- Entry Price - 100

- Target price - 138.00

- Potential - 38

- Dividends - 2%

- Risk - High

- Horizon - 9 of month

What's the idea?

- Crocs has come a long way from being a niche watersports shoe retailer to becoming a household name of iconic clogs.

- High brand awareness provides the firm with a significant competitive advantage in the form of price power.

- While Crocs has exhausted its low base effect, we believe the firm still has room to further expand its core brand.

- The HEYDUDE brand accounts for about a quarter of Crocs’ total revenue and is also an important growth driver capable of extending the company's runway.

- Crocs has double-digit revenue growth, high margins, and solid cash flow.

- Despite the better financials compared to peers, Crocs trades at a discount to the industry average.

About Company

Crocs (CROX) manufactures and sells footwear and lifestyle accessories for men, women, and children worldwide. The company has become widely known for its clogs and today offers a variety of shoes, including sandals, wedges, boots, and slippers. Following the takeover of HEYDUDE in December 2021, the firm further expanded its product portfolio. Crocs was founded in 2002 and is headquartered in Broomfield, Colorado.

Reason 1. Company evolution

Crocs was founded as a manufacturer of unique yachting footwear. In 2002, the company introduced its first model at the Florida Boat Show, and all pairs produced were quickly sold out, demonstrating the strong demand for soft clogs that would not sink in the water. However, the niche nature of boat footwear severely limited the company's target market. Within a few years, Crocs had exhausted its growth potential. Amid the financial crisis in 2008, the firm lost $185 million and was forced to cut 2,000 jobs.

Initial attempts to overcome the brand's niche nature and enter the mass market were met with muted consumer response, with some fashion influencers calling clogs "ugly." However, in the following years, Crocs has done significant work on its positioning. The company has rethought the brand and adopted a new marketing strategy that involves product premiumization and active cooperation with famous fashion houses. As a result, Crocs’ clogs have become a household name, putting the company on par with brands such as Converse, Ugg, and Dr. Martens.

In recent years, Crocs shoes have been advertised by such celebrities as Kendall Jenner, Nicki Minaj, Justin Bieber, Madonna, and Victoria Beckham. Crocs has collaborated on several collections with Balenciaga and with renowned designer Salehe Bembury, attracting the attention of haute couture aficionados, and solidified its position in the mass market with collaborations with companies such as Taco Bell, 7-Eleven, and KFC. Fashion magazine Vogue has taught readers how to wear famous clogs, while TIME magazine has listed Crocs among the 100 most influential companies in 2023.

According to a semi-annual survey conducted by Piper Sandler, Crocs was ranked 6th in the preferred shoe brands among millennials, up from the 8th position last year. High brand awareness provides the firm with a significant competitive advantage in the form of price power. In the last quarter, the company increased the average price of Crocs shoes by 12.8%, which is well above inflation.

Reason 2. Core brand potential

About 75% of the company's consolidated revenue comes from its core brand, Crocs, which had been its only brand until 2022. With soft and comfortable clogs, Crocs was one of the beneficiaries of the COVID-19 pandemic. From 2019 to 2022, the number of pairs of clogs sold increased by 72% from 67.1 million to 115.6 million, while the brand's revenue increased by 116% from $1.23 billion to $2.66 billion.

Crocs brand revenue, and pair sold; source: compiled by author

While Crocs has exhausted its low base effect, we believe the firm still has room to further expand its core brand. We identify several drivers that can ensure the growth of the main brand in the coming years:

