About Company

The Goodyear Tire & Rubber Company (GT) manufactures and markets tyres for cars, trucks, buses, aircraft, motorbikes, earthmoving, mining and industrial machinery under the brands Goodyear, Cooper, Dunlop, Kelly, Debica, Sava, Fulda, Mastercraft, Roadmaster and others. The company sells its products through a network of independent dealers, regional distributors and retailers throughout the world. The Goodyear Tire & Rubber Company was founded in 1898 and is headquartered in Akron, Ohio.

What's the idea?

- Goodyear is the third largest producer in the huge and established tyre market. The acquisition of Cooper Tyres has significantly strengthened the company's position.

- The easing of covid restrictions in China should help the company's growth in the Asia-Pacific region.

- The potential of the electric vehicle market will provide Goodyear with considerable room for growth, as well as improving margins.

- Goodyear trades at a substantial discount to the industry average and a discount to book value.

Why do we like Goodyear Tire & Rubber?

Reason 1. Industry opportunities

The pandemic has taken a heavy toll on the tyre industry and the market is down 5.7%. Nevertheless, in the short term, Goodyear's future looks clear. The company's management notes stable demand conditions in both the retail and commercial segments. Automotive giants such as Ford and GM are also seeing steady demand and forecast sales growth despite the slowing global economy.

According to Allied Market Research, the global tyre market is expected to grow at a compound annual growth rate of 3.8% (CAGR) through 2030, reaching $218.9 billion at the end of the forecast period. Growth will be driven by increased vehicle production as well as the growing popularity of electric vehicles, pickup trucks, and other light commercial vehicles.

Although North America is the key region in terms of sales, the main growth will come from international markets — 4.2% (CAGR). China, Asia Pacific, and India and Brazil will be the fastest growing markets. A key driver of demand in these markets is rising prosperity driven by urbanisation and increased industrial activity. The takeover of Cooper Tyres allowed the company to double its presence in China, which now accounts for around 12% of total revenue. The easing of covid restrictions in China should support the company's growth in this region.

Reason 2. Acquisition of Cooper Tyres

In June 2021, Goodyear acquired Cooper Tyres for $2.8 billion, reinforcing its position as the world's third largest tyre company and making it the largest producer in its key market, the US. Today the combined company controls more than 25% of the spare tyre market.

Market position of the combined company

Although the main market for Cooper Tire was North America, which accounted for 82% of revenue, the company also had a strong global presence. This is important because the US tyre market is growing much more slowly than in developing countries.

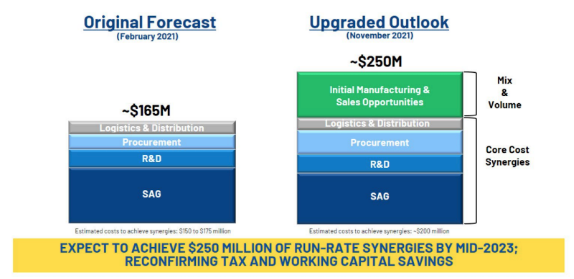

Based on pre-pandemic 2019 results, the combined operating profit of the two businesses would have been $1.003 billion ($820 million for Goodyear and $183 million for Cooper Tyres). The company's operating profit for the last 12 months is $1.069 billion. Initially, management expected to achieve $165 million in synergies through brand integration, but the forecast was raised to $250 million in the second quarter.

Expected synergies

A conservative estimate (excluding sales growth) puts potential operating profit at $1.320 billion. Thus, even with the 46.06 million stock dilution, this acquisition does not burn up shareholder value, but provides significant upside potential.

Reason 3. Prospects in the electric vehicle market

Goodyear is one of the main beneficiaries of the electric vehicle market. The company's innovative solutions have enabled it to win 60% of tenders for electric vehicle tyres in 2021. EV tyres differ from their conventional counterparts with regard to durability because electric vehicles are heavier than internal combustion engine vehicles. The need for quiet tyre performance has emerged, as electric vehicles are notable for their quiet ride. There has also been a demand for greater efficiency to increase the range of vehicles. In addition, the regenerative braking technology used in most electric vehicles requires additional functions from tyres that were not available before.

By 2035, 59% of all new cars sold are expected to be electric. Thus, the potential market for electric vehicles is enormous, providing Goodyear with significant room for expansion. In addition, growth in this market could improve the company's margin profile, as tyres for electric vehicles sell for more than 30% more than their internal combustion engine counterparts, according to Deutsche Bank.

Financial indicators

The company's financial results for the last 12 months can be summarised as follows

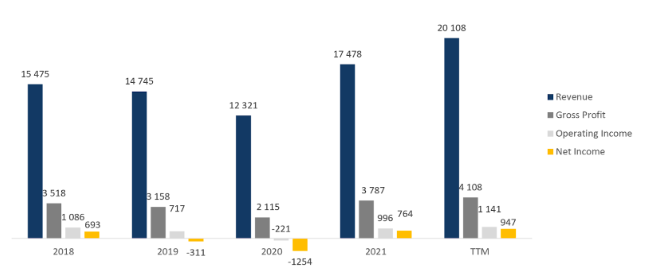

- TTM posted revenues of $20.11 billion, up 15% on 2021. Growth was driven by the takeover of Cooper Tyres as well as the market recovery from the pandemic.

