What's the idea?

The rapid collapse of Silicon Valley Bank and Signature Bank once again proved the destructive power of the bank panic run. The financial system’s stability has become a major concern for many investors. A high degree of uncertainty instantly affected the market value of bank stocks. Amid the increased risks of confidence runs and liquidity shortage, the SPDR S&P Regional Banking exchange-traded fund, which holds the stocks of 140 US regional banks, lost more than 26% of its market value. The Invesco KBW Bank's exchange-traded fund, focused primarily on the large-cap financial stocks, such as JPMorgan Chase, Citigroup, Wells Fargo and Bank of America, lost more than 23% of its market capitalization.

However, apart from banks with heavy accumulated losses exceeding their equity capital, the market underperformers also included first-class financial stocks with healthy safety margins. We have selected bank with strong competitive positions, allowing them to successfully navigate headwinds and provide high returns to their investors: Fifth Third Bancorp (FITB).

Why do we like Fifth Third Bancorp?

According to the Federal Reserve, Fifth Third Bancorp has about $206 billion in assets, making it the 17th largest bank in the US. Considering that Silicon Valley Bank (SVB) was larger than Fifth Third, the size of the bank's assets in itself plays a much less significant role than their quality and the overall balance sheet structure. In terms of balance structure, the collapse of SVB and Signature was due to the following factors:

- During the period of ultra-soft monetary policy, funds from growing deposits were invested in long-term fixed-income securities. As a result of rising interest rates, the bonds have lost a significant portion of their value.

- The exact amount of the accumulated deficit could not be determined because a significant portion of the securities on the balance sheet was classified as held to maturity. The actual value of the securities held was lower than the book value, and this caused devastating consequences when it became necessary to sell them.

- It is estimated that more than 90% of the SVB and Signature deposits were not insured. This is because the maximum insurance coverage from the Federal Deposit Insurance Corporation (FDIC) is $250,000.

Like virtually all US banks, Fifth Third suffered losses on its securities portfolio due to the rising interest rates. However, the losses are not hidden and are well documented on the balance sheet. All Fifth Third’s securities worth $51.5 billion are listed as available for sale. The bank does not hide its losses in the held-to-maturity line, and they can be accurately estimated.

As of the end of the last reporting period, the accumulated deficit amounted to $5.1 billion, while the company's equity was estimated at $17.3 billion. For comparison, SVB's accumulated deficit exceeded the bank's equity.

FITB’s equity and accumulated deficit

The likelihood that depositors will withdraw more than $50 billion is extremely low, even in the event of a massive banking run (following the SVB problems announcement, depositors withdrew $42 billion from the bank). Even under the worst and most unlikely scenario, Fifth Third could not lose more than 30% of its equity.

According to the bank’s 2022 results, its uninsured deposits accounted for only 42% of its total deposits. According to S&P Global, SVB’s share of uninsured deposits was 93.8%, while the figure for Signature was 89.3%. According to the table below, Fifth Third deposits are much more secure than most of those in the US major banks.

Share of uninsured deposits with large banks

Fifth Third stands out by its high-quality loan portfolio. Most of the loans on the bank's balance sheet relate to the real estate and manufacturing sectors. The company has no exposure to the high-risk technology sector, which has been a central part of SVB's loan portfolio. At the end of the last reporting period, the Allowance for Credit Losses (ACL) ratio stood at 1.81% compared to 1.69% a year earlier. Total net losses charged-off increased from 0.16% to 0.19%, but is still relatively low. For comparison, in 2020 the figure amounted to 0.42% of the total loan portfolio.

Fifth Third provides its shareholders with a significant dividend yield. The company distributes $0.33 per share per quarter, which equates to $1.32 per year. Thus, the forward dividend yield is about 5%. Fifth Third directs about 38% of its net profit to dividend payments, that is, the coverage ratio allows the company to maintain and increase payments. However, the bank may revise the payouts policy amid turbulence in the financial industry.