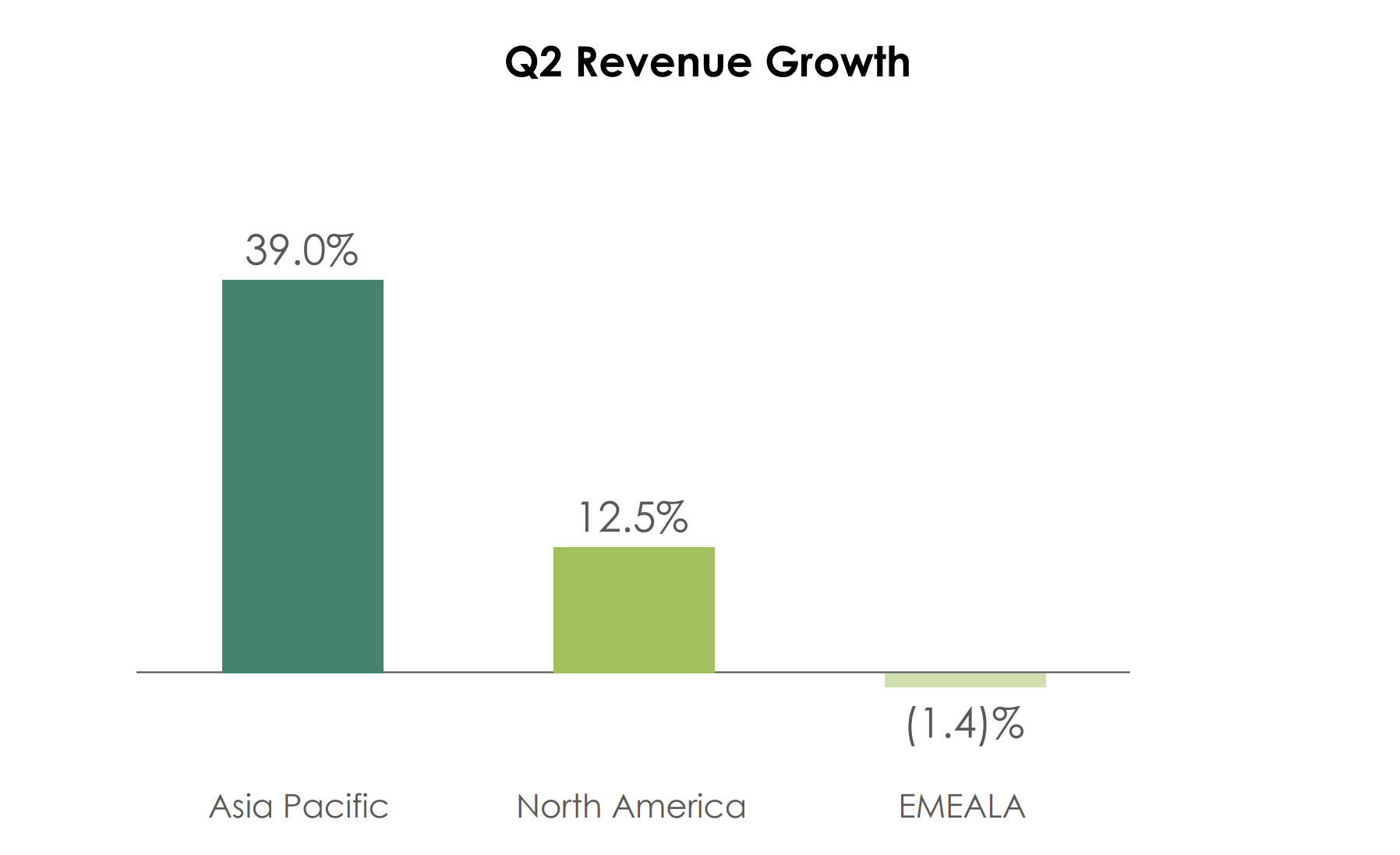

Expansion in Asian markets. Asia is an important long-term growth driver for the Crocs brand, as brand penetration in the region is currently significantly lower than in the US. In Q2, sales in Asia rose 39% in constant currency. Growth was observed in all key region markets, including China, Australia, South Korea, and Southeast Asia. In the most promising market, China, the brand's revenue grew by more than 100%, exceeding the company's expectations.

Crocs brand revenue dynamics by regions

Growth in digital sales. In Q2, Crocs’ digital sales grew 17% year-on-year and e-commerce penetration was 38%, which, while above the industry average, is still lower than Nike's and in line with VF Corp.’s and Macy's. We believe Crocs can achieve a higher proportion of online sales as clogs are easier to buy online than sneakers, boots, and clothing. Clogs are easier to size due to their spacious shape and soft material.

Dynamics and share of digital revenue

The sandal segment development. As a promising avenue for brand expansion, sandals have long been a focus of Crocs' attention. The sandal market presents a significant opportunity because it is large and highly fragmented. Crocs' management estimates the sandal’s volume at $30 billion versus $8 billion for the clog market. Sandal sales were around $310 million in 2022 and are expected to reach $400 million in 2023. It is worth noting that in Q2 2023 sandals were the most dynamic segment within the Crocs brand, with a 34% year-on-year growth.

