What's the idea?

HealthEquity Inc. is the largest provider of HSAs in the US, managing approximately 9.4 million HSAs with $29.5 billion in assets, as of July 2024, alongside 6.9 million other CDB accounts. The US HSA market has grown substantially, with total assets increasing from $65.9 billion in 2019 to $123.3 billion in 2023, reflecting a compound annual growth rate (CAGR) of 17%. Projections suggest HSA assets could reach $168.3 billion by 2026, indicating further market expansion.

To fuel future growth, HealthEquity has implemented several strategic initiatives, including strong sales efforts, a new mobile app, and AI-powered claims processing. The company has also enhanced its partnerships within the health benefits ecosystem and recently launched HPAs in collaboration with Paytient, offering employees an interest-free way to manage healthcare costs.

HealthEquity’s Q2 FY2025 results outperformed expectations, with revenue increasing by 23% YoY (YoY) to $299.9 million, surpassing analysts' consensus estimate of $285.1 million. Non-GAAP net income reached $76.3 million, or $0.86 per share, beating the estimated $0.70 per share.

As a result, the company raised its FY2025 guidance, now projecting non-GAAP EPS between $2.98 and $3.14, with revenue expected to range from $1.17 billion to $1.19 billion. While potential risks include a future decline in interest rates, which could impact custodial revenue, HealthEquity’s strong HSA growth and increasing invested assets are expected to drive continued performance.

About Company

HealthEquity Inc. (HQY) offers technology-enabled services that help consumers make informed decisions about healthcare savings and spending. The company manages tax-advantaged Health Savings Accounts (HSAs) and other consumer-directed benefits (CDBs) provided by employers. As of June 2023, HealthEquity was the largest HSA provider in the US, with a 20% market share, leading both in the number of accounts and total HSA assets under management. HealthEquity was founded in 2002 and is headquartered in Draper, USA.

Why do we like HealthEquity Inc?

Reason 1. Rising demand for healthcare saving solutions drives growth in the US HSA market

HealthEquity Inc. (HQY) provides technology-enabled services that empower consumers to make health care savings and spending decisions. It manages consumers' tax-advantaged health savings accounts (HSAs) and other consumer-directed benefits (CDBs) offered by employers. In addition, the company provides consumers with payment processing services, personalized benefit information, the ability to earn wellness incentives and investment advice to grow their tax-advantaged health savings.

HealthEquity’s products and services include:

Health Savings Accounts. An HSA is a financial account that allows consumers to spend and save for health care expenses on a tax-advantaged basis over the long term. HSAs are managed by a custodian, which can be a bank, an insurance company or a non-bank custodian specifically approved by the Internal Revenue Service (IRS). HealthEquity is an IRS-approved non-bank custodian of its members' HSAs.

Investment Platform and Advisory Services. HealthEquity provides an investment platform and access to an online investment advisory service to members whose account balances exceed a specified threshold. The advisory service is provided through a web-based tool, Advisor, managed by HealthEquity Advisors LLC, its SEC-registered subsidiary. Members using these services pay asset-based fees, subject to a monthly fee cap.

Other Consumer Directed Benefits. Other CDBs include health flexible spending accounts (FSAs), dependent care flexible spending accounts, health reimbursement arrangements (HRAs), federal COBRA and state continuation benefits, and commuter programs.

The HSA is HealthEquity's core offering. As of July 31, 2024, it administered 9.4 million HSAs, with total balances amounting to $29.5 billion. In addition to HSAs, the company managed 6.9 million complementary CDBs, bringing the total number of accounts, including both HSAs and CDBs, to 16.3 million.

HealthEquity holds a leading position in the HSA industry, steadily growing its market share over the years. From December 2010 to June 2023, the company increased its share of the HSA market from 4% to 20%, as measured by HSA Assets. Moreover, according to the Devenir HSA Research Report, HealthEquity was the largest HSA provider as of June 2023, both in terms of the number of accounts and the total HSA Assets under management.

