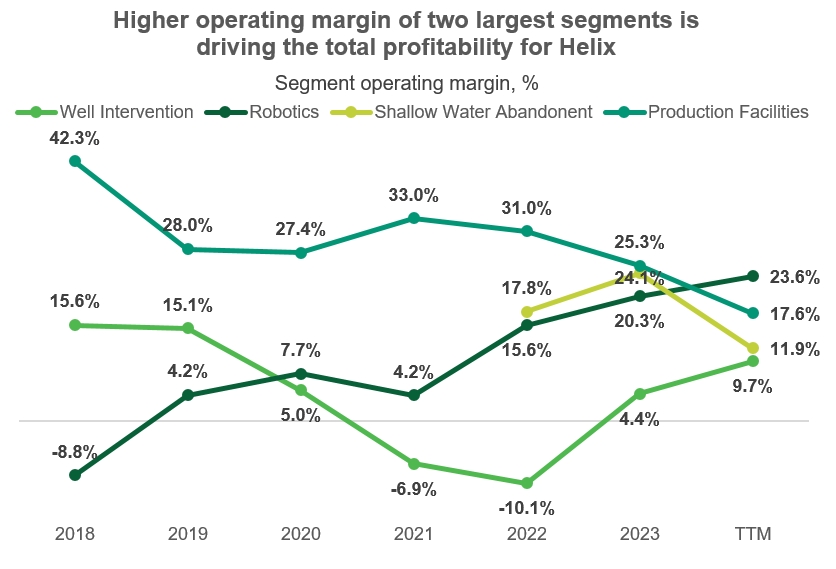

Well Intervention — This segment focuses on activities that enable customers to improve the performance of subsea wells or decommission them. The company's customers benefit from the ability to extend well life and production and avoid the need for new drilling, which is more costly. In addition, such work minimizes oil and gas spills. Helix Energy operates seven well intervention vessels, as well as specialized equipment, such as risers and subsea lubricators, which can be provided separately to customers. This segment accounted for 60% of the company's revenue in the last 12 months.

Robotics — This business segment covers seabed clearing, trenching, offshore construction, as well as inspection, repair and maintenance. These services are in demand in both the oil and gas industry and the renewable energy sector, which accounts for more than 50% of the segment's revenues. Core services are provided using remotely operated vehicles, trenchers, and other robotic equipment and vessels, which are also rented as a separate service. This segment generates approximately 18% of revenues.

Shallow Water Abandonment is Helix Energy's new business line following its 2022 acquisition of Alliance, a company specializing in well decommissioning services in the shallow waters of the Gulf of Mexico. This segment includes well removal, reclamation, plugging and abandonment, as well as commercial diving and other related services. Helix Alliance also operates a fleet of specialized vessels such as lifting vessels, offshore supply vessels and plug and abandonment systems. These activities accounted for 16% of the company's total revenue in the last 12 months.

Production Facilities — This segment includes the operation of the Helix Producer I floating production unit and the Helix Fast Response System, designed to contain spills in the Gulf of Mexico. This segment generates only 6% of the company's revenue.

Geographically, Helix Energy's sales are 50% generated in the US Gulf of Mexico, but the company has operations around the world, including in the North Sea (21% of sales), Brazil (14%) and Asia Pacific (13%).

Helix Energy covers several phases of offshore well development, and therefore demand for its services is highly dependent on market energy prices and the willingness of oil and gas project operators to make capital investments. An advantage of Helix Energy's business is that some of its activities also depend on the operating costs of its customers — for example, production maximization services that help the company’s clients to avoid unnecessary capital expenditures. Moreover, Helix Energy benefits from the global trend of low-carbon energy transformation by providing services to the renewable energy industry, mainly related to submarine cable installation and seabed clearing.