Revenue dynamics by segments within the Crocs brand

Reason 3. HEYDUDE potential

The acquisition of HEYDUDE, closed in February 2022, cost Crocs a total of approximately $2.3 billion and was negatively perceived by the market. However, today HEYDUDE provides about a quarter of the firm's total revenue and is also an important growth driver capable of extending the company's runway.

HEYDUDE is one of the fastest-growing casual footwear brands in the US market. According to WanderLuxe World, the brand's revenue grew 15 times from 2017 to 2019. After the deal was closed, Crocs’ management provided a forecast according to which HEYDUDE's revenue should reach $1 billion in 2024. However, the target is likely to be achieved already this year as the brand generated revenue of $986 million on a pro forma basis in 2022 and is expected to increase it by 3.5%–7.5% in 2023.

HEYDUDE revenue

Crocs has already done significant work on HEYDUDE’s brand recognition. Last quarter, in the aforementioned Piper Sandler survey, HEYDUDE ranked 8th in the list of preferred shoe brands among millennials. In our opinion, due to its non-standard and original character, the brand can get wide coverage. HEYDUDE has the following main growth drivers:

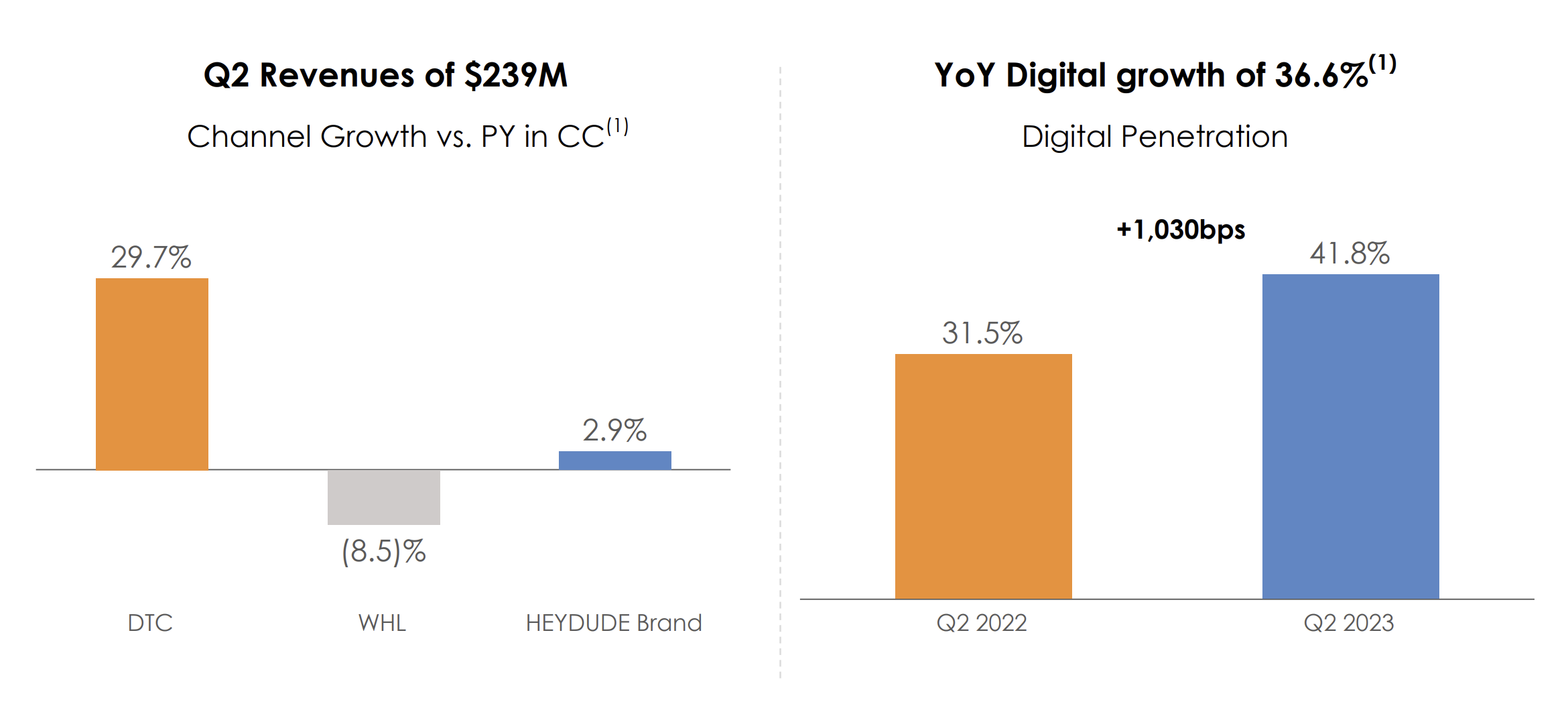

