- Ticker: DBX.US

- Entry price: $20.9

- Target price: $30

- Growth potential: 43.54%

- Time horizon: 9 months

- Risk: Moderate

- Position size: 2%

The Company

Dropbox Inc. (DBX) provides a cloud platform that enables users to create, store, share and collaborate on content. The company serves more than 700 million users in 180 countries. Dropbox was founded in 2008 and is headquartered in San Francisco, California.

What's the idea?

- The global cloud storage market is expected to grow at a high rate until 2029. As a major player in the industry, Dropbox has significant room for expansion.

- Dropbox has managed to build a competitive moat and establish itself as a strong player, increasing the number of registered and paying users over the years.

- Through a combination of tools such as Shop, DocSend and HelloSign, Dropbox can become an attractive one-stop service provider for content creators, freelancers, small and medium-sized businesses.

- Dropbox has been actively buying back and is likely to continue to do so, as founder and CEO Andrew Houston still owns a significant stake.

- Despite slowing revenue growth, Dropbox has strong margins, impressive cash flow and a strong balance sheet.

- According to the Wall Street consensus, Dropbox stock is trading at a significant discount to fair value.

Why might the stock go up?

Reason 1. Large and growing market

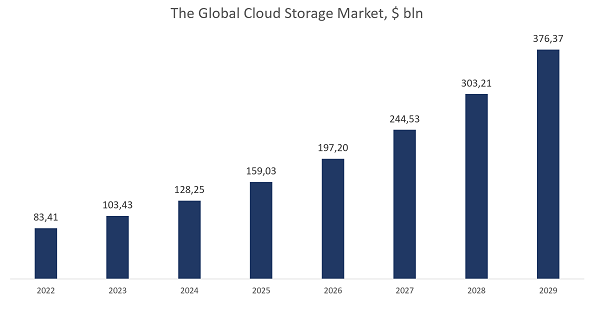

According to Fortune Business Insights, the global cloud storage market is valued at $83.41 billion and is expected to grow at a compound annual growth rate of 24% to reach $376.37 billion by 2029. The growing popularity of remote mode of operation serves as one of the major growth drivers for the industry. Cloud storage enables organisations to support remote working as well as manage vast amounts of data seamlessly.

Demand for low-cost storage, backup and data protection is driving market growth in the enterprise segment, including small, medium and large enterprises. By focusing on a 'budget' format for cloud storage and security, Dropbox is following established trends and responding to key requests from current and potential users.

A large and growing market provides significant room for growth for cloud storage companies. In addition, a growing market gives innovative companies the 'right to make a mistake' — the loss of market share can be more than compensated for by the high growth rate of the target market.

Reason 2. Competitive positioning

Dropbox competes with both the technology giants Google and Microsoft and the relatively small company Box. As much larger companies, Microsoft and Google can invest more financial resources in the development of their products. Box, on the other hand, offers cheaper solutions. Nevertheless, Dropbox has managed to build a competitive moat and establish itself as a strong competitor, increasing the number of registered and paying users over the years. So what makes the company so attractive?

Firstly, it is an open ecosystem. Dropbox works on all devices and operating systems, and gives users the ability to integrate with Zoom, Adobe, Slack, Salesforce, BetterCloud, Atlassian and all the same Microsoft and Google. Microsoft and Google's solutions, on the other hand, are closed, which deprives customers of flexibility.

Secondly, Dropbox features an extensive digital infrastructure that allows documents to be analysed through the DocSend tool and signed through the HelloSign tool.

Thirdly, the company pays great attention to security and reliability. Dropbox has created several layers of data protection and built a unique infrastructure to ensure a high degree of data security.

Thanks to its strong positioning, Dropbox is growing its user base without incurring additional sales and marketing costs. For example, at the end of the first half of 2022, sales and marketing expenses as a percentage of revenue were 17.7% compared to 19.5% a year earlier.

Reason 3. New growth strategy

The company has noticed that digital content creators are increasingly selling their products on marketplaces but saving them on cloud platforms like Dropbox. In April 2022, Dropbox launched a new product, Dropbox Shop, which allows creators to sell downloadable content. The new product will allow Dropbox to become a beneficiary of the booming creative economy and differentiate its offering. By doing so, the company is able to expand its user base and increase the share of paying customers, which is already showing steady growth.

Through the combination of Shop, DocSend and HelloSign tools, the company can become an attractive one-stop service provider offering cloud storage, free document management, digital signatures and a marketplace for content creators, freelancers, small and medium-sized businesses.

Reason 4. Active stock buyback

Dropbox regularly repurchases its stock to return value to shareholders. For example, Dropbox bought back $214 million worth of shares in the last quarter. Earlier, the board of directors approved a $1.2 billion buyback programme, which exceeds 16% of the company's current capitalisation.

One of the reasons Dropbox is buying back its shares is that co-founder and CEO Andrew Houston still owns 25.62% of the company. We view such significant insider ownership positively, as it may indicate management's confidence in the long-term prospects of the company.