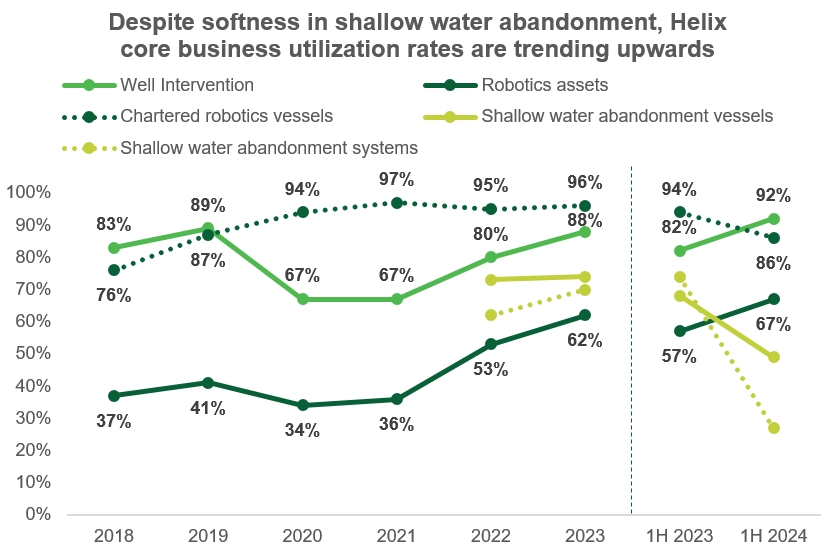

We are currently seeing positive asset utilization in two of the company's key segments, which is likely to contribute to its development in the medium term.

The well operations segment is experiencing a revival, particularly evident in the operating margin dynamics. Vessels are in high demand, with utilization rates reaching 92% in H1 2024, compared to 82% in H1 2023. In particular, the two vessels in the Gulf of Mexico showed a utilization rate of 82% in Q2 2024 due to a short break between customers, while the five vessels in the North Sea, Australia and Brazil were utilized at 100%. Management is forecasting an even more successful 2025.

The robotics segment is also expected to improve results next year on the back of strong utilization of support vessels in construction and supply for renewable energy projects. Helix Energy owns six vessels in this segment and all of them were employed during the quarter. The utilization rate was lower in Q1 2024 as one vessel was taken out of service to make improvements that will provide fuel savings. However, the utilization rate reached 76% in Q2 2024 compared to 58% in the same quarter a year earlier. Helix Energy management also noted fierce competition for vessels between oil & gas and renewable energy projects amid limited robotics supply.

As for the shallow water decommissioning business, this business is seasonal and highly dependent on weather conditions. In 2024, it suffered from weather-related delays in operations, and in Q2 2024, the company noted a decline in demand in the Gulf of Mexico offshore market, which had a direct impact on the segment's performance.

Reason 3: Contract rate revisions seen as key growth driver in coming years

Despite temporary weakness in the decommissioning segment, Helix Energy's order book is growing and stands at $873 million as of Q2 2024. Approximately half of these orders are contracted for years beyond 2024. The backlog has grown from $850 million at the end of 2023. Most recently, Helix Energy won Petrobras' tender and signed a three-year contract with the Brazilian oil and gas company to lease two well intervention vessels along with services. The contract value is estimated at $786 mln.

Helix Energy's management reported that previous vessel leases, which the company entered into during the market downturn at lower freight rates, are beginning to expire. Ongoing negotiations with customers for new contracts are expected to result in higher rates and significantly higher EBITDA, with initial results expected as early as 2025. Management announced the following important milestones for the company in the near term:

For one of the vessels in Brazil, which is used to improve well performance, freight rates are expected to increase by 40% towards 2025, with the vessel to be utilized until 2028. The EBITDA contribution from a single vessel is estimated to be in the range of $50,000 to $70,000 per day. By extending these contracts, Helix Energy is securing a more favorable market position for the coming years.

Some of the older contracts have built-in rate increase mechanisms. Freight rates for another vessel in Brazil will increase by approximately 20% when the contract is renewed in 2025.