Growth of direct-to-customer (DTC) sales. Unlike the Crocs brand, half of whose revenue comes from direct sales, HEYDUDE earns primarily through wholesale supplies, which account for 36% of the brand's revenue. At the same time, HEYDUDE’s DTC sales are growing much faster than wholesales. Thus, in Q2, DTC sales grew by 29.7% yea-on-year, while wholesales decreased by 8.5%. It is worth noting that HEYDUDE's e-commerce penetration rate exceeds that of Crocs at 41.8%.

HEYDUDE revenue by channel, and e-commerce penetration

International expansion. While Crocs has begun testing the brand in international markets including the UK, Germany, and the Netherlands, HEYDUDE remains a local brand. The international market accounts for only about 6% of its revenue. In comparison, the Crocs brand earns 40% of its revenue abroad. The low level of HEYDUDE's presence in international markets suggests significant room for brand expansion.

It is worth noting that in Q2, the company lowered its HEYDUDE revenue forecasts for Q3 and FY2023, noting weakness in the wholesale channel. Management noted that wholesale partners have become more careful in managing their inventories amid deteriorating macroeconomic conditions. The company began to reduce stocks, thereby limiting future supply. By the end of 2023, HEYDUDE sales are expected to grow by 3.5%–7.5% year-on-year, while the previous forecast assumed growth of about 15%.

Financial performance

Crocs’ financial performance in the trailing 12 months (TTM) can be summarized as follows:

- Revenue amounted to $3.89 billion, up 9.3% from 2022. The highest growth rate of 14.2% was demonstrated by the HEYDUDE brand, while the Crocs brand grew by 7.8%.