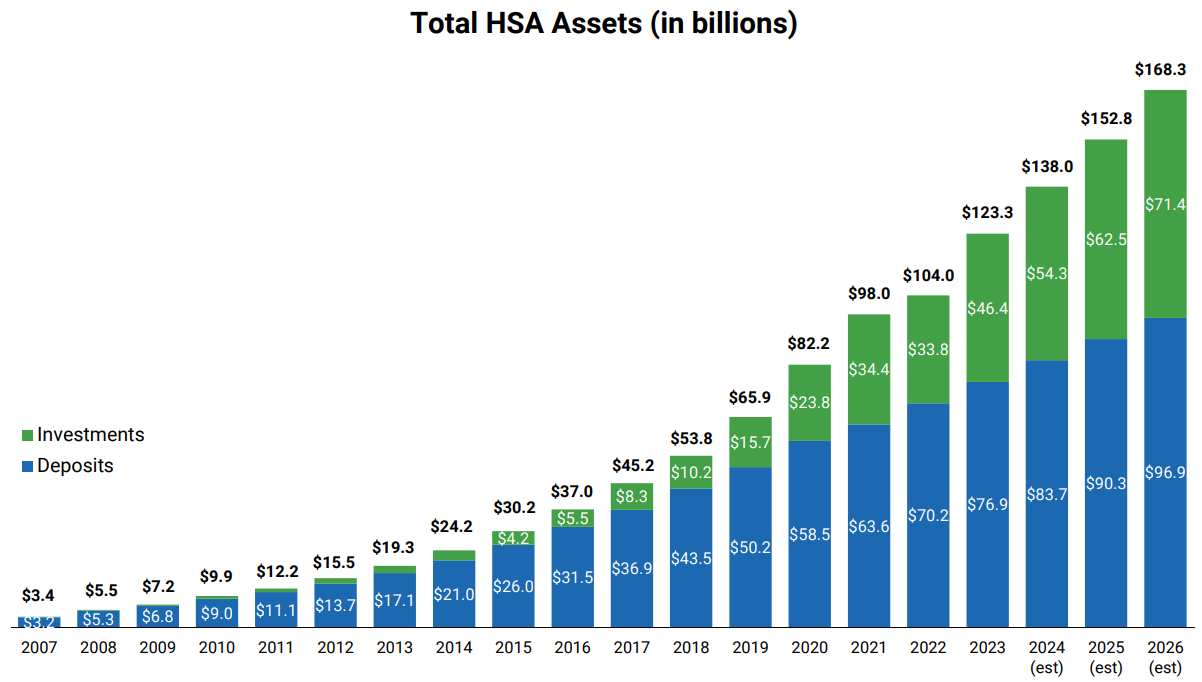

The US HSA market has experienced significant growth over the past several years. From 2019 to 2023, total HSA assets surged from $65.9 billion to $123.3 billion, reflecting a CAGR of 17.0%. In 2023, HSA assets saw record growth, driven by favorable stock market conditions, although the growth in the number of HSA accounts slowed during the year. By the end of 2023, there were $123.3 billion in HSA assets held across more than 37 million accounts, marking a year-over-year (YoY) increase of 18.6% in assets and 5.3% in the number of accounts. Devenir forecasts HSA assets to reach $138.0 billion by 2024, an 11.9% increase, and grow further to $168.3 billion by 2026, with a CAGR of 10.9% over the 2023–2026 period.

Total HSA assets in the US

Trends in the distribution of HSA assets between deposits and investments have been shifting in recent years. Historically, deposits were the primary destination for HSA assets, accounting for 76.2% of total HSA assets in 2019. However, this trend is changing as more individuals are allocating their HSA assets into investments. In 2023, HSA investment assets grew by 37%, reaching $46 billion by the end of the year, resulting in their share amounting to 37.6%, while deposits made up the remaining 62.4%. By 2026, investments are expected to continue expanding and are projected to account for 42.4% of total HSA assets. However, with a greater share of HSA assets now being held in investments, the impact of market movements is making it more challenging to project future growth with certainty.

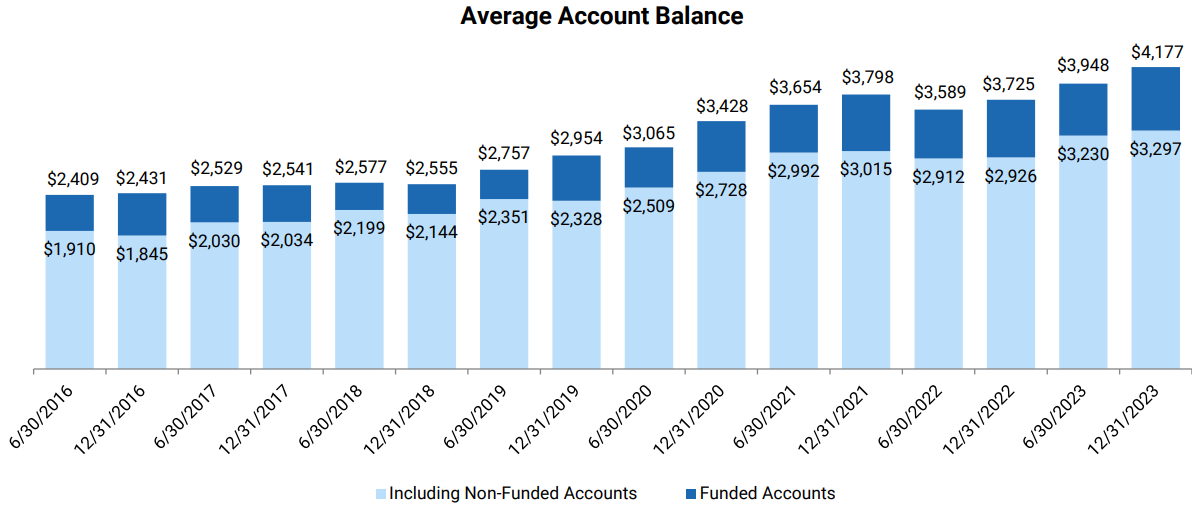

Additionally, the average HSA account balance has shown strong growth. After experiencing some contraction in the first half of 2022, the average balance rebounded significantly. By December 31, 2023, the average HSA balance reached a record high of $4,177, up 10% from $3,798 as of December 31, 2021. This growth underscores the increasing value and utility of HSAs for consumers.

Average HSA balance

Despite strong overall growth in the HSA market, there are some negative trends to consider. First, the pace of account growth continued to slow during 2023, with a 5.3% YoY growth. Devenir currently projects that the HSA market will approach 44 million accounts by the end of 2026, which implies a CAGR of 5.6% over 2023–2026. Secondly, withdrawal activity is increasing. In 2023, HSA account holders contributed $50 billion to their accounts, a 7% increase from the prior year. However, withdrawals grew at a faster rate, with $39 billion being withdrawn, up 13% from the previous year.

