What's the idea?

The past decade has been relatively difficult for investors in small-cap stocks as globalization, moderate inflation and low-interest rates have pushed the values of large corporations to new heights. However, it seems that the economic winds have changed their direction. As businesses reorient on domestic production and capital expenditures grow, the US-focused small-cap companies can show impressive results.

About Company

Franklin Covey (FC) provides consulting services related to management, productivity, sales performance, and customer loyalty. The company's solutions enable corporations and educational institutions to achieve better results. Franklin Covey was founded in 1983 and is headquartered in Salt Lake City, Utah.

Why do we like Franklin Covey CoShs?

Franklin Covey operates in a huge and highly fragmented market. According to The Business Research Company, the global management consulting services market is valued at $891.88 billion and is expected to grow at a compound annual rate of 7.9% through 2026 to reach $1.32 trillion at the end of the forecast period. It is worth to be noted that there are no clear leaders in the market — it is dominated by a huge number of independent players, which provides a significant space for Franklin Covey.

Franklin Covey enjoys strong market positioning. The company's solutions allow clients to achieve better results by revising the corporate culture, directions of development, and management methods. The company products’ efficiency is partly reflected in its high customer retention rate, which exceeds 90%. A notable example was a number of companies that doubled their subscription on the All Access Pass (AAP) product during the pandemic. Among the companies was a major new customer, an airline that had its business on hold at the time and wanted to improve its culture with Franklin Covey products. Another client was Best Western, one of the world’s largest hotel chains, whose business has also been affected by the pandemic.

Franklin Covey's business is relatively resilient to macro headwinds. More than half of the company's revenue comes from multi-year contracts that cannot be terminated during their term. The rest of the income comes from one-year, non-cancellable contracts that are paid upfront and close on different days throughout the year, allowing the firm to easily forecast its cash flow.

The targeted acquisitions have allowed Franklin Covey to consolidate its suppliers, providing a significant competitive advantage in the form of a rich content library that is expected to continue to expand. The purchase of Strive in the spring of 2021 allowed Franklin Covey to create its Impact technology platform, automating many processes that were previously performed manually by users. The platform has a best-in-class technology stack combined with an extensive database of educational materials.

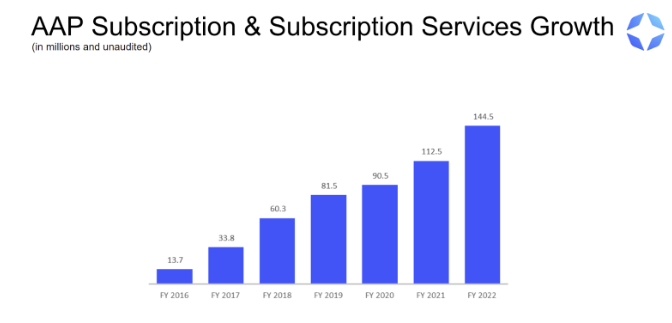

It is worth noting that Franklin Covey is actively increasing revenue from the subscription model. AAP Subscription & Subscription services have grown at a compound annual rate of 81.1% since their launch in 2016. The high share of subscriptions in the revenue structure makes the company's cash flow stable and easily predictable.

AAP Subscription & Subscription services growth

Financial results

FC's financial results for the trailing 12 months (TTM) are presented below:

- At the end of Q1 2023, the company's revenue amounted to $271 million against $262.8 million at the end of the previous year.

- Net profit for the same period increased from $18.4 million to $19.3 million.

- Net margin rose from 7.01% to 7.12%.

- Cash from operations stood at $45.11 million versus $52.25 million in 2022.

- Free cash flow decreased from $46.92 mln to $38.33 mln.

Franklin Covey generates significant cash flow. The decrease in indicators is temporary, as it is due to an increase in net working capital. An increase in receivables will ultimately lead to an increase in the company's revenue.

The company has a strong balance sheet with total debt of $22.27 million, cash and cash equivalents of $58.15 million, and net debt of $35.88 million.

Valuation

Franklin Covey trades at a premium to the industry average: EV/Sales — 2.18x, EV/EBITDA — 17.23x, P/Cash flow — 21.62x, P/E — 34.34x, FWD P/E — 32.42x.

Comparable valuation

The premium valuation is driven by growing revenue, positive margins, and solid cash flow. In addition, the presence of the Impact platform shifts the company's business model from consulting to EdTech. That's why Coursera was added as one of the peers for valuation.

Roth Capital values the company at $71 per share. Northland in turn set its price target at $100 per share. Thus, according to the consensus, the fair market value of the stock is $85.5 per share, which implies a 80.95% upside potential.

Price targets of investment banks

Key risks

The training and consulting services industry is characterized by fierce competition and relatively easy entry. Competitors are constantly introducing new services that may directly compete with Franklin Covey's offerings and may render the company's offerings uncompetitive or outdated.

Although we believe that Franklin Covey trades at a discount to its fair value, the current multiples reflect the market's attitude towards it as a growth company. A slowdown in growth could lead to a significant revaluation of shares.