In the robotics segment, trenching and demand from wind farms provide a flow of contracts until 2027 and a number of negotiations are already underway for 2028. Helix Energy also plans to use the last available trenching vessel in 2025, which was not in demand this year.

While the outlook for shallow water decommissioning remains unclear in the near term, the segment is already underperforming and this has already been factored into the stock's market value. An unexpected increase in customer spending could have a positive impact on Helix Energy's results in 2025.

An important consideration for investors is the fact that Helix Energy does not plan to reinvest cash flow in expanding capital expenditure in the near term and will only use cash to support capital expenditure.This will preserve the company’s potential to increase shareholder value.

Financial results

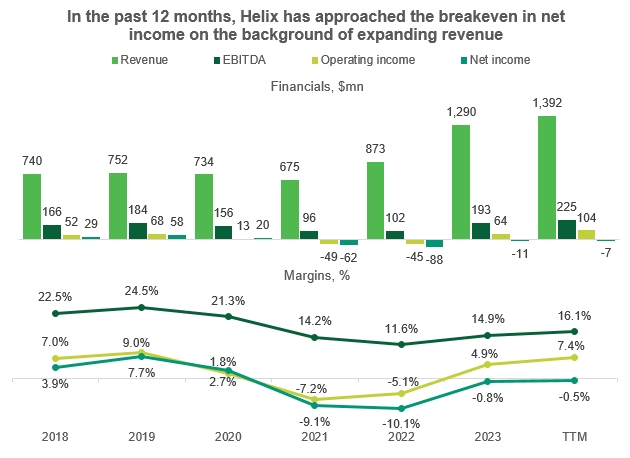

Helix Energy's financial results for the trailing 12 months (TTM) through Q2 2024 are as follows:

- Revenue increased 7.9% to $1.39 billion.

- EBITDA grew 16.7% to $225 million, with EBITDA margin reaching 16.1%, 1.2 p.p. above the 2023 result.

- Operating profit soared 63% to $104 million, or 7.4% of revenue. Margin expansion amounted to 2.5 p.p.

- Net income came more close to zero compared to 2023, but was still negative at -$7 million, or -0.5% of revenue.

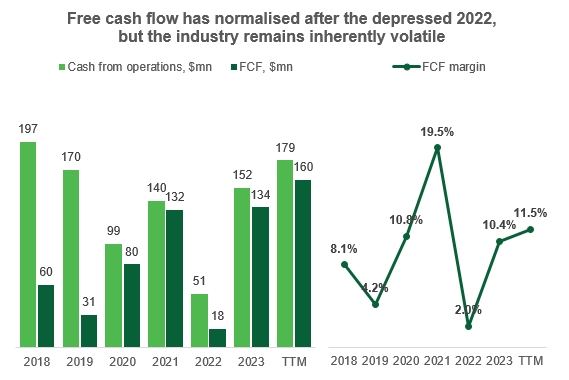

Cash flows from operating activities increased by 17.2% year-on-year (YoY) to $179 million. The main drivers of growth were an increase in depreciation and amortization in the cost structure, a loss of approximately $20 million related to convertible bonds, which are non-cash in nature, and a reduction in other current assets. With stable capital expenditures, free cash flow (FCF) increased 19.8% to $160 million. FCF margin expanded 1.1 p.p. to 11.5% of revenue. The FCF margin is noticeably volatile for the company, which is part of its business specifics.