Nevertheless, HSA providers are expected to grow their businesses by 23% in 2024. Historically, these providers have been fairly accurate in their growth forecasts, demonstrating a strong understanding of their business outlook. Several factors support this positive projection:

Recent research by Fidelity found that 17% of Americans report that paying medical bills for a health condition is preventing them from reaching their retirement goals. Additionally, more than a third (36%) of respondents said that being able to afford health care is among their top retirement concerns.

The good news is that younger generations are increasingly leveraging HSAs to invest for future health care costs. According to Fidelity, younger HSA holders, particularly those aged 18 – 35, were more likely to invest their HSA funds compared to older account holders.

Americans of all ages are taking steps to address the rising costs of care, with 71% indicating plans to save more for retirement due to concerns about the high cost of health care.

These trends highlight the growing importance of HSAs as a tool for financial and health care planning, supporting future growth of HSA providers’ businesses.

Reason 2. Diversified revenue streams and promising growth drivers

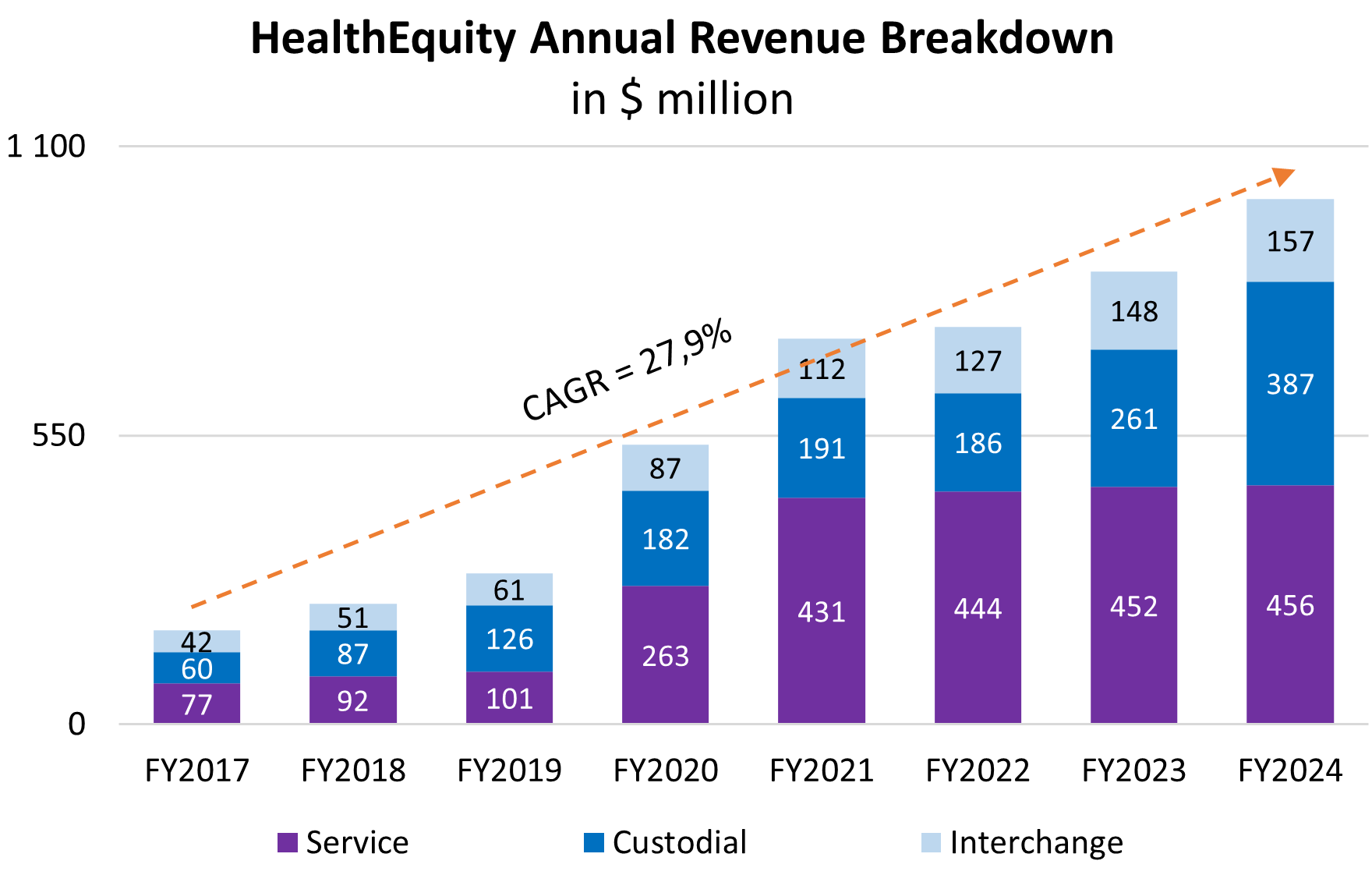

HealthEquity generates revenue from three primary sources:

Service revenue: This comes from fees paid by clients and members for administrative services related to HSAs and other consumer-directed benefits. It also includes fees for recordkeeping and investment advisory services. In FY2024, service revenue accounted for 45.6% of the company’s total revenue.