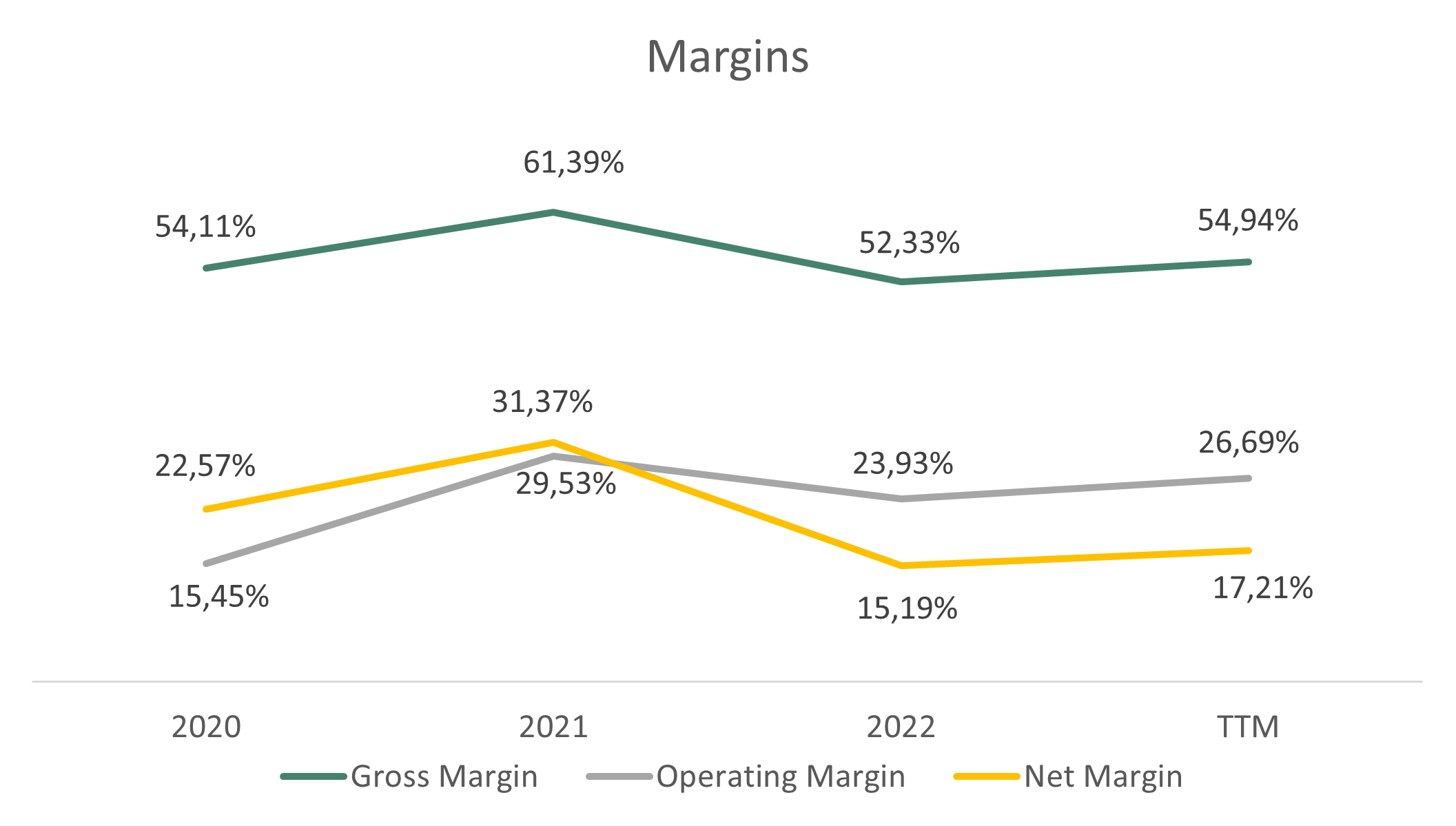

- Gross profit increased from $1.86 billion to $2.14 billion. Gross margin rose from 52.33% to 54.94%.

- Operating profit increased from $850.8 million to $1.04 billion, driven by higher revenue and improved operating leverage. Operating margin rose from 23.93% to 26.69%.

- Net income amounted to $669.0 million against $540.2 million at the end of the year. Net margin increased from 15.19% to 17.21%.

Dynamics of the company's financial results

Company margin dynamics

Crocs’ financial performance in Q2 FY 2023 are presented below:

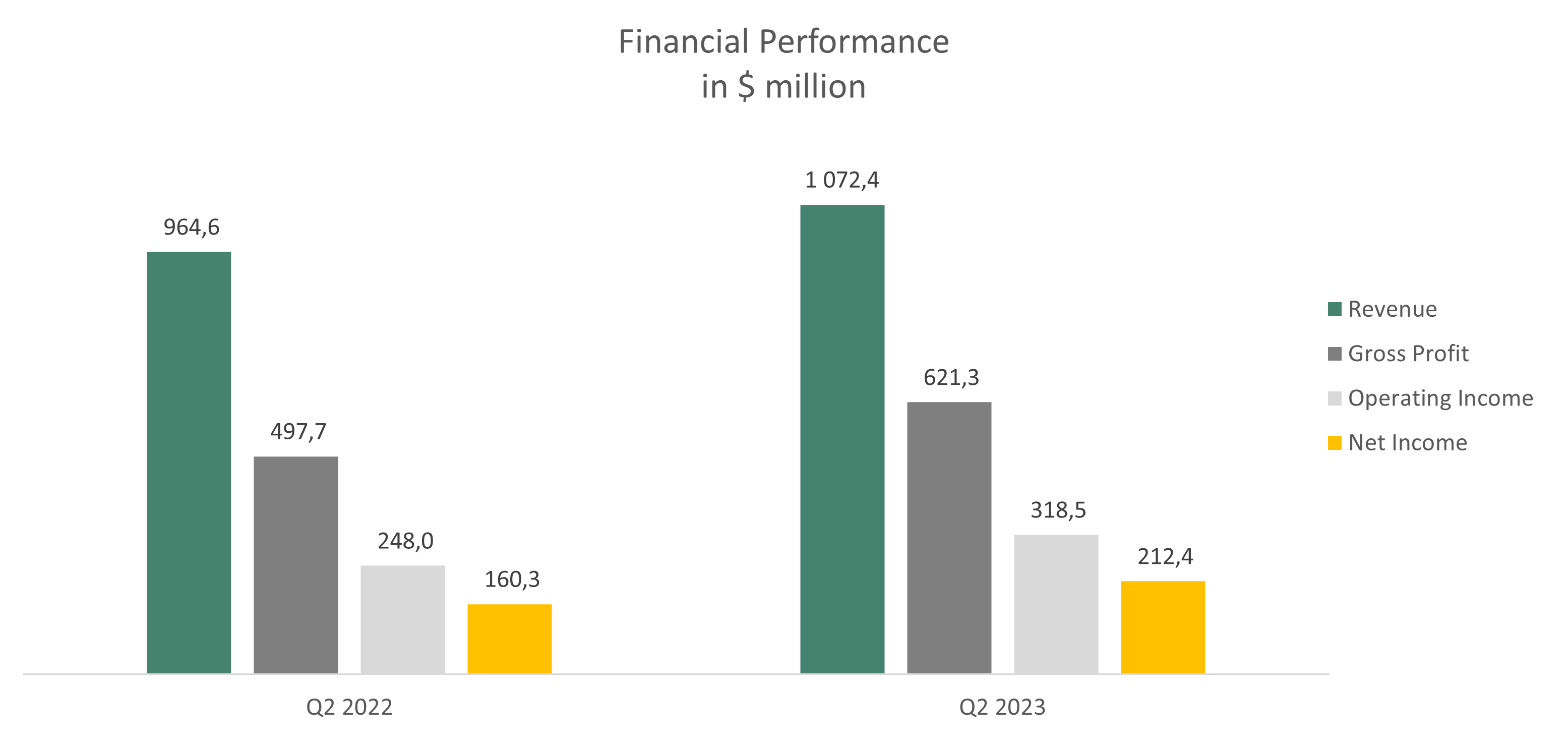

- Revenue grew by 26.1% YoY: from $964.6 million to $1.07 billion. The core brand showed the best growth rate of 13.8%, while HEYDUDE’s revenue grew by only 3% due to headwinds in the wholesale channel.

- Gross profit increased from $497.7 million to $621.3 million. Gross margin rose from 51.60% to 57.94%.

- Operating income was $318.5 million versus $248.0 million a year earlier. Operating margin increased from 25.71% to 29.70%.

- Net income amounted to $212.4 million versus $160.3 million a year earlier. Net margin increased from 16.62% to 19.81%.

Dynamics of the company's financial results

As noted earlier, at the end of the last reporting period, Crocs’ management lowered its HEYDUDE revenue forecast, causing a significant drop in the stock value. At the same time, the company improved its guidance for its main Crocs brand to 12%–13% (against 7%–9% earlier) and raised its expectations for margins and earnings per share.

