What's the idea?

- DigitalOcean is a growth company operating in the cloud computing industry and providing startups and SMBs with a range of PaaS, IaaS and SaaS offerings.

- Boosted by COVID-19 pandemic, the cloud computing industry is set to grow exponentially in the coming years due to the business transformation, better security and improved productivity advantages that it offers to various businesses.

- DigitalOcean has a diversified product portfolio and more than 600,000 constant clients globally. It has been growing rapidly over the last several years, but currently, amid ongoing market headwinds, the company’s revenue growth rates are slowing down.

- DigitalOcean has recently made two important acquisitions that could shape the company’s future if the entities are successfully integrated into existing business.

- Despite the growth slowdown, the company’s management targets high margins and is committed to a share buyback program that could prop up the stock price during economic and industry fluctuations.

About Company

DigitalOcean Holdings (DOCN) is a leading cloud computing platform offering on-demand infrastructure and platform tools for startups and small and medium-sized businesses (SMBs). The company provides cloud computing solutions, including platform-as-a-service (PaaS), infrastructure-as-a-service (IaaS) and software-as-a-service (SaaS) offerings, that enable developers to deploy and manage applications on scalable servers along with various services for streamlined development. The company’s platform is designed to empower developers with efficient infrastructure to build, test, and deploy their applications without the complexities of traditional infrastructure management. The company was founded in 2012, went public in 2021, and is headquartered in New York.

Why do we like DigitalOcean Holdings?

Reason 1. Cloud computing market is set to flourish in long-term

DigitalOcean is a leading cloud computing platform offering on-demand infrastructure and platform tools for startups and small and medium-sized businesses. Cloud computing is revolutionizing how companies across the globe develop and deploy applications. The cloud offers lower upfront cost and superior flexibility, extensibility and scalability as compared to on-premise software development environments. DigitalOcean’s platform simplifies cloud computing, providing solutions that are easy to leverage, broadly accessible, reliable and affordable, so that its clients could benefit from transformative effects of the cloud, such as rapid acceleration of innovation, and increase in productivity and agility.

The global cloud computing market has witnessed a rapid growth over the past years, especially amid COVID-19 pandemic and worldwide lockdowns, since cloud computing helps enterprises overcome the challenge of running business operations online and organizing efficient remote work, connecting teammates from all corners of the world. As a result, enterprise spending on cloud infrastructure services, encompassing infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS) segments, has soared from $96 billion in 2019 to $225 billion in 2022, up by 2.3 times over just three years.

Despite returning to the normal state of life after long-lasting lockdowns, the global cloud computing market has a number of other factors that are likely to drive the sector’s growth in the coming years. The EY research indicates the following top-3 business drivers for moving to cloud:

- Business growth and transformation. Cloud computing allows companies to adapt business operations easier and faster, reducing operational and capital expenditure, while increasing data processing speed.

- Security and data privacy. Cloud solutions providers offer important backup infrastructure and recovery facilities without the need to install data centers, as well as security services such as data encryption, authorization management, and access control.

- Workplace productivity. Applying cloud computing solutions, both big corporations and startups can connect teammates from all corners of the world and organize their remote work in an efficient and productive way.

