What's the idea?

- Although Generac is the market leader in standby power generators, the company's current penetration rate is only 5.5%.

- A one percentage point increase in penetration could provide Generac with around $3 billion in additional revenue.

- We expect the company to be one of the beneficiaries of the growing solar energy market through its advanced storage solutions.

- Generac's board of directors has approved a new $500 million stock buyback programme, to be implemented within 24 months.

- Generac is trading at a discount to the industry average. According to Wall Street consensus, the stock price has an upside potential of more than 60%.

About Company

Generac Holdings (GNRC) manufactures and sells stationary and mobile standby power generators for residential properties within the Residential Products segment and for commercial and industrial markets within the Commercial & Industrial Products segment. The company also provides solar energy storage solutions.

Why do we like Generac Holdlings Inc?

Reason 1. Market opportunities for standby generators

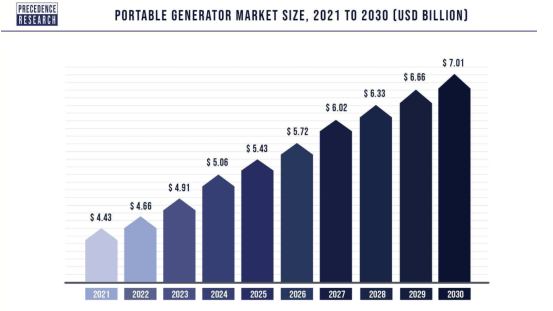

Backup generators currently account for 91% of Generac's total revenue, while clean energy technologies account for only 9%. Although today the generator market is only valued at $4.43 billion, it is expected to reach $7.01 billion in 2030, at a compound annual growth rate (CAGR) of 5.34%.

Expected market dynamics for standby generators

Due to global warming, as well as the aging US energy system, power outages are becoming more frequent. This problem is particularly acute in regions prone to natural disasters, such as Florida, Texas and California. For example, in early autumn, California warned of power outages due to record heat waves. Due to the relatively frequent outages, there is a growing demand for standby generators as households seek energy independence.

Although Generac is the market leader in generators, the company's current penetration rate is only 5.5%. Meanwhile, in the aforementioned markets of Florida, Texas and California, the figure is only 3.5%, while in some states it is as high as 15%-20%. We expect Generac's penetration rate to continue to grow as demand for standby generators grows. According to management, a one percentage point increase in penetration could generate about $3 billion in additional revenue for the company.

Reason 2. Potential for solar energy storage solutions

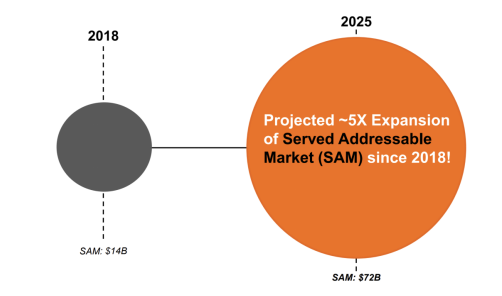

Generac has significantly expanded its target market through organic growth and active M&A deals. According to the company, the target market was valued at $14 billion in 2018 and is expected to reach $72 billion by 2025, suggesting more than five-fold growth. The expected market expansion is driven by growth in the segments of Energy Technology and Smart Grid Ready.

Target market assessment

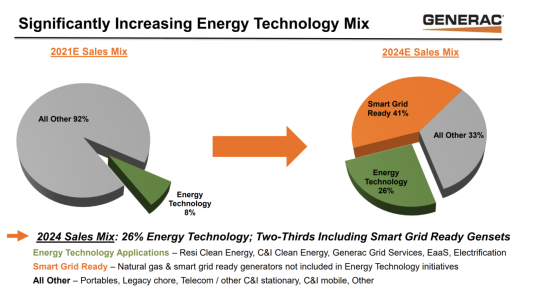

As noted earlier, clean energy solutions account for only 9% of Generac's revenue. However, the revenue mix is expected to change significantly in the coming years. During a recent investor day, the company predicted that the share of clean energy will reach 26% in 2024. The main growth driver is expected to be solar energy storage solutions.

Generac's expected revenue structure

According to Vantage Market Research, the solar energy market is valued at $85.1 billion and is expected to reach $255.3 billion by 2028, which implies a compound annual growth rate of 20.1% over the forecast period. We expect Generac to be one of the beneficiaries of this growth through its advanced storage solutions.

Reason 3. A massive buyback programme

During Q3, Generac repurchased 536,600 common shares for $123.9 million and thus exhausted the limit of the past buyback programme. However, in July this year, the company's board of directors approved a new programme worth $500 million, which is to be implemented within 24 months.

With the company's current market capitalisation at around $6 billion, the programme reduces the number of shares outstanding by 8.3%. Given that the programme is within the stipulated time frame, we expect to see it implemented within the coming quarters.