Custodial revenue: HealthEquity earns interest on HSA cash held by its federally insured bank and credit union partners (Depository Partners), insurance company partners, and client-held funds deposited with Depository Partners. Custodial revenue contributed 38.7% to the company’s total revenue in FY2024.

Interchange revenue: This source is derived from fees paid by merchants when HealthEquity members make payments using physical or virtual payment systems. Interchange revenue represented 15.7% of total revenue in FY2024.

Therefore, the company’s main revenue drivers include the growth in the number of accounts on its platform (both HSAs and CDBs), increases in account balances, the yield earned on HSA cash and client-held funds, and the level of health-related spending per account.

HealthEquity annual revenue breakdown

The company possesses several competitive strengths that helps it to successfully compete with peers and maintain leading market positions:

HealthEquity offers an integrated, bundled solution for HSAs and complementary CDBs, positioning itself as a one-stop provider for these services. The company operates proprietary cloud-based technology platforms, which are currently undergoing modernization. These platforms are accessible via desktop or mobile devices, allowing HSA members to manage healthcare savings and spending, pay medical bills, receive personalized benefit information, earn wellness incentives, and grow their savings. Additionally, all HSA users can access healthcare consumer specialists 24/7. The company also provides a commuter platform that offers real-time commute data to help clients design and implement flexible return-to-office and hybrid workplace strategies.

The cloud-based technology platforms enable a scalable operating model, reducing service costs for any given customer over time after initial on-boarding and a period of education. The company benefits from a broad and diverse channel strategy, using a business-to-business-to-consumer (B2B2C) approach, while also marketing directly to potential members. HealthEquity maintains high HSA member retention rates, as individually owned trust accounts like HSAs have naturally high switching costs. This is further supported by the platform’s integration with the broader healthcare system, providing additional value to users.

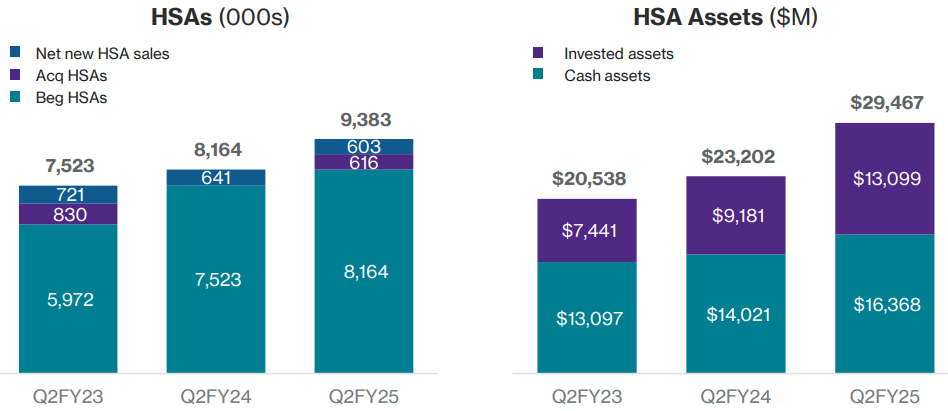

Developing and investing in technology capabilities and product offerings has been instrumental in driving HealthEquity's strong operating metrics. In Q2 FY2025, the company saw a net increase of 1.2 million HSA accounts, reflecting 23% YoY growth. HSA assets also surged by $6.3 billion, a 27% increase from the previous year, with cash assets growing by 17% and investments up by 43%.

Furthermore, the completion of the final tranche of Conduent’s BenefitWallet HSA portfolio acquired in May 2024 contributed to a 15% growth in HSA members, adding approximately 216,000 HSAs and $1.0 billion of HSA assets in Q2 FY2025. Notably, the number of HSA members that invest grew even faster, rising by 24% YoY, which helped drive a 43% YoY increase in invested assets, now totaling over $13 billion.

HealthEquity’s key operating metrics

The management remains optimistic about the company’s future growth, citing several key drivers. The first driver is effective sales strategies implemented by the sales and relationship management teams, which have boosted organic HSA sales. The management is particularly positive about this year's selling season. Beyond organic growth, the timely transfer of HSAs and assets from BenefitWallet has created opportunities for cross-selling CDBs into FY2026, while locking in strong custodial yields on these assets for years to come.

The second driver is the launch of a new mobile app and the continued rollout of claims AI. Additionally, in August, HealthEquity completed its migration to a new card processor, enabling the use of stack cards on major digital wallets. The next phase, expected next year, includes instant card issuance.

A third driver is the company’s digital transformation of sales and the strengthening of partnerships within the broader health benefits ecosystem. The management is working toward scaling partner-facing APIs, with a new third-party developer portal set to go live later this year.

The fourth driver is the formal launch of Health Payment Accounts (HPAs). In September, HealthEquity announced a collaboration with Paytient, a healthcare technology firm, to offer HPAs. These accounts provide a no-interest, no-fee option for employees to manage healthcare costs with flexible payment terms, complementing existing benefits like HSAs, FSAs, and HRAs. HPAs allow employees to select the best medical plans for their needs without the fear of depleting savings or going into debt, as there are no credit checks or impacts on credit scores.