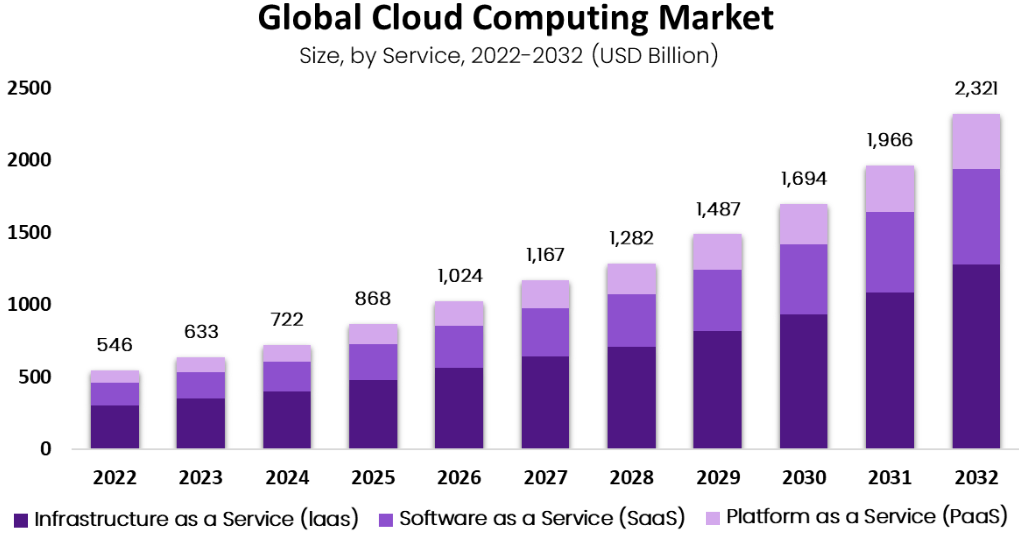

In addition, the recent boom in artificial intelligence (AI) has highlighted the necessity for companies to tap into machine learning and AI capabilities, and integrate them into their own services in order to keep up with competitors. As a result of these long-term trends, Market.US forecasts the global cloud computing market, comprised of IaaS, PaaS and also software-as-a-service (SaaS) segments, to reach around $1,167 billion in 2027 and $2,321 billion in 2032. Given the market’s size of $546 billion in 2022, its CAGR will constitute 15.6% during the forecast period.

Global cloud computing market forecast

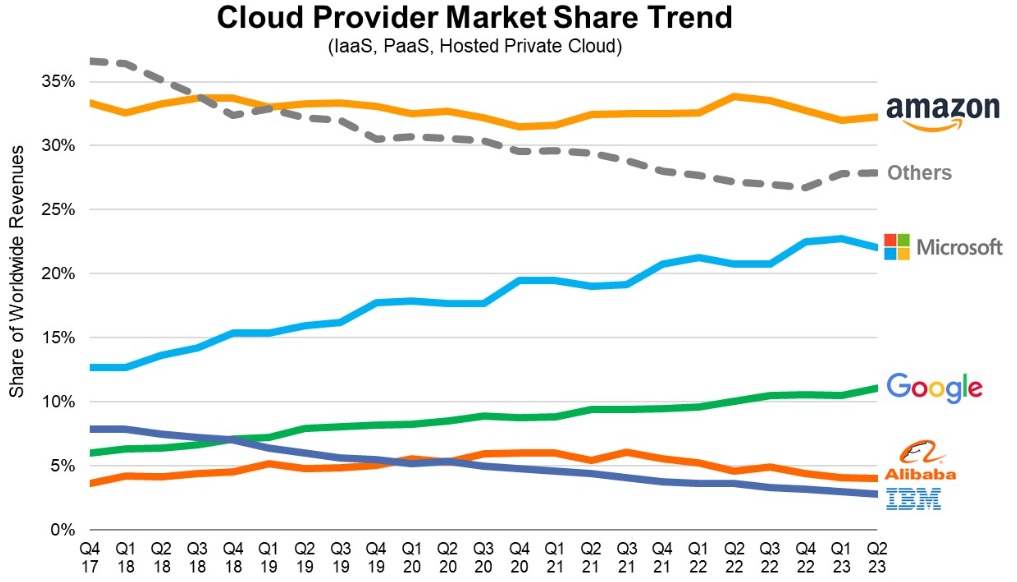

The cloud computing market is dominated by three tech-giants such as Amazon (Amazon Web Services), Microsoft (Azure) and Google (Google Cloud). They have been gradually overtaking the market over the past years, and as of Q2 2023, their total market share amounted to 65%, with Amazon at the top (32%), followed by Microsoft (22%) and Google (11%). The rest of the market (35%) is subject to a quite severe competition among several dozens of companies, each trying to gain its share and specialize on certain customer categories. Among the tier two cloud providers, those with the highest year-on-year growth rates include Oracle, Snowflake, MongoDB, VMware, Huawei and China Telecom.

Cloud provider market share trend

In 2023, the growth rate in cloud spending continues to nudge down, driven by macroeconomic pressures, some belt-tightening by enterprises, local market issues in China, and, above all else, the big data regulation. According to the recent research by Synergy Research Group, in Q2 2023, global enterprise spending on cloud infrastructure services (including IaaS, PaaS and hosted private cloud) was close to $65 billion, up by 18% year-on-year, while in Q1 2023 and Q4 2022 the year-on-year growth rates were 19% and 20%, respectively. However, in absolute terms the market has been growing by $10 billion YoY for the third successive quarter. Thus, it is expected that cloud services providers will overcome short-term challenges, many economic pressures will ease, and the cloud market’s future growth rates will remain buoyant.