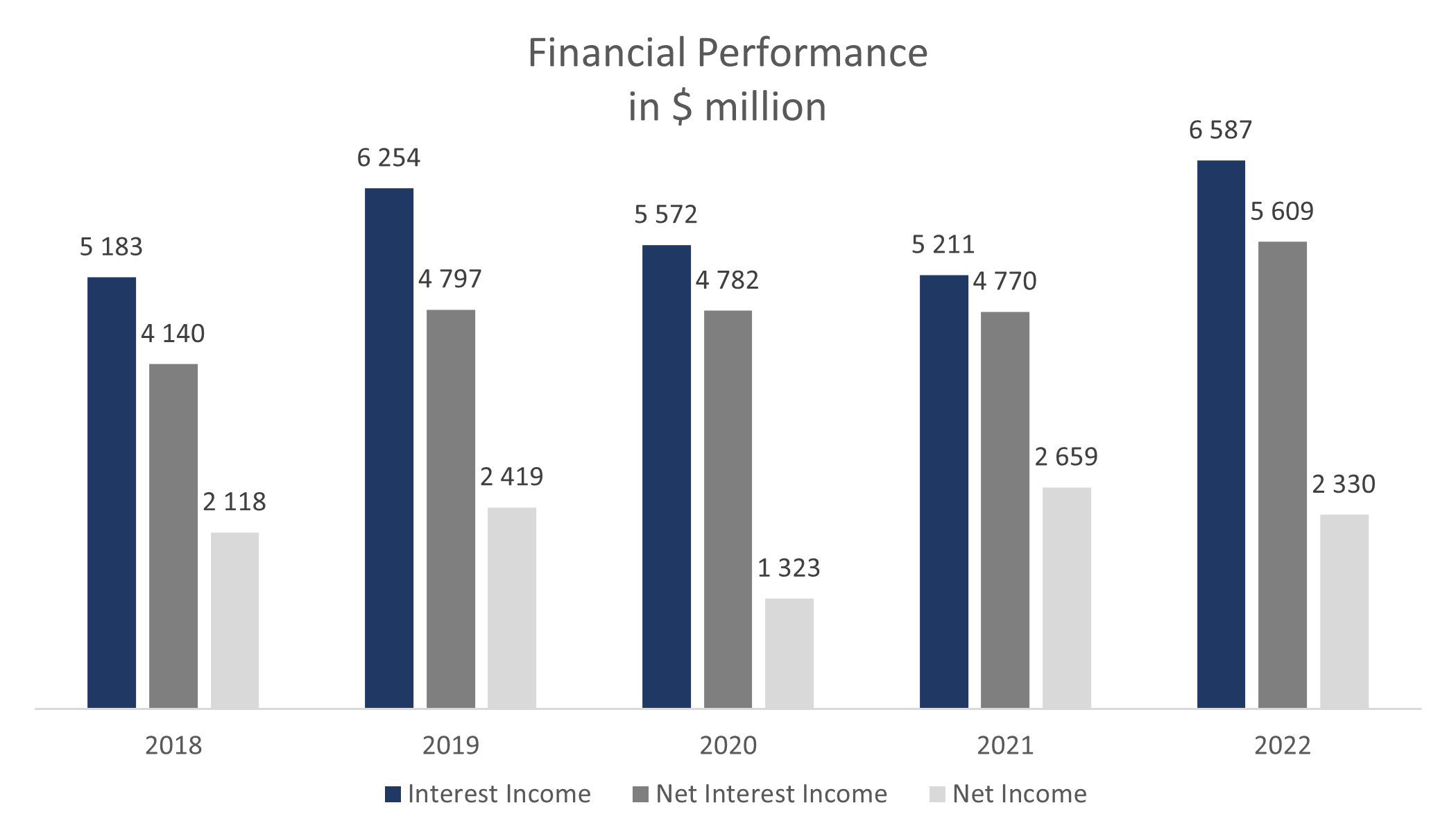

Fifth Third's 2022 financial results can be summarized as follows:

- Interest Income was $6.59 billion, up 26.4% from a year earlier.

- Net Interest Income stood at $5.61 billion compared to $4.77 billion a year earlier.

- Net Income fell from $2.66 billion to $2.33 billion due to higher loan loss provisions.