Financial indicators

Dropbox has seen a steady rate of growth in its financial performance over the past few years. The results for the past 12 months can be summarised as follows

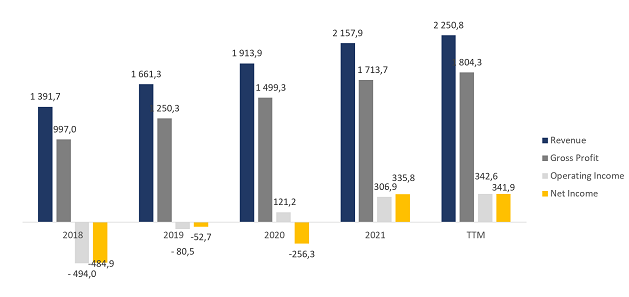

- TTM generated revenue of $22508 illion, an increase of 4.3% over 2021. The growth was driven by both an increase in the number of paid users and an increase in average revenue per user (ARPU).

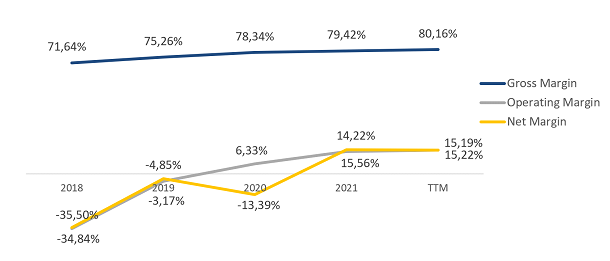

- Gross profit rose 5.3% in the latest reporting period, from $17137illion to $18043illion. The gross margin was 80.16% compared with 79.42% for the year-ago period.

- Operating profit increased by 11.6%: from $306.9 million to $342.6 million. Operating margin increased from 14.22% to 15.22%.

- Net profit rose from $335.8million to $341.9million. Net profit margin was 15.19% compared to 15.56% for the year.

Management expects revenue to be in the range of $2308ilion-$2318illion by 2022, representing growth of 6.9%-7.4% year-on-year. Gross margin is expected to reach 81.5% and operating margin to 30%.

The financial results for the first half of 2022 are as follows

- Revenue rose 8.9% year on year, from $1042.2 illion to $1135.1 illion.

- Gross profit increased by 11.0% year-on-year: from $825.8 million to $916.4 million. Gross margin increased by 1.5 percentage points: from 79.24% to 80.73%.

- Operating profit was $172.4 million compared to $126.9 million a year earlier. The operating margin increased from 12.18% to 15.19%.

- Net profit rose from $135.6million to $141.7million. Net margins decreased by 0.5 percentage points: from 13.01% to 12.48%.

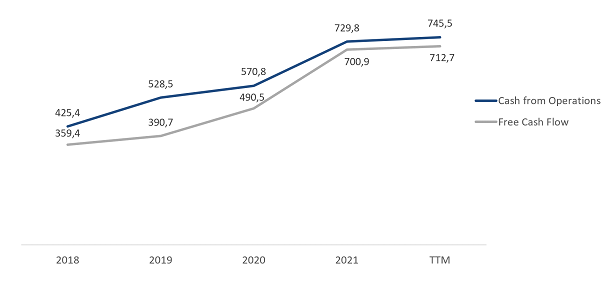

At the end of the latest TTM reporting period, operating cash flow was $745.5 million compared to $729.8 million for the year. Free cash flow to equity increased from $700.9 million to $712.7 million.

Dropbox has a strong balance sheet: total debt is $2316illion, cash equivalents and short-term investments account for $1446illion, net debt is $869.8million, slightly above TTM operating cash flow. The Net Debt / EBITDA multiple is 1.74x.

Evaluation

Dropbox trades at a discount to the industry average: EV/Sales — 3.39x, EV/EBITDA — 15.19x, P/Cash flow — 9.98x, P/E — 19.13x.

The minimum price target from investment banks set by Citigroup is $24 per share. Bank of America, on the other hand, values DBX at $34 per share. By consensus, the fair market value of the stock is $30 per share, suggesting a 43.54% upside potential.

Key risks

- Dropbox's strategy of attracting freelance content creators and SMEs is not without its drawbacks. Small businesses tend to be more agile, causing their average churn rate for SaaS companies to be 31%-58% 6%-10% for large corporations. Dropbox's inability to retain this customer segment could lead to a decline in the company's financial performance and stock price.

- Although Dropbox has been successful against the giants so far, losing ground in a highly competitive market is a key risk factor. This factor could affect the company's ability to grow organically in the long term and lead to a significant revaluation of its stock.

How to take advantage of the idea?

- Buy shares at a price of $20.9.

- Allocate no more than 2% of your portfolio for purchase. To compile a balanced portfolio, you can use the recommendations of our analysts.

- Sell when the price reaches $30.