- Ticker: HPE.US

- Current price: $12

- Target price: $17

- Growth potential: 41,66%

- Dividend yield: 3,9%

- Time horizon: 6-9 months

- Risk: High

- Position size: 2%

Hewlett Packard Enterprise Company offers its customers data collection, processing, analysis and storage solutions. Its products include servers for various applications, storage devices, wired and wireless networking solutions, communications and media solutions, as well as cloud solutions, professional support services and software. In addition, Hewlett Packard offers financing and leasing services. The company operat in the Americas, Europe, the Middle East, Asia Pacific, Japan and Africa.

What's the idea?

- Diversified business with a focus on the most profitable segments.

- The new artificial intelligence solution could be in demand from large banks interested in reducing fraudulent transactions.

- Improved financial performance and a strong balance sheet will support the company's growth.

Why may the stock rise?

Reason 1. Order growth, diversified business with good potential and innovation

Hewlett Packard Enterprise has a well diversified business, both in terms of geographical revenue distribution (40% Americas, 36% EMEA, 24% Asia Pacific and Japan) and in terms of segment revenue distribution.

The highest allocation is to the most efficient segments:

Compute — 43% of revenue with an operating margin of 13.3% and a growing backlog (orders accepted but not yet fulfilled and not reflected in revenue). The cloud computing market will grow at a compound annual growth rate of 19.9% over the horizon of 2022-2029, according to Fortune Business Insights.

Storage — 16% of revenue with an operating margin of 14.7% and a growing backlog. MarketsandMarkets forecasts the cloud storage market to grow at a compound annual growth rate of 18.5% (CAGR) through 2027. In addition, Hewlett Packard Enterprise has recently begun offering blockchain storage as a service to customers, which could further boost its customer base. With block storage, data is broken down into blocks of the same size, which improves speed and performance when accessing such data.

Intelligent Edge — data generation, analysis and interpretation generate 13% of revenue at an operating margin of 16.5% and the seventh consecutive quarter with a year-on-year increase in orders of more than 15%. Analyst firm Technavio believes the data analytics market expects to grow at a 13.6% (CAGR) through 2026.

High performance computing & artificial intelligence — 12% of revenue with an operating margin of 3.4%. At the same time, the segment's margins showed a year-on-year increase of 900 basis points on the back of higher volumes of services provided. We expect this segment's margins to grow further due to a new artificial intelligence solution that will allow training predictive models on more data without privacy issues. Such a solution will be of interest to banks for anti-fraud and other purposes. Although the new solution was announced at the end of April, we anticipate that the process of negotiating with large banks to use the new product on customer data will take quite some time due to the need to ensure a high level of data privacy. This could mean that the new technology has not yet realised its potential to improve the segment's financial results.

Among other things, Hewlett Packard Enterprise has enriched its Aruba service platform with additional artificial intelligence capabilities that significantly reduce the need for manual network configuration and can attract new customers for whom the solution was previously too time-consuming.

In another new source of revenue, the company announced on 29 September that it had reached an agreement with a UAE-based telco to deploy end-to-end orchestration software to accelerate the digital transformation of its operations support system to the next generation to expand its service offerings and monetise its 5G investment. Successful implementation will help the company increase market share in the rapidly growing 5G area and further accelerate financial performance growth.

Reason 2. Buyback programme and dividends

Having analyzed Hewlett Packard Enterprise's 2021 Form 10-K and stock buyback program implementation data we can conclude that the company has an additional $1.5 billion (~9.6% of total market capitaliation) remaining to repurchase shares from the originally reported amount. Hewlett Packard Enterprise maintains stable free cash flow and significant balance sheet strength, so we expect the buyback to continue amid undervaluation. However, the company's programme does not include a specific timeline for implementation.

Hewlett Packard Enterprise pays its shareholders a dividend with a yield of around 3.9% per annum.

Financial indicators

The company's results for the last 12 months:

TTM revenue: up from $27.64 billion to $27.98 billion

TTM operating profit: up from $2.03 billion to $2.04 billion

in terms of operating margins — unchanged at 7.3%

TTM net profit: up from $1.03 billion to $3.73 billion thanks to a positive performance in one-off revenue of $1.73 billion compared to $1.10 billion in the same period a year earlier:

in terms of net margins an increase from 3.7% to 13.3%

Operating cash flow: increase from $3.66 billion to $4.51 billion

Free cash flow: up from $1.33 billion to $1.62 billion

Hewlett Packard increased revenue from $6.9 billion to $7 billion and EPS from $0.47 to $0.48 in its latest reported period, ended 31 July 2022.

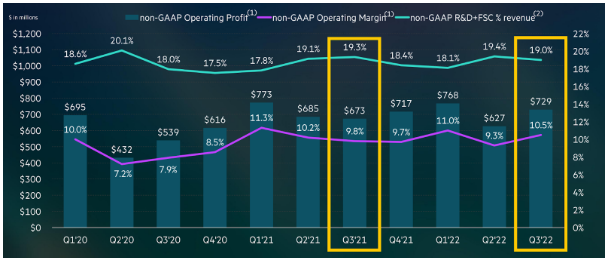

In terms of operating profit in the chart below, the company showed an increase from $673 million to $729 billion, boosting its operating margin from 9.8% to 10.5%.

On the cash flow side, as seen in the infographic below, the company's Q3 results were not only able to recover from a temporary slump early in the year, but also surpassed last year's results: operating cash flow rose from $1.1 billion to $1.3 billion and free cash flow increased from $0.5 billion to $0.6 billion.

It is worth noting that the company is showing robust financial results despite the current difficulties associated with the worsening geopolitical situation and the emergence of a recession in the global economy. At the same time, Hewlett Packard Enterprise managed to withdraw from the Russian market without significant losses. Thus, the company feels quite confident even in the current difficult times and maintains its business in a stable condition.

- Cash and cash equivalents: $3.76 billion

- Net debt: $10.1 billion

- Net debt/EBITDA: up/down year-on-year from 2.36x to 2.23x

Hewlett Packard Enterprise's significant cash and cash equivalent reserves, coupled with improved cash flow and an acceptable level of leverage, point to good financial strength. Separately, we highlight the fact that the level of real debt risk is actually lower than it first appears: if we evaluate only the company's operating segments, not including the financing segment, we see that such a company's net debt would be negative at -0.7 billion (left-hand chart below). At the same time, the assets of the finance segment are $12.6 billion and exceed the liabilities of $11.7 billion (right-hand chart).

Evaluation

If we look at the multiples, we notice that the company is undervalued relative to its competitors.

For FY2022, the company expects revenue to increase by 3%-4% year-on-year, demonstrating management's ability to grow the company's financial performance even in the face of macroeconomic pressures.

Ratings of other investment houses

The minimum price target set by Citigroup is $13.5 per stock. Raymond James and Barclays have set a target price of $19. By consensus, the fair value of the stock is $16.5, suggesting a 36.1% upside potential.

Key risks

- An unstable macroeconomic situation can force customers to cut costs.

- A prolonged continuation of the recession could potentially slow the company's growth rate.

How to take advantage of the idea?

- Buy shares at a price of $12.

- Allocate no more than 2% of your portfolio for purchase. To compile a balanced portfolio, you can use the recommendations of our analysts.

- Sell when the price reaches $17.