What's the idea?

The digitalisation of companies, in addition to new horizons for business, also opens up new opportunities for criminals. Based on expert forecasts, we expect demand for cyber security products to grow. We suggest that investors diversify their portfolios by adding stocks in this area so as not to miss out on possible profits. We have selected two companies that can show good returns: Rapid7, Inc. and Datadog, Inc.

About Company

Datadog offers its customers a platform for monitoring and securing cloud applications under the Software as a Service (SaaS) model. The company generates revenue from monthly or annual subscriptions. In addition to subscriptions, customers also have the option to purchase additional products such as customizable metrics kits, anomaly detection kits, etc. Datadog uses a Land-and-Expand business model, which involves offering easily deployable products to 'capture' a large number of customers and then expand their reach with additional applications.

Why do we like Datadog Inc?

Reason 1. The growth of the cloud industry

In addition to increased demand for its products due to the general digitalisation of potential customers, Datadog may benefit from business migration to the cloud and an increase in the number of users adopting next-generation DevOps. Gartner estimates that cloud spending as a proportion of total IT spending will increase from ~10% at the end of 2022 to ~17% in 2026.

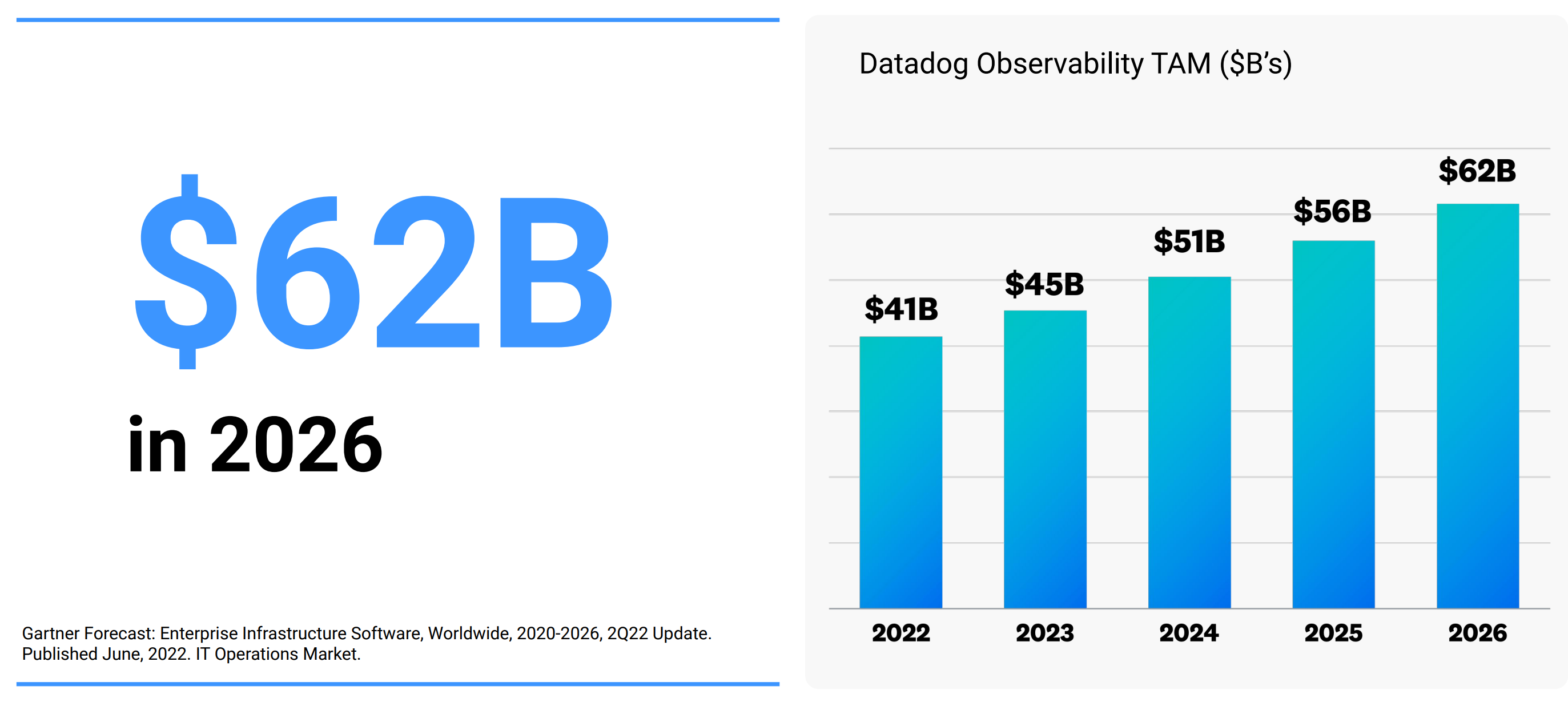

Datadog, which cites Gartner research, predicts the total target market for its key Datadog Observability product will increase from $41 billion to $62 billion over the 2022-2026 horizon.