Reason 3. Strong Q2 FY2025 results, with raised full-year guidance

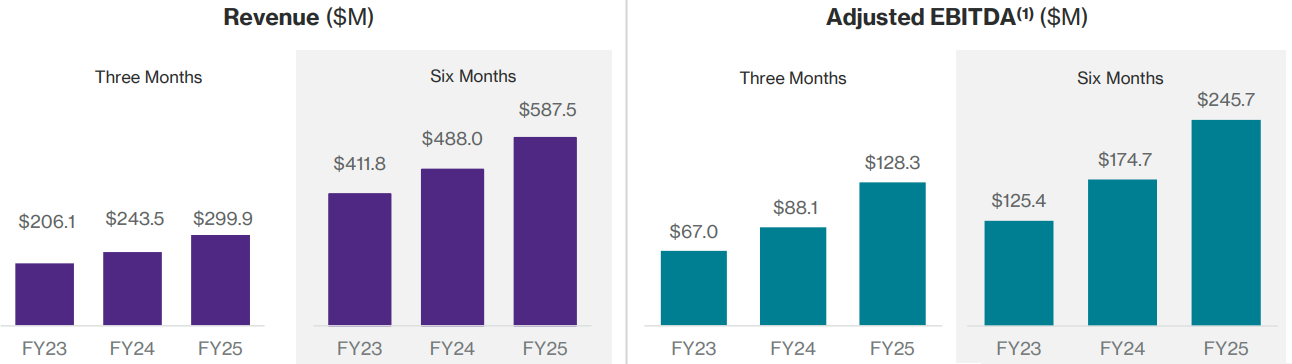

HealthEquity delivered strong performance in Q2 FY2025, with revenue reaching $299.9 million, a 23% increase from $243.5 million in Q2 FY2024, surpassing analysts' expectations of $285.1 million, as surveyed by Capital IQ. Net income for the quarter was $35.8 million, or $0.40 per share on a GAAP basis. On a non-GAAP basis, net income reached $76.3 million, or $0.86 per share, well above analysts' expectations of $0.70 and up from $0.53 per share a year ago.

Breaking down the quarterly revenue, its service revenue grew 4% YoY to $116.7 million, driven by growth in total accounts, HSA investor accounts, and invested assets, despite a mixed shift toward HSAs that lowered average unit service revenue. Custodial revenue saw an impressive 50% growth, reaching $138.7 million, supported by a 3.1% annualized interest rate yield on HSA cash due to BenefitWallet placements and a shift toward enhanced rates. Besides, interchange revenue grew by 14% to $44.5 million, outpacing account growth as members increasingly used payment cards over cash reimbursements.

As for profitability, HealthEquity’s gross profit margin improved to 68% in the second quarter, up from 62% the prior year. Adjusted EBITDA surged by 46% YoY to $128.3 million, with an adjusted EBITDA margin of 43%, representing a 650 basis point improvement compared to the same quarter last year.

HealthEquity’s revenue and adjusted EBITDA

Such strong results have prompted the management to raise FY2025 guidance and they are now projecting non-GAAP EPS between $2.98 and $3.14 on revenue of $1.17 billion to $1.19 billion, up from its previous forecast of $2.93 to $3.10 on revenue of $1.16 billion to $1.18 billion. Analysts are expecting earnings of $3.0 per share on $1.17 billion in revenue.

HealthEquity’s FY2025 guidance

One of the main risks to HealthEquity’s future financial performance stems from the potential start of an easing interest rate cycle by the Fed. HealthEquity earns a significant portion of its custodial revenue from interest on HSA cash assets deposited with its Depository Partners, which surged during FY2022 to FY2024 due to increasing interest rates. With interest rates likely to decrease in the coming quarters, custodial revenue growth is expected to slow. However, HealthEquity’s robust organic growth in HSA accounts and assets, coupled with an increasing volume of invested assets driven by favorable stock market conditions, is anticipated to help sustain overall revenue growth, offsetting the potential slowdown in custodial revenue.

Thus, HealthEquity's strengths, including its solid HSA account growth, increasing invested assets, and its ability to adapt to market conditions, position the company well for continued success. These factors, along with strategic innovations and partnerships, make the company resilient in a changing financial landscape.

Financial performance

HealthEquity’s trailing twelve months (TTM) financial results can be summarized as follows:

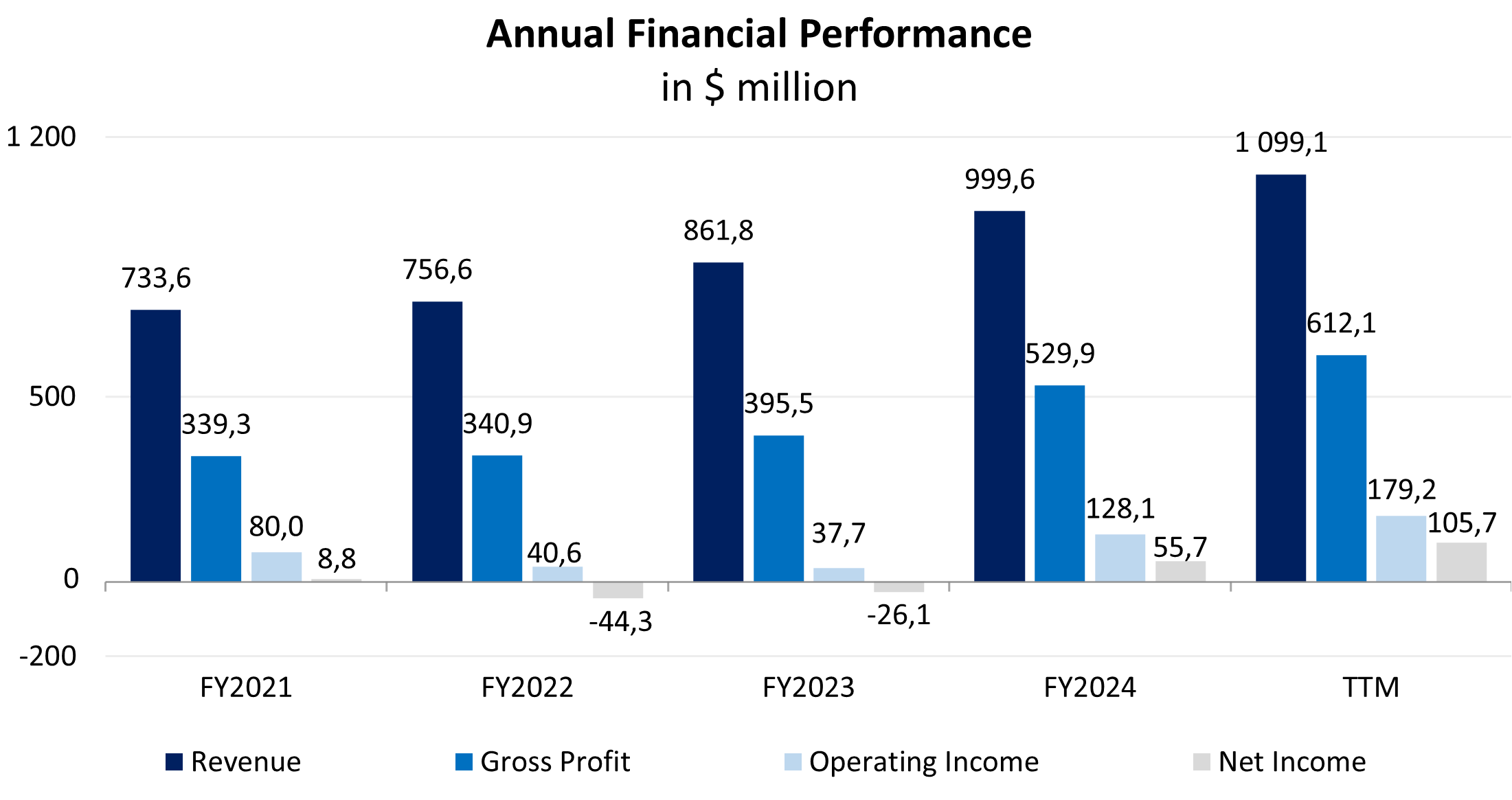

- Revenue increased to $1.09 billion, up by 10.0% compared to FY2024.

- Gross profit grew by 15.5%, from $529.9 million in FY2024 to $612.1 million TTM, with gross margin improving from 53.0% to 55.7%.

- Operating income surged by 39.9% and accounted for $179.2 million. Operating margin expanded from 12.8% to 16.3%.

- Net income soared by 89.7%, from $55.7 million in FY2024 to $105.7 million TTM. Net margin increased from 5.6% to 9.6%.