Management guidance for 2023

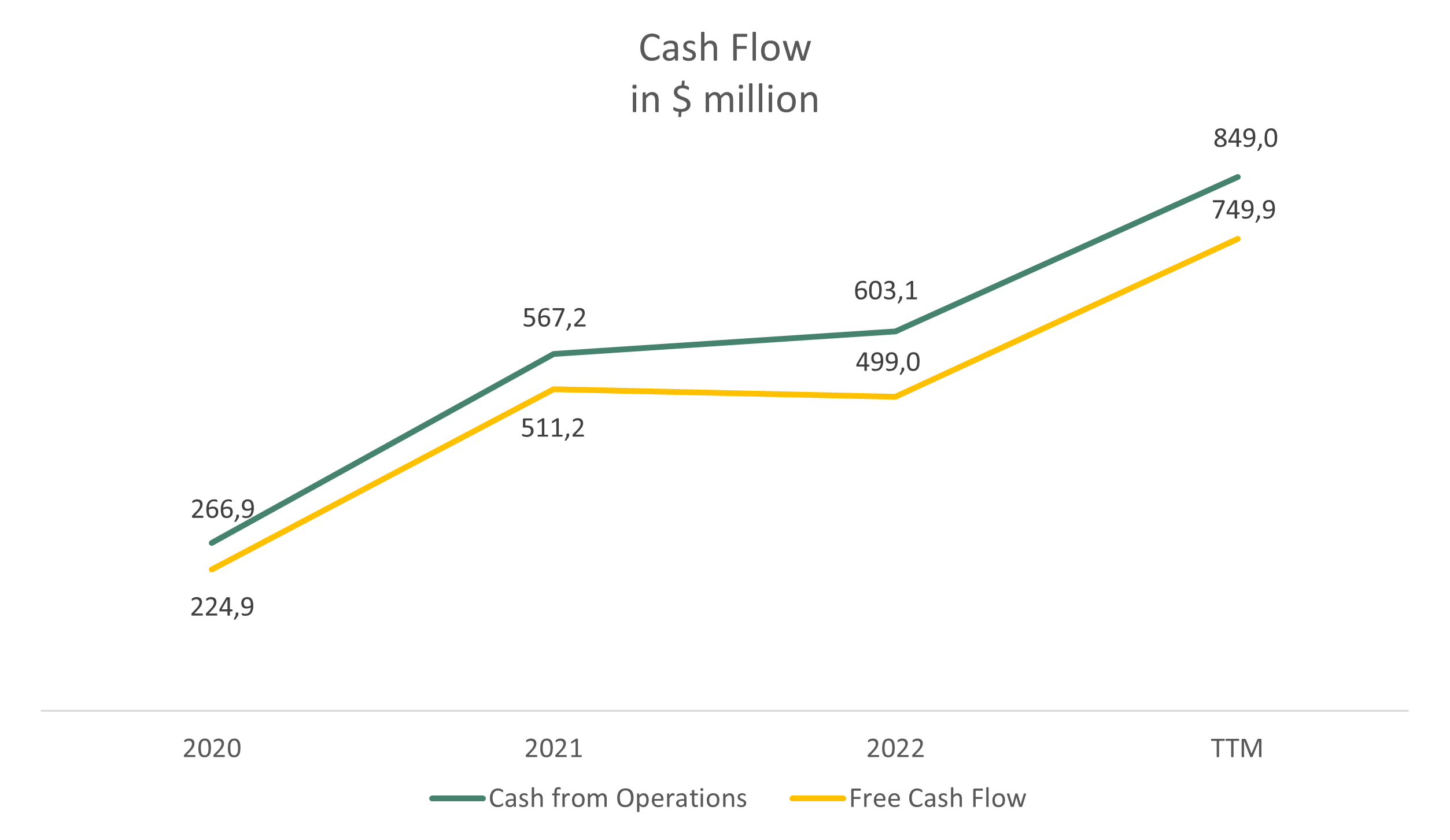

Crocs has been showing an impressive cash flow conversion. TTM cash from operations was $849.0 million versus $603.1 million for the year. Free cash flow for the same period increased from $499.0 million to $749.9 million. The positive dynamics were due to an increase in net income, a decrease in net working capital, and a reduction in capital expenditures.

Company’s cash flow

Crocs has a healthy balance sheet with total debt of $2.03 billion, cash equivalents and short-term investments of $166.2 million, and net debt of $1.86 billion, 1.71x EBITDA over the trailing 12 months (Net Debt/EBITDA of 1.71x).