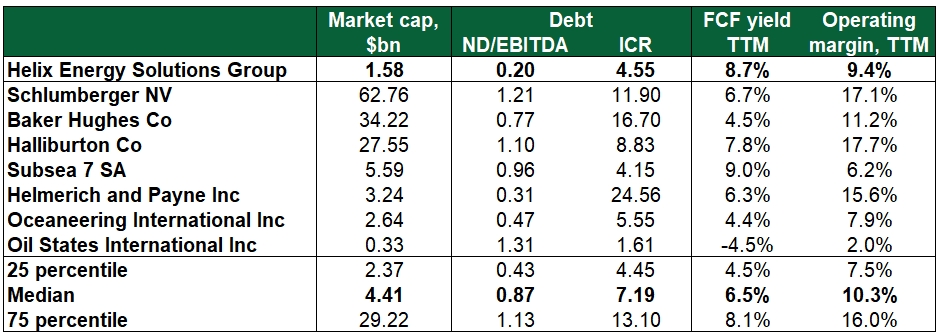

Helix Energy does not rely heavily on debt, in part due to the volatile nature of its business. As of Q2 2024, the company has $318.6 million in total debt, of which only $9 million is short-term debt, with $275 million in cash reserves. Overall, net debt is only 0.19x TTM EBITDA, with an interest coverage ratio of 4.55x. Thus, the debt load is not a problem for Helix Energy's financial position.

Stock valuation

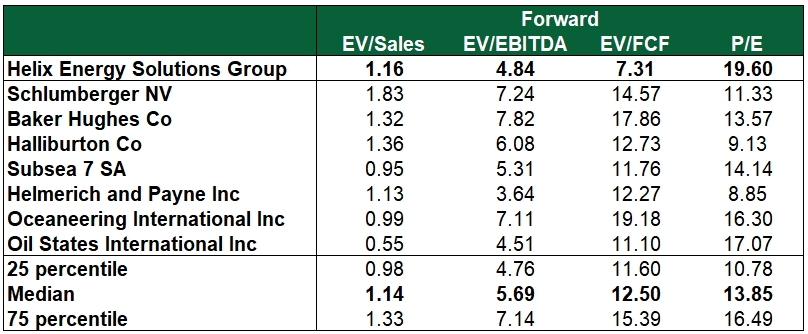

Helix Energy is valued closer to the lower end of the peer group due to both the presence of larger integrated oilfield service companies in the group and Helix Energy's current negative net income. The lower multiples also reflect the smaller size and scope of the company's operations.

TTM EBITDA and FCF multiples reflect a discount of 24% and 30%, respectively, relative to the group, while forward EBITDA and FCF multiples reflect a discount of 15% and 42%, respectively. As the company is only expected to reach the break-even point, the forward P/E is already higher relative to other companies.

Helix Energy's fundamentals are average, but its debt burden is lower. We believe the company has the potential to narrow the valuation gap with peers as further recovery of the offshore industry allows it to realize operating leverage and improve margins.

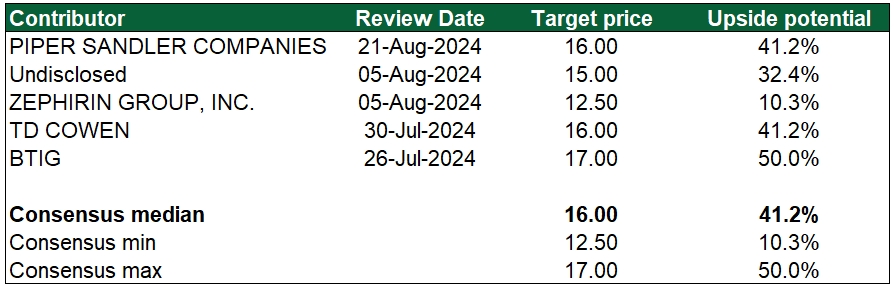

Wall Street analysts are very optimistic about Helix Energy’s stock, forecasting target prices of $12.5 to $17.0 per share. At the same time, the median estimate of $16.0 implies a 42.2% upside potential over 12 months.

Key risks

A prolonged shock to the oil market could affect long-term investment in the offshore industry and reduce the growth prospects of companies related to the industry. The emergence of new negative surprises in the well abandonment segment could undermine the overall positive momentum in other parts of the business.

Helix Energy may face stiff competition from larger oilfield service companies and may not be able to deliver the desired workloads or prices. The company's current order book is 73% concentrated in long-term contracts with six customers. The early termination or renegotiation of any of these contracts could have a significant impact on the future order book.