Dynamics of annual financial results

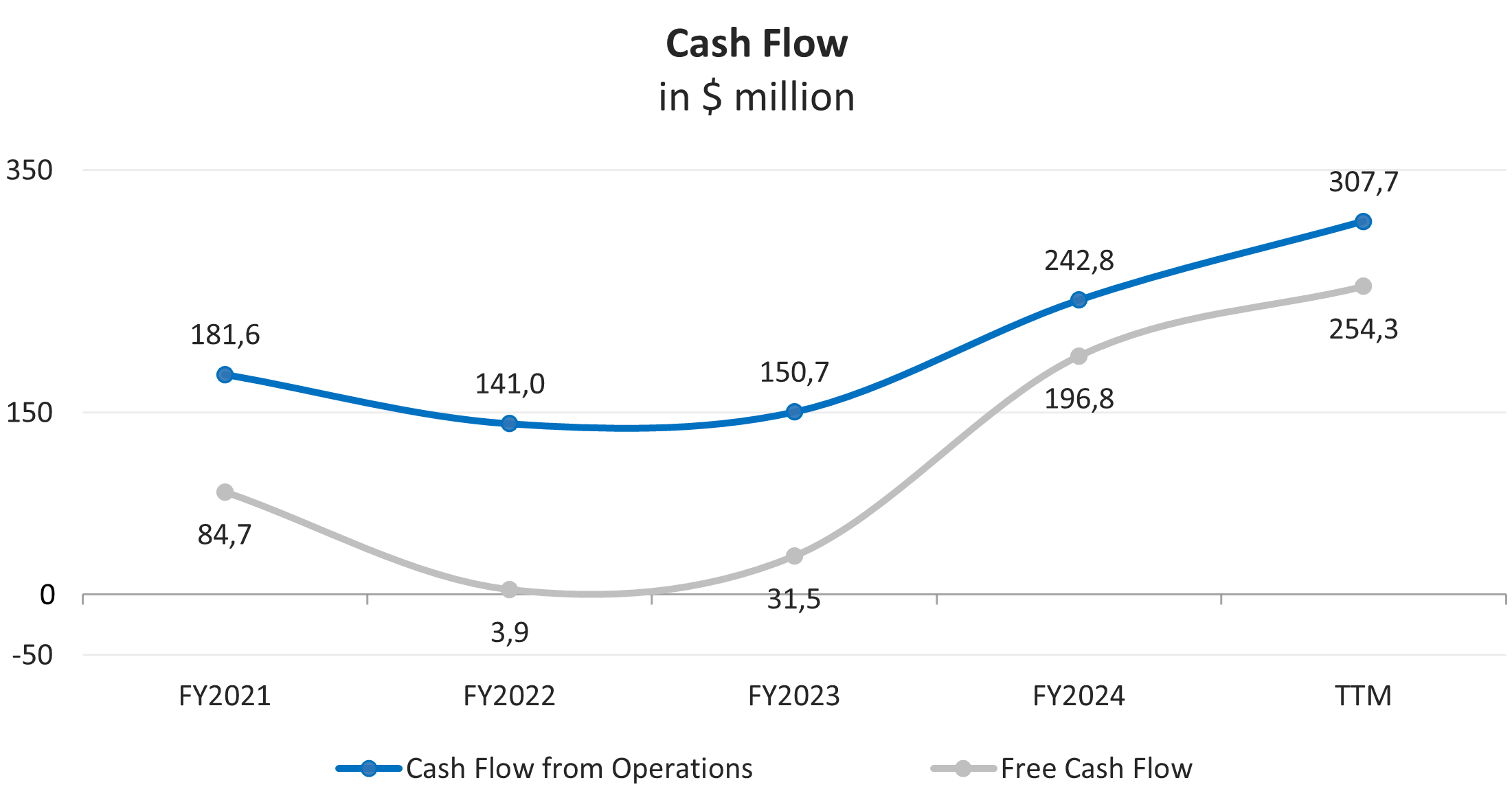

HealthEquity has significantly improved its cash flows over the past several years. Its TTM operating cash flow (FFO) accounted for $307.7 million, up by 26.7% compared to FY2024, driven largely by higher net income and improvements in non-cash items. TTM free cash flow (FCF) amounted to $254.3 million, up by 29.2% compared to FY2024, due to lower growth in capital expenditure.

Dynamics of annual financial results

The company's financial performance for Q2 FY2025 is presented below:

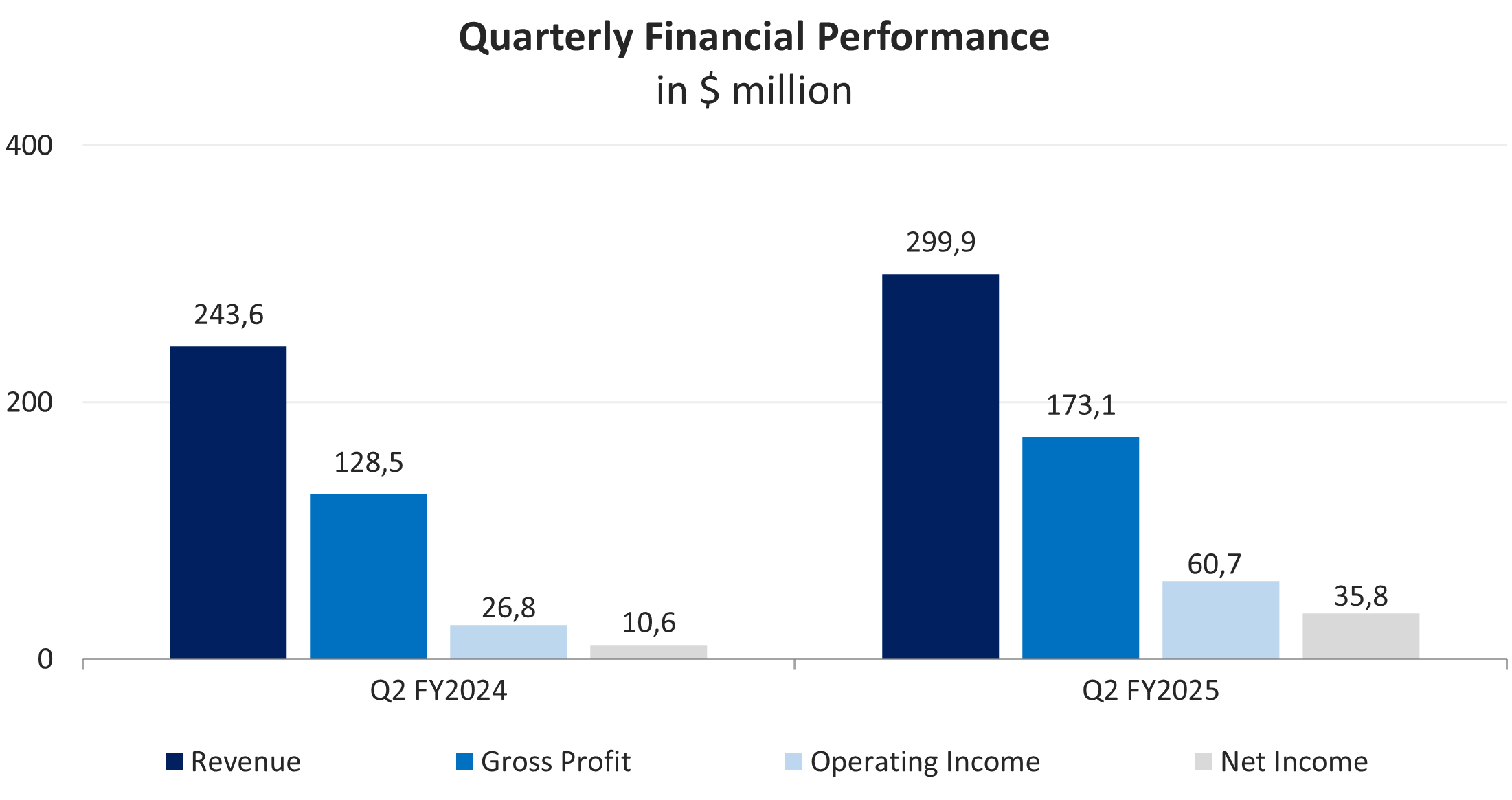

- Revenue increased by 23.1% YoY, from $243.6 million to $299.9 million.

- Gross profit grew by 34.7% YoY, from $128.5 million to $173.1 million.

- Operating income soared by 126.7% YoY, from $26.8 million to $60.7 million.

- Net income skyrocketed by 238.6% YoY, from $10.6 million to $35.8 million.

Dynamics of quarterly financial results

HealthEquity maintains a robust balance:

The leverage ratio, defined as the ratio of total debt to assets, stands at 33%, which is little higher than the industry average of 25%.

As of July 31, 2024, total debt accounted for $1.10 billion, up by 25.9% from $875.0 million on January 31, 2024. With reported cash and cash equivalents of $326.9 million, net debt accounts for $774.5 million.

The company earned $337.5 million of TTM EBITDA, and, consequently, Net Debt/EBITDA ratio equals 2.30x, which turns out to be better than the average of 3.73x over the past five years.

TTM interest expenses remained unchanged compared to FY2024 and accounted for $54.4 million. With TTM EBIT of $179.2 million, interest coverage ratio amounts to 3.29x, demonstrating the company’s ability to service its debt.

The company’s debt is represented by senior notes due 2029 (54%), term loan (26%) and revolving credit (20%). With strong cash flows that the company’s business model generates, HealthEquity is likely to settle its debts.

Stock valuation

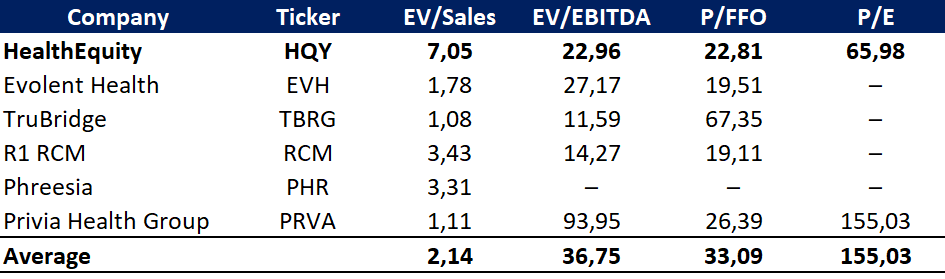

There are few public HSA providers that directly compete with HealthEquity. The table below presents companies whose businesses have some features similar to HealthEquity. Since HealthEquity is the most profitable, most its multiples are lower compared to those of peers but it trades with a premium to the average EV/Sales ratio: EV/Sales — 7.05x, EV/EBITDA — 22.96x, P/FFO — 22.81x, P/E — 65.98x. However, the company offers the best return per unit of risk taken.

Comparable valuation

The minimum price target set by an undisclosed investment bank is $95.0 per share, while another undisclosed investment bank values HealthEquity at $115.0 per share. According to the Wall Street consensus, the stock’s fair market value stands at $105.0, implying a 35.7% upside potential.

Price targets of investment banks

Key risks

HealthEquity’s revenue is primarily generated from tax-advantaged Health Savings Accounts (HSAs) and other consumer-directed benefits (CDBs). Efforts by government agencies or third-party payers to increase revenue or reduce healthcare costs could include changes to the tax advantages of HSAs and CDBs, potentially having an adverse impact on the company's business.

A significant portion of HealthEquity’s revenue comes from fees earned through partnerships with depository institutions and insurance companies. A decline in interest rates would reduce the company’s ability to generate income from HSA assets and client-held funds, while also making it more challenging to attract HSA contributions.The value of HealthEquity’s fees is tied to the performance of invested HSA assets. A decline in asset values, whether due to market conditions or other factors, would negatively affect fee income, ultimately hurting the company’s financial results.

Cyber-attacks or data security incidents pose a risk to HealthEquity, as the company relies heavily on its proprietary technology platforms. In addition, disruptions in service at its facilities, third-party data centers, or cloud service providers could impair customer access to its products and services.

The regulatory and political environment for healthcare is evolving and uncertain. HealthEquity cannot predict how future healthcare reforms or changes in government programs will affect its business and financial performance. Finally, HSAs and other CDBs exist due to provisions in the Internal Revenue Code and other laws. Any changes to this regulatory framework would require significant time and cost to ensure compliance with new laws, which could further impact the company’s operations.