FITB’s financial performance

- In 2022, the return on assets (ROA) was 1.11% against 1.28% a year earlier.

- The return on equity (ROE) amounted to 11.79% against 11.73% a year earlier.

FITB’s profitability

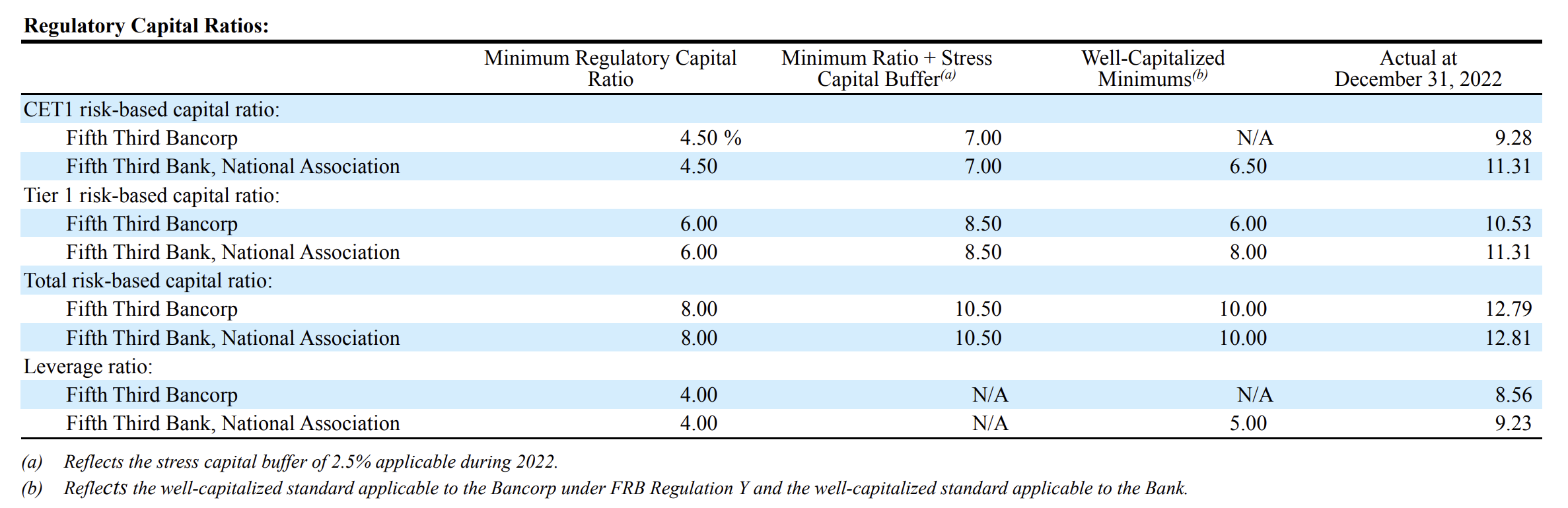

Fifth Third is a well-capitalized bank. The CET1 risk-based capital ratio is 11.31% compared to the required level of 6.50%. Tier 1 capital accounts for 11.31% against a minimum requirement of 8.00%. The total risk-based capital ratio is 12.81% compared to the required rate of 10.00%. The leverage ratio is 9.23% against the regulatory norm of 5.00%.

FITB’s regulatory capital ratios

Fifth Third is trading near industry averages: P/E (TTM) — 7.95x, FWD P/E — 7.22x, P/B — 1.20x. However, FITB is better positioned in the event of deteriorating conditions in the banking industry.

FITB’s comparable valuation

The minimum price target from investment banks set by Piper Sandler is $34 per share. However, Wells Fargo estimates FITB at $41 per share. According to the Wall Street consensus, the stock’s fair market value is $38.5, implying a 49.22% upside potential.

Price targets of investment banks

Key risks

- Although Fifth Third is highly resilient, in the event of a significant outflow of deposits, the bank could face a squeeze in its net interest margin.

- It must be taken into account that investments in the banking industry in the current environment carry high risks. The deterioration of the industry situation and the appearance of signs of another panic run could lead to significant losses for the shareholders of financial institutions.