Financial indicators

Generac's results over the past 12 months can be summarised as follows

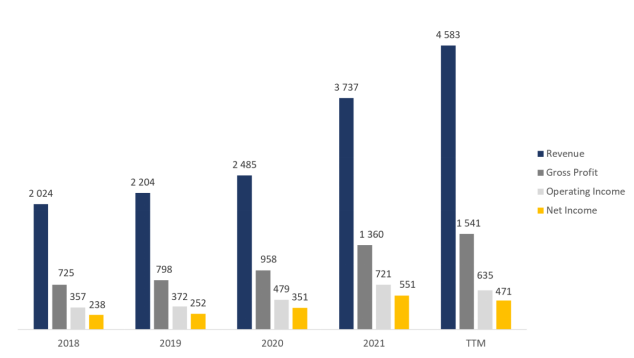

- TTM generated revenue of $4.58 billion, up 22.6% from 2021. The Residential Products segment grew 23.9% to $3.04 billion, while Commercial & Industrial Products grew 18.5% to $1.18 billion.

- Gross profit increased from $1.36 billion to $1.54 billion. Gross margin declined from 36.39% to 33.64% due to inflationary factors.

- Operating profit decreased from $721 million to $635 million, mainly due to an increase in one-off expenses (tax charges, bad debt provisions for a bankrupt customer). The operating margin declined from 19.3% to 13.85% for the year.

- Net profit was $471 million compared to $551 million at the end of the year. Net profit margin decreased from 14.73% to 10.29%.

Company margin dynamics

Company margin dynamics

Since the IPO in 2010, Generac's revenue has grown at an average annual rate of 18%. Total sales are expected to grow 22%-24% year-on-year at the end of the year. We expect gross margins to gradually recover as the impact of inflation diminishes as it slows. Operating margins should also return to the upward trajectory as we overcome headwinds of additional operating expenses.

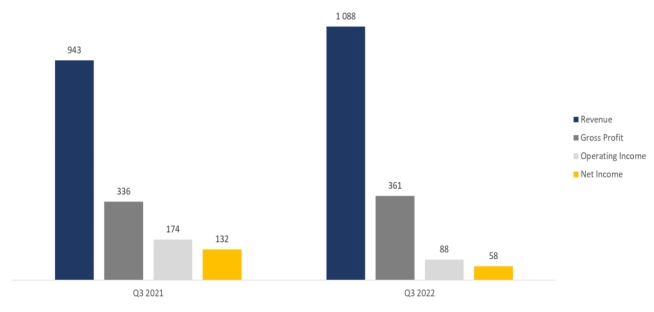

The financial results for Q3 2022 are as follows

- Revenue grew 15.4% year on year, from $943 million to $1.09 billion, with Residential Products up 9.1% to $664 million and Commercial & Industrial Products up 20.5% to $311 million.

- Gross profit rose by 7.5% year on year: from $336 million to $361 million. Gross margin declined by 2.5 percentage points: from 35.64% to 33.18%.

- Operating profit was $88 million compared to $174 million a year earlier. The operating margin declined from 18.42% to 8.04%.

- Net profit was $58 million compared to $132 million a year earlier. Net margin decreased from 13.96% to 5.36%.

Dynamics of the company's financial results

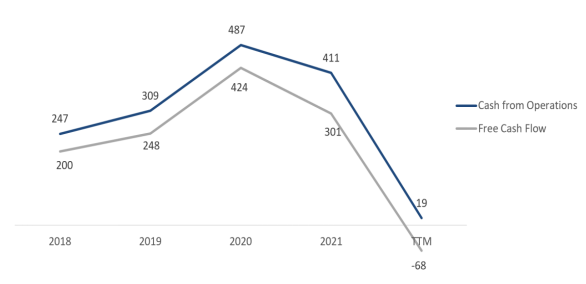

The main factor behind the decline in stock price in recent months has been a significant increase in inventories and the resulting decrease in cash flow. Thus, in the last reporting period TTM operating cash flow amounted to $19 million compared to $411 million for the year. Free cash flow to equity declined from $301 million to -$68 million.

Company cash flow

The company's management attributed the growth in inventories to the cyclical nature of the business and provided a forecast that conditions should recover in the second half of 2023. The market seems to be sceptical about this kind of expectation. However, we remain optimistic about Generac because:

- The company is the undisputed market leader in the generator market, which confirms the opportunistic nature of the expected decline in demand.

- The trends driving growth in Generac's target markets are fundamental and therefore unlikely to change in the medium term.

- The market seems to have more than reflected the expected decline in demand in the price. If management's forecast proves correct and the inventories start to decline in the second half of the year, we will see a significant revaluation of the stock.

Generac has a strong balance sheet: the company has total debt of $1.36 billion, cash equivalents and short-term investments of $230 million and net debt of $1.13 billion, which is 1.4 times TTM EBITDA (Net debt/EBITDA — 1.39x).

Evaluation

Generac trades at a discount to its most closely held companies: EV/Sales — 1.57x, EV/EBITDA — 8.92x, P/Cash flow — 309.21x, P/E — 14.36x, FWD P/E — 13.00x.

Comparable estimate

The minimum price target from investment banks set by Roth Capital is $75 per share. In turn, Guggenheim values GNRC at $180 per share. According to the consensus, the fair market value of the stock is $152 per share, which implies a 45.9% upside potential.

Price targets of investment banks

Key risks

- As noted earlier, Generac is highly cyclical. A deep and prolonged recession could lead to a decline in the company's financial performance and, consequently, a revaluation of its stock.

- There is a possibility that the excessive stockpiling is caused by more fundamental headwinds rather than market conditions. This fact poses risks to our thesis about the temporary nature of the expected slowdown.