What's the idea?

- Chegg operates in a large and growing educational technology market. Digital spending is expected to exceed 5% of total education spending.

- The focus on academic programs allows Chegg to significantly expand the LTV (Lifetime value) of its subscriber base.

- Prudent strategic management and targeted acquisitions have allowed the company to expand its range of services and significantly deepen its competitive moat.

- Chegg is able to increase the stock value by almost a quarter through the current share buyback program.

- Chegg is one of the few companies in the education technology industry with a steady and growing cash flow.

- According to the Wall Street consensus, the stock has an upside potential of 58.17%.

- The company will release its 2022 financial results on Monday, February 6. Given the mixed results of some tech companies, it's hard to provide a prediction for Chegg’s report. There is a possibility of increased volatility in the company's stock. We consider it appropriate to hedge the position by buying PUT options (strike 15, expiration date