Reason 2. Strong market position in cloud computing for SMBs and AI opportunities

As a cloud computing solutions provider, DigitalOcean, operates at the same market as big-tech companies do but targets startups and SMBs rather than large enterprise customers. The company has managed to find its niche, offering startups and SMBs, which typically have more limited financial resources, operational expertise and IT personnel, simpler and cheaper solutions that allow them to rapidly build, deploy and scale, whether creating digital presence or building digital products, while spending less time managing their infrastructure and more time building innovative applications that drive business growth. DigitalOcean has developed user-friendly and cost-effective cloud solutions across all segments:

- Infrastructure-as-a-Service (IaaS) segment includes compute (Droplets), storage (Object Storage, Block Storage, and Backups) and networking (Cloud Firewalls, Managed Load Balancers, and Virtual Private Cloud) products.

- Platform-as-a-Service (PaaS) segment offers infrastructure as well as database management systems, application platforms, development tools and other services designed to support the complete web application lifecycle: Managed Databases, Managed Kubernetes and Container Registry, App Platform, Functions, etc.

- Software-as-a-Service (SaaS) segment is represented by Managed Hosting and Marketplace offerings.

DigitalOcean’s customer base is diverse with respect to technical competency, type of business, use case and geography. It includes software engineers, researchers, data scientists, system administrators, students and hobbyists, who use the company’s platform for a wide range of use cases, such as web and mobile applications, website hosting, e-commerce, media and gaming, personal web projects, and managed services, among many others. DigitalOcean’s customers are spread across over 190 countries, and about two-thirds of its revenue has historically come from customers located outside the United States. The company has no material customer concentration, as its top 25 customers provide 10% of the revenue in 2022.

DigitalOcean geographical expansion and revenue breakdown

As of June 30, 2023, DigitalOcean had approximately 616,000 customers (excluding Testers on an aggregate basis), classified into four categories, depending on their monthly payments and lifecycle:

- Testers — customers paying less than $50 per month, using DigitalOcean platform for less than three months and contributing revenue of approximately $1 million per month.

- Learners — customers paying less than $50 per month and using DigitalOcean platform for at least three months. As of June 30, 2023, DigitalOcean had 466,000 Learners (75.6% of all customers, excluding testers). From the deep pool of Learners, many companies grow their businesses and become Builders and Scalers.

- Builders — customers paying $50–$500 per month and using DigitalOcean platform on average for four years. As of June 30, 2023, DigitalOcean had 134,000 Builders (21.8%).

- Scalers — customers paying more than $500 per month and using DigitalOcean platform on average for six years. As of June 30, 2023, DigitalOcean had 16,000 Scalers (2.6%).

While constituting the lowest share in total number of customers, Builders and Scalers contribute 85.9% to a monthly revenue, since they represent the SMBs that are actively developing and gaining traction, and are most likely to continue to scale on DigitalOcean platform and purchase additional products. Therefore, the company focuses on go-to-market and product initiatives aimed at attracting, retaining and expanding business from Builders and Scalers. Over the past six months, Builders and Scalers segments increased from 144,000 to 150,000 customers, up by 4.2%, and their total revenue rose from $47 million to $49 million, up by the same 4.3%.

DigitalOcean customer base and monthly revenue

Despite the growing customer base and monthly revenue in absolute terms, DigitalOcean has faced declining growth rates. First, net dollar retention rate (NDR), a measure of the share of the current annual recurring revenue (ARR) linked to the customer base that was active in the previous period, fell from 107% in Q1 2023 to 104% in Q2 2023, which is a drastic decline comparing to 112% in Q2 2022. During the earnings conference call the company’s management warned that NDR will likely decline to 90%–95% in the Q3 2023 due to “cloud optimization” headwinds.

Secondly, YoY revenue growth rates have decreased for the second quarter in a row, from 28.0% in Q4 2022 to 11.6% in Q2 2023. As a result, the management has revised downward its FY 2023 revenue projection, with the forecast revenue set between $680 million–$685 million, down from $700 million–$720 million, while revenue growth rate is expected at 18%, down from 34% in FY 2023. DigitalOcean was able to continue to boost average revenue per user due to its price increases implemented last year, but nevertheless, it indicates the problems with its organic growth and the broad weakness that the technology market is currently facing.

DigitalOcean changes in FY 2023 guidance

These negative trends are occurring despite the two big acquisitions, of Cloudways and Paperspace, made within the past year. The $350 million acquisition of Cloudways, a leading managed cloud hosting and SaaS provider, was completed in H2 2022. The deal was aimed at strengthening DigitalOcean’s core business and product portfolio, and expanding the addressable cloud market. Indeed, it has expanded the company’s customer base by 18%, but as recent financial results showed, has not helped the company to accelerate revenue growth by now.

DigitalOcean's newest acquisition is the $111 million deal to buy Paperspace, which allowed DigitalOcean to expand its portfolio with an AI/ML dimension. Paperspace adds 12,000 paying customers (2.0% of total customer base) and creates cross-selling opportunities, so in the long run, the AI business may generate triple-digit revenue growth and become a large part of DigitalOcean's revenue, proving the rationale behind the acquisition. In the short term, however, this deal appears to further increase the company’s net debt that has almost tripled over the past year, from $300.4 million as of June 30, 2022 to $923.5 million as of June 30, 2023.

On the one hand, when a company is undergoing significant transformations or engaging in numerous acquisitions instead of pursuing organic growth, it could raise concerns. On the other hand, DigitalOcean's management confirmed its commitment to prioritizing the integration of Cloudways and Paperspace in the near term, which can boost DigitalOcean's financial results in the coming quarters. Thus, given a higher interest rate environment and increased net debt burden, it would be prudent to concentrate on boosting growth through internal drivers rather than aggressive M&A strategy.

Reason 3. Higher margins and share buybacks to compensate for growth rate slowdown

While the company’s management stated uncertainty regarding when macro headwinds would subside, they did state that they intend to offset any deceleration in growth rates with big improvements in profitability. Adjusted EBITDA margin is forecasted to grow from 34% in FY 2022 to 38.5% in FY 2023, and free cash flow margin is seen to increase by 8.5% to 21.5% over the same forecast period. Given that the management initially had been targeting 2024 as the year of delivering a 20%-plus free cash flow margin, achieving this important milestone a year earlier would enable the company to generate attractive returns on the investors’ capital regardless of the revenue growth rate, and in general a good sign.

DigitalOcean margins forecast

Moreover, the management outlined a resounding commitment to its buyback program. Over the past two years, the company has repurchased more than 27 million shares (22.9% of the total diluted weighted average shares outstanding as of December 31, 2022) for $1.3 billion (around 54% of the current market capitalization). All purchased shares were subsequently redeemed. However, it has not impacted the total number of diluted shares outstanding since the buyback program barely compensated for the excess of the shares granted to employees under the employee stock ownership plan (ESOP) that increased from 61.6 million in 2021 to 105.8 million in 2022. As a result, despite the 2022 buyback program, the number of diluted weighted average shares outstanding stood at 118 million, the same amount as of December 31, 2021.

DigitalOcean is aiming at shares outstanding to stand at around 106 million by the end of 2023, down from 118 million as of the earlier 2/16/2023 guidance, which means a decline of 10.2%. The company repurchased additional 7.76 million shares for $266 million in Q1 2023 and 2.8 million shares in Q2 2023 for $103 million at an average price of $37.08 per share, ending Q2 2023 with the number of fully diluted shares outstanding of 105 million, down from 120 million in Q2 2022. During the conference call, the management indicated that they may moderate the magnitude of buybacks from 2023 levels but still confirmed commitment to capital return to shareholders through share repurchases going forward. While generally a good sign of the management’s confidence in the company’s resilience and future perspectives, it is a big question whether using capital for share buyback is currently the most efficient allocation of capital since over the past two years, it has boosted neither the DigitalOcean share price nor its EPS.

Thus, DigitalOcean appears to be quite a risky investment. Reduction of revenue and revenue growth rate guidance in FY 2023 reflects the challenging macro environment in the SMB space and slowing growth in the cloud industry that the company is currently facing. However, if DigitalOcean manages to successfully incorporate newly acquired businesses into its perimeter and achieve the targeted synergies effects, the company may return to 20%+ revenue growth rates in 2024 regardless of the SMB market environment changes.

Financial performance

DigitalOcean 2022 financial results can be summarized as follows:

- Revenue increased from $428.6 million in 2021 to $576.3 million in 2022.

- Gross profit grew from $258.0 million to $364.4 million YoY.

- The company is still operationally unprofitable, but performance has been steadily improving over the last years — in 2022, operating loss accounted for $9.7 million, down from $10.4 million in 2021 and $14.6 million in 2020.

- Net loss slightly increased from $19.5 million in 2021 to $24.3 million in 2022, mainly due to a one-time sale of group companies with a loss of $14.9 million.

- Nevertheless, DigitalOcean generates positive cash flows. Operating cash flow increased from $133.1 million to $195.2 million YoY. Free cash flow also soared from $24.0 million in 2021 to $69.5 million in 2022.

Dynamics of annual financial results

Dynamics of annual financial results

DigitalOcean's financial performance in H1 2023 is presented below:

- Revenue increased from $261.2 million to $334.9 million YoY.

- Gross profit grew from $166.2 million to $195.7 million YoY.

- Operational performance demonstrated positive dynamics — after an operating loss of $19.8 million in H1 2022, the company earned $7.9 million of operating profit in H1 2023.

- Net loss increased to $34.3 million in H1 2023 versus $25.3 million a year ago. Much of this net loss is attributable to the so-called restructuring charges, a one-time expense occurred in the Q1 2023. In Q2 2023, DigitalOcean managed to show a minor profit of $0.7 million.

Despite overall positive results in H1 2023, the company’s management projects certain challenges in the coming months due to ongoing market headwinds, and therefore, cut its guidance for 2023, with revenue, revenue growth rate and non-GAAP diluted EPS lower by 5%–15% compared to what was expected in May 2023.

Dynamics of half-year financial results

DigitalOcean’s balance sheet causes some concerns due to increased leverage:

- The leverage ratio, defined as the ratio of total debt to assets, stands at 98%, which means that its debt is almost equal to its assets. The figure is much higher than the cloud providers average of 3%–67%.

- Total debt has not changed significantly over the last year — it accounted for $1,467 million as of June 30, 2022 versus $1,474 million as of June 30, 2023. However, due to M&A deals, the company’s net cash position has plummeted. While the company reported cash and short-term investments of $1,166 million in Q2 2022, the figure decreased to $550,5 million in Q2 2023, which results in the company's net debt of $923.5 million.

- The net debt/EBITDA ratio sets at about 10.0x (Net Debt/EBITDA is 10.0x). If FY 2023 adjusted EBITDA forecasted by the company is applied, the ratio falls to 3.5x (TTM Net Debt/Adjusted EBITDA is 3.5x).

- Cash flow from operations has been steadily increasing from year to year, with a CAGR of 70% over 2019–2022. In H1 2023, DigitalOcean earned $100.4 million of operating cash flow, up by 31.3% YoY.

Stock valuation

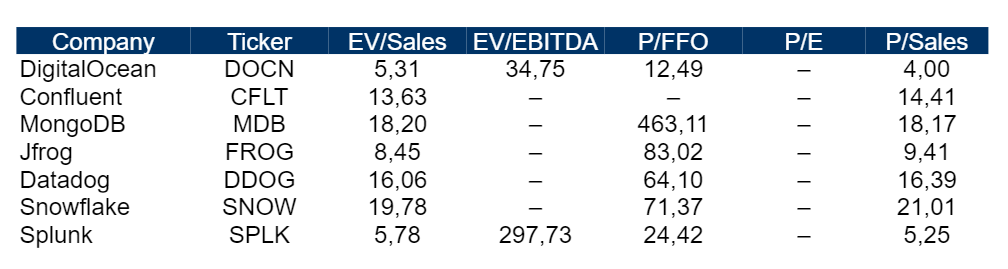

DigitalOcean trades at a discount to the average multiples of cloud computing providers: EV/Sales — 5.31x, EV/EBITDA — 34.75x, P/FFO — 12.49x, P/Sales — 4.00x. This discount can be partly explained by higher growth rates of some competitors compared to DigitalOcean. However, DigitalOcean is on track towards operational profitability, has steadily growing cash flows, and, therefore, offers the best return per unit of risk taken.

Comparable valuation

The minimum price target set by Stifel, Nicolaus & Company is $25 per share, while Bank of America values DigitalOcean at $58 per share. According to the Wall Street consensus, the share’s fair market value stands at about $41, implying 63% upside potential.

Price targets of investment banks

Key risks

- Cloud computing market is a highly competitive area. The company should timely update its products and release new features, adapt and respond effectively to rapidly changing technology, evolving industry standards, otherwise it will lose its competitive position.

- Global economic slowdown and unfavorable conditions in the cloud computing industry may lead to reductions in information technology spending, which will negatively affect DigitalOcean’s business and results of its operations.

- Since DigitalOcean is a growth company, its financial results may fluctuate significantly, making it difficult to project future results. Consequently, its stock price is highly sensitive to the expectations of securities analysts and investors.

- The company’s increased leverage could adversely affect its financial condition and the ability to raise additional capital to fund future operations.