- Ticker: EVRI.US

- Current price: $17.2

- Target price: $28

- Growth Potential: 62.79%

- Time Horizon: 6-9 months

- Risk: High

- Position size: 1%

The Company

Everi Holdings Inc. offers customers entertainment and technology solutions for the casino and digital gaming industry. The company's business is divided into two segments:

- Games — slot machines, lottery terminals, historical horse racing games and other gaming technology and related services.

- Financial Technology Solutions — financial technology solutions that include access to financial resources and cash transactions through various service channels.

What's the idea?

- A company at the crossroads of the technology and gaming sectors.

- Active acquisitions in 2022, along with positive market trends, will help the company improve its financial performance in the coming periods.

- Adequate leverage will allow share buybacks to continue at a steady pace.

Why might the stock go up?

Reason 1. Positive market trends

In our investment idea story on Boyd Gaming Corporation, we already mentioned about the growth of the gaming sector, with the American Gaming Association reporting record gaming industry revenues. GGR (gross gaming revenue, or the difference between the amount players bet and the amount they win) reached a record $34.27bn in the first seven months of the year ($29.2bn for H1 2022). The increase was 15.5% relative to the same period in 2021.

The positive trends are reflected in Everi's financial results: In Q2 2022, revenue reached a record $197.2 million, with about 74% of revenue attributable to recurring revenues. These are highlighted in purple in the chart below.

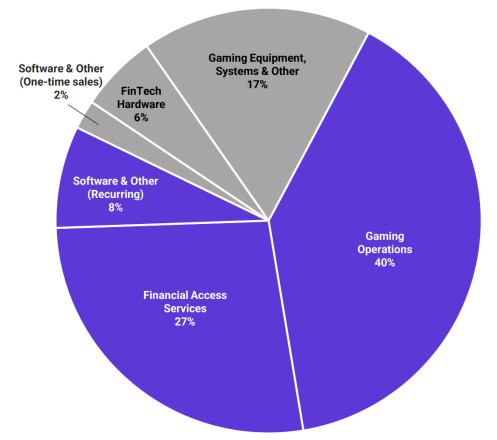

Let's take a closer look at Everi's revenue segments:

- Gaming: 67% of the company's revenue comes from gaming operations, equipment and software. Revenue is generated by placing slot machines on a revenue-sharing basis with casino operators, with over 25% of the machines installed under multi-year contracts.

The positive development of the industry as a whole is directly reflected in Everi's results:

- In Q2 2022, the number of gaming machines installed reached 17,464, a year-on-year increase of 7% (left-hand graph below);

- 8,355 of them are in the premium class, with a year-on-year increase of 20% (top right-hand chart).

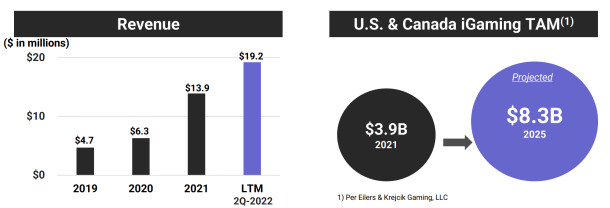

In addition to physical gaming machines, Everi is also developing an iGaming business, which is now attracting attention, including from major players. In April, for example, Brookfield Business Partners acquired the lottery business from Scientific Games for $5.8bn. Everi Holdings itself, citing Ellers & Krejcik Gaming research, forecasts that the total target market for iGaming in the US and Canada will increase from $3.9bn in 2021 to $8.3bn in 2025. Expect the company to aim to 'take a bite' out of that pie and significantly grow revenue through it.

The company's share of revenue in this area is still small, but Everi is growing at a double-digit rate. In Q2 2022, iGaming had an annual growth rate of 38.1%.

FinTech: 33% of revenue is generated from transactional activity under multi-year service contracts (3-5 years) and fintech equipment supplies. The average duration of relationships with Everi's top 30 clients exceeds 12 years. The positive trends in the industry can be seen by looking at the company's transaction statistics: the number and volume of transactions in Q2 2022 for the last 12 months exceeded the results for 2021 (left and right graphs, respectively).

According to a study by The Brainy Insights, this market is expected to grow at a compound annual growth rate of 26.2% over the horizon of 2022-2030. By 2030, the global size of the Fintech industry could reach $936 billion, with the US and Canada accounting for a significant . Thus, the relevance of this area will only increase and, as a consequence, we expect the Everi Fintech segment to continue its positive momentum.

Reason 2. Active business expansion through acquisitions

Everi Holdings sees several key areas for development and is taking active action in these areas:

Diversified game development:

- In March this year, Everi acquired the game development technology and intellectual property of Australian developer Atlas. The acquisition added to Everi's existing game development portfolio and paved the way for future expansion into new international markets.

- On May 3, Everi announced the acquisition of historical racing game developer Intuicode Gaming Corporation. The total deal will be valued at $22m-$27m. The acquisition will enhance Everi's expertise in historical horseracing and help accelerate the development and commercialisation of its extensive portfolio of content in this market.