Stock valuation

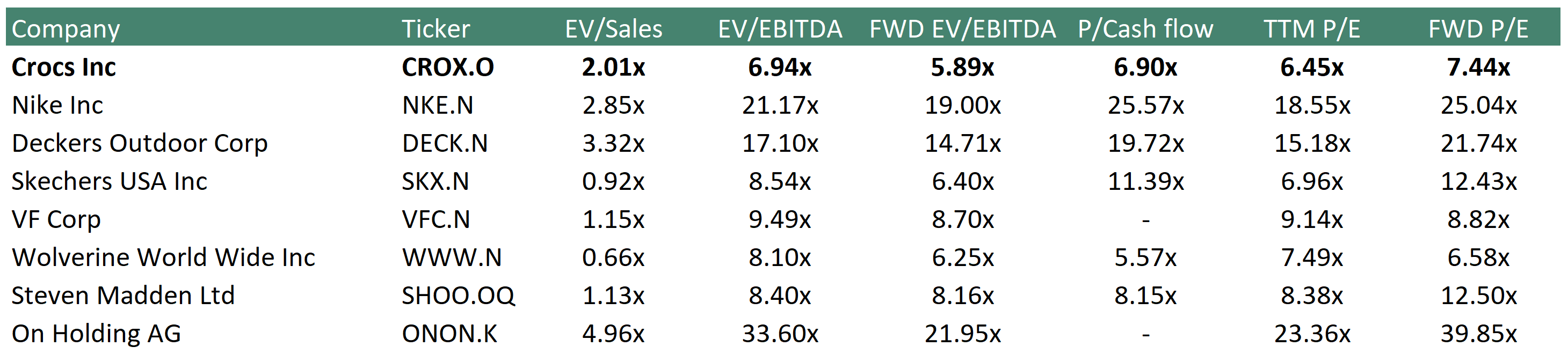

Despite its double-digit growth, high margins, solid cash flow, and a healthy balance sheet, Crocs trades at a discount to the industry average on the following multiples: EV/EBITDA — 6.94x, FWD EV/EBITDA — 5.89x, P/Cash flow — 6.90x, P/E — 6.45x, FWD P/E — 7.44x.

Comparable valuation

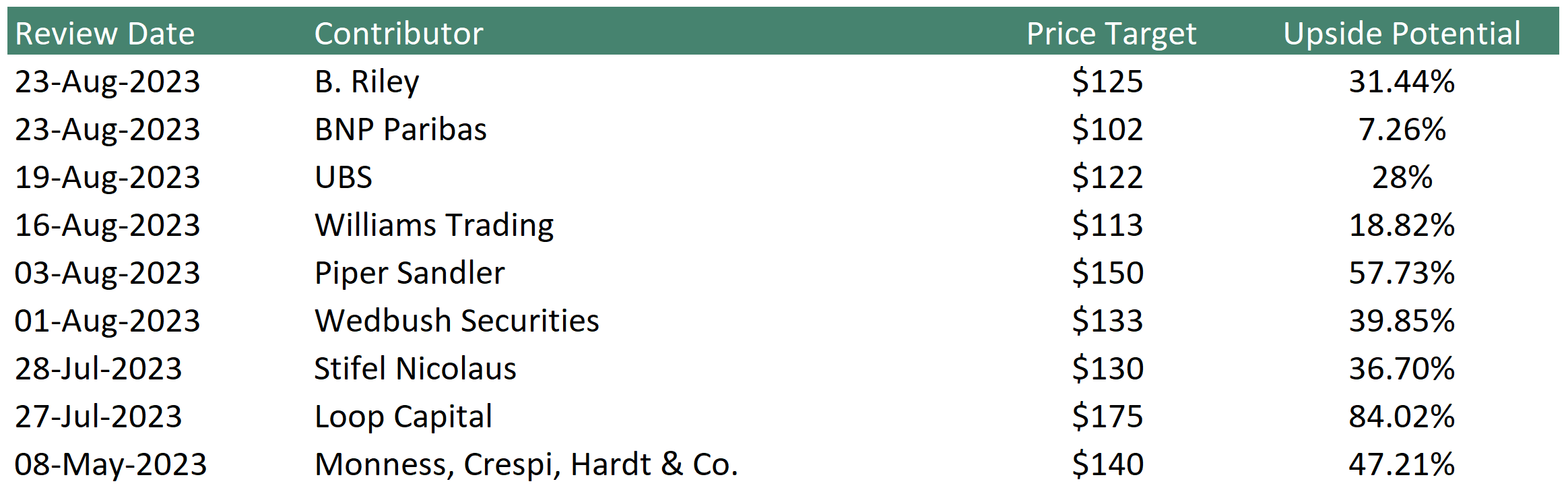

The minimum price target from investment banks set by BNP Paribas is $102 per share. Meanwhile, Loop Capital estimates CROX at $175 per share. According to the Wall Street consensus, the stock’s fair market value is $138, implying a 44.1% upside potential.

Price targets of investment banks

Key risks

- Given that Crocs' main product, clogs, has an unusual appearance, it is possible that the company's impressive growth is due to temporary fashion trends and is not of sustainable character. If Crocs fails to remain relevant to consumers, the company could lose its foothold in the footwear market.

- Companies in the consumer discretionary sector are highly susceptible to economic cycles. The possible deterioration of the macroeconomic environment could damage Crocs' financial performance, which would affect the company’s market value.

- The slowdown in the HEYDUDE revenue growth seen in the recent quarters had been unexpected by the company’s management. The slowdown may indicate that the company has overestimated the acquired brand's prospects and its value. In this case, Crocs may have to write off some of its intangible assets, which would affect the company’s profit.