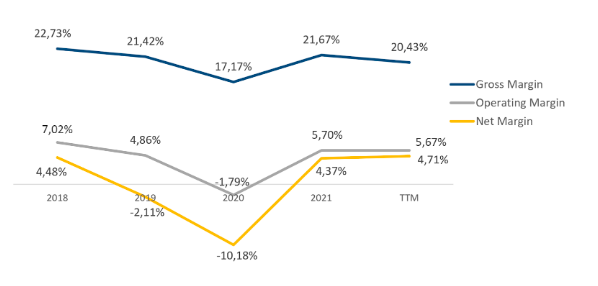

- At the end of the last reporting period, gross profit rose by 8.5%: from $3.79 billion to $4.12 billion. The gross margin declined from 21.67% to 20.43%, due to the impact of inflation.

- Operating profit rose by 14.6%: from $996 million to $1.14 billion. The operating margin was 5.67% compared to 5.70% for the year.

- Net profit rose from $764 million to $947 million. Net profit margin increased from 4.37% to 4.71% for the year.

Trends in the company's financial results

Company margin dynamics

The financial results for the first half of 2022 are as follows

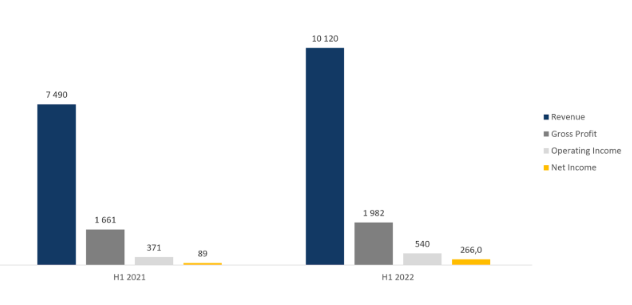

- Revenue rose 35.1 per cent year on year, from $7.49 billion to $10.12 billion.

- Gross profit increased by 19.3% year on year: from $1.66 billion to $1.98 billion. Gross margin decreased by 2.59 percentage points: from 22.18% to 19.58%.

- Operating profit was $540 million compared to $371 million a year earlier. The operating margin increased from 4.95% to 5.34%.

- Net profit rose from $89 million to $266 million. Net margin increased by 1.44 percentage points: from 1.19% to 2.63%.

Dynamics of the company's financial results

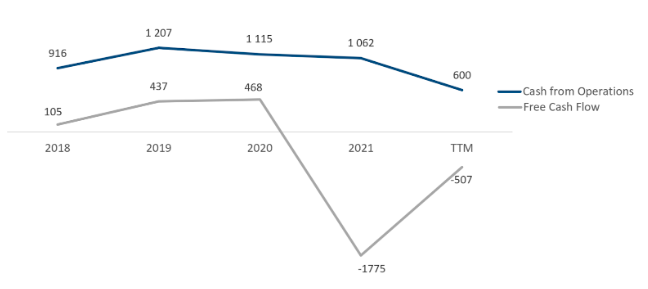

At the end of the latest TTM reporting period, operating cash flow was $600 million compared to $1.06 billion at the end of the year. The decrease was due to an increase in net working capital because of the inventory balance. Free cash flow to equity increased from -$1.78 billion to -$507 million. The negative free cash flow is due to a large capital expenditure programme, which is expected to significantly improve the efficiency of the operations in the future.

Company cash flow

Goodyear has a high but manageable debt load: total debt is $9.45 billion, cash equivalents and short-term investments account for $1.25 billion and net debt is $8.21 billion, which is 3.9x TTM EBITDA (Net debt/EBITDA is 3.9x). Achieving synergies from the integration of Cooper Tyres will reduce the ratio to 3.5x.

Evaluation

Although Goodyear is one of the largest producers in a huge and established market, the company trades at a significant discount to book value and at a discount to the industry average: EV/Sales is 0.53x, EV/EBITDA is 5.06x, P/E is 3.47x and P/B is 0.63x.

Comparable estimate

The minimum price target from investment banks set by BNP Paribas is $12 per share. Wolfe Research, on the other hand, values Goodyear at $21 per share. According to the consensus, the fair market value of the stock is $18.50, which implies a 61.3% upside potential.

Price targets of investment banks

Key risks

- The general bearish mood in the global economy remains a key risk for the company, especially given the higher debt load than competitors. This could cause a further downward movement in the stock price.

- The company has extremely low margins, which pose a risk to shareholder value in the current macroeconomic turbulence. For example, a cost increase of a few percentage points could result in a net loss.