- In Q2 2022, the company unveiled the new Player Classic Signature slot machine with improved ergonomics and software, which should help entertainment venues attract more customers who prefer modern technology

Expansion of the fintech network:

- Everi continued its expansion into the Australian market in March this year. The company acquired Australian developer and provider of cash handling and financial payment solutions ecash Holdings Pty Ltd. The company's geography includes markets in Australia, Asia, Europe and the US. The deal was valued at AUD$33 million, but could be increased to AUD$43 million if certain growth targets are met. The deal has provided Everi with access to the Australian gaming market as well as an additional customer base in certain US and other gaming markets.

- On 14 April, the company announced the acquisition of certain strategic assets from XUVI LLC, which is a provider of a marketing platform. The platform is designed to assess, target and engage customers in order to increase their loyalty through immersive data analytics. The deal complements Everi Holdings' existing portfolio of loyalty solutions and marketing services to improve their customers' gaming experience and drive revenue growth.

- Last year saw the launch of CashClub Wallet, an app that integrates with the casino's financial system and combines cashless funding with player loyalty tracking

- Other acquisitions: The company is also interested in complementary businesses that can be scaled by leveraging existing resources and distribution networks to generate revenue and additional cash flow. For example, on October 4, Everi Holdings announced an agreement to acquire certain assets of Venuetize, offering mobile technology solutions, guest engagement and m-commerce platform for the sports, entertainment and hospitality industries. This acquisition will expand Everi's target market beyond the casino gambling business for the first time, as well as increase the company's technology capabilities in new markets and geographies. We expect Venuetize's complementary assets and established customer base to provide further growth through overlapping marketing opportunities with Everi Holdings' existing customers, which will have a positive impact on the value of the company.

- International expansion: as seen in the Atlas and ecash deals, the company is further diversifying its business by country while expanding its target market.

- iGaming: Everi plans to leverage its portfolio of 'physical' games and future cash flows from digital games to on the expansion of the iGaming industry.

Financial indicators

The company's results for the last 12 months:

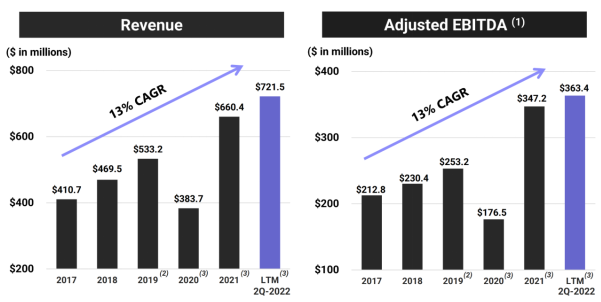

TTM revenue: up from $543.4m to $721.5m

TTM operating profit: up from $129.6m to $210.1m

in terms of operating margins, an increase from 23.8% to 29.1% due to a decrease in the cost of revenue from 40.9% to 35.4%

TTM net profit: up from $57m to $160.2m

in terms of net margin, up from 10.5% to 22.2%

Operating cash flow: up from $238.1m to $302.4m thanks to better earnings

Free cash flow: up from $142.5m to $186.8m

Based on the results of the most recent reporting period ended 30 June 2022:

Revenue: up from $172.6m to $197.2m

Operating profit: up from $54.4 million to $54.6 million

in terms of operating margins, a decrease from 31.5% to 27.7%, mainly due to an increase in the cost of revenue from 35.5% to 37.3%

Net income: down from $36.2m to $32.5m:

in terms of net margins, a decrease from 21% to 16.5%, mainly due to an increase in income tax from 0.2% to 4.9%

Operating cash flow: up from $51.9m to $69m

Free cash flow: up from $22.7m to $32.6m

Everi has shown good financial results both for the last 12 months and for Q2. Despite a temporary decline in profitability, the company still generates good margins. We expect the level of the indicator to increase in the future due to the implementation of integrations with acquired companies.

- Cash and cash equivalents: $251.7 million

- Net debt: $728.1 million

- Net debt/EBITDA: year-on-year decline from 2.99x to 2.22x. In terms of Net debt/adj. EBITDA is at 2.5x.

Everi Holdings has sufficient financial strength through stable cash flows and an acceptable level of debt, which the company is gradually reducing.

Valuation

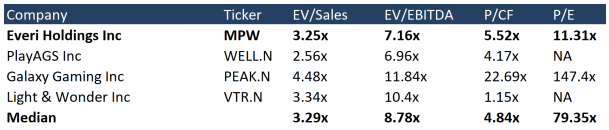

In terms of trading multiples, the company is undervalued compared to its peers on all metrics except P/CF (5.52x vs. 4.84x)

At the end of the first quarter, Everi Holdings Inc. announced the launch of a $150m buyback programme over 18 months. During the second quarter, the company has already carried out a $33.3m buyback, leaving approximately $116.7m, which represents ~7.5% of the company's market capitalisation.

Ratings of other investment houses

The minimum price target set by Stifel Nicolaus is $24 per share. B. Riley has set a target price of $35. According to consensus, the fair value of Everi is $28.75 per share, which implies a 62.79% upside potential.

Key risks

- The worsening economic climate may force some customers to reduce their spending in casinos, which could also have a negative impact on Everi's revenue. However, the company is partly covering this risk by entering into multi-year contracts.

- Continued action to ease restrictions in Macao could result in some customers migrating to markets where Everi does not already offer its services.

How to take advantage of the idea?

- Buy shares at a price of $17.2.

- Allocate no more than 1% of your portfolio for purchase. To compile a balanced portfolio, you can use the recommendations of our analysts.

- Sell when the price reaches $28.