This increase is a good opportunity for Datadog to expand its market share, which should have a positive effect on both the company's financial results and stock price.

Reason 2. New acquisitions and products, entering new markets

On 3 November, Datadog announced the takeover of Cloudcraft, a visualisation service for cloud and systems architects that enables the creation of real-time diagrams of cloud infrastructures. Such a toolkit is highly relevant as users move to the cloud, as it allows them to intelligently model their infrastructure and further reduce the need to update documentation by automatically updating the diagram.

On 19 October, the company unveiled some good news:

Datsadog has achieved PCI (Payment Card Industry) compliance for its Log Management and Application Performance Management products. Achieving these standards will enable the company to work with more organisations involved with credit, debit and other card data. This means we can expect Datadog's customer base and financial results to expand.

The launch of Cloud Security Management, which integrates the functionality of several applications into a single platform, enabling the company to respond more quickly to new threats.

Datadog Continuous Testing is a product designed to help create, manage and run end-to-end tests for web applications. In a rapidly changing macroeconomic environment, businesses often need to adapt quickly and speeding up the testing process is just what you need.

The launch of Cloud Cost Management is a solution for monitoring an organisation's cloud costs. In the context of customer migration to cloud spaces, the solution will, in our view, be popular, as in the initial stages the task of monitoring resources and analysing the rationality of their use is quite time-consuming.

Separately, after the launches described above, Datadog still has 11 more products in beta test (illustration below). We expect them to contribute to improved financial results after the full release.

Reason 3. Investing in research and improving the customer experience

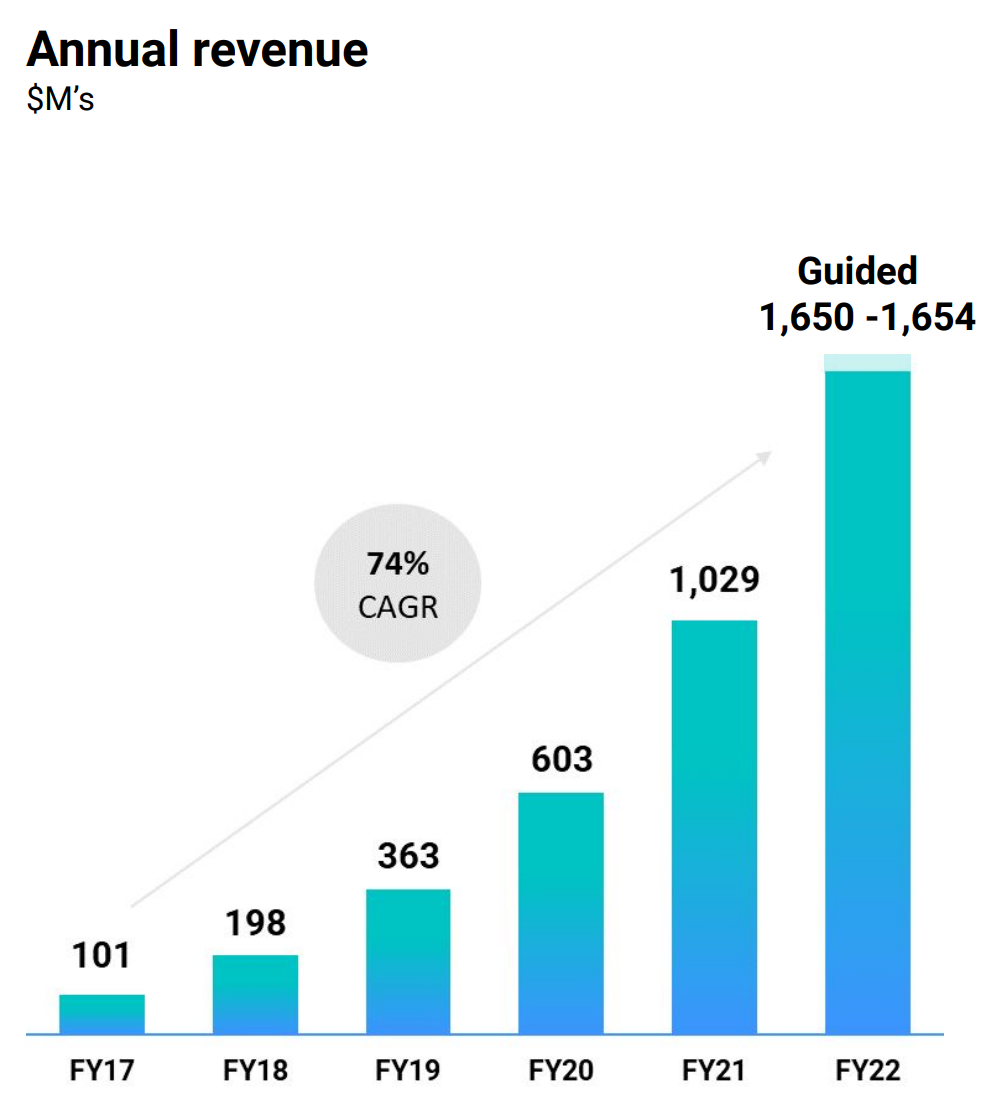

Datadog is focusing on investment in research — its volume has been growing for the past five years (first graph below), and 2022 is no exception.

Greater investment in research increases the company's chances of creating an innovative product that can help expand market share.

In addition to this, the company's efficient customer service is also helping to grow revenues: the proportion of customers using more than two, four and six products simultaneously has been growing steadily since 2018.

At the end of Q3 2022, 80% of the company's customers were using more than two products, 40% were using more than four products, and 16% were using more than six products. The growth in these figures indicates that Datadog has been successful in cross-selling, which is an important quality. We expect that further product launches by the company will contribute to the continued growth of these figures.

Financial indicators

The company's results for the last 12 months:

TTM revenue: up from $880.1 million to $1531.9 million

TTM operating profit: up from -$36.5 million to -$15.6 million:

in terms of operating margins, increase from -4.1% to -1.0% due to a decrease in SG&A expenses from 40.2% to 36.7%

TTM net profit: up from $-44.1 million to $-14 million

in terms of net margin, up from -5% to -0.9%

Operating cash flow: increase from $194.6 million to $419.8 million mainly due to improvement in non-cash items

Free cash flow: up from $160.5 million to $363.9 million

Based on the results of the most recent reporting period:

Revenue: up from $270.5 million to $436.5 million

Operating profit: down from -$4.9 million to -$31.3 million:

in terms of operating margins, down from -1.8% to -7.2%, mainly due to an increase in SG&A expenses from 156.6% to 180.2% due to expansion of the sales force and infrastructure costs

Net income: down from $-5.5 million to $-26 million

in terms of net margin, down from -2% to -6%

Operating cash flow: up from $67.4 million to $83.6 million

Free cash flow: up from $57.1 million to $67.1 million

Datadog has delivered an excellent performance over the past 12 months, given the high base and negative market sentiment in 2022. In our view, the decline in profitability in Q3 is temporary and the increase in sales force costs will be recouped by a further increase in the number of products used by customers.

Cash and liquid assets: $1.77 billion

Net debt: -$1.03 billion

Negative net debt allows Datadog to feel confident during the transition from loss-making to profitable business, leaving room for investment in research and company growth.

Evaluation

In terms of trading multiples, Datadog trades above its competitors except for EV/EBITDA and P/CF.

The company's expensive multiples are linked to its growth rate (as shown in the illustration below, the average annual revenue growth rate since 2017 is 74%) and significant growth potential due to good positioning relative to market trends.

For the year, management expects revenues of $1.65 billion, non-GAAP operating income of $300-$304 million, and non-GAAP EPS in the range of $0.90-$0.92. In our view, the projections are quite realistic and already take into account the temporary margin squeeze that appeared earlier.

Ratings of other investment houses

The minimum price target set by Macquarie is $85 per share. Sanford C. Bernstein, in turn, set a target price of $172 per share. According to the consensus, the fair value of the stock is $118 per share, which implies a 51% upside potential.

Key risks

- Significant investment in R&D could weaken a company's financial stability in the event of a recession.

- Expensive valuation by multiples implies greater volatility in case of negative events (e.g. cybersecurity incidents).

- Against the backdrop of a potential recession, the company may lower its forecasts for next year, which could eventually lead to a significant sell-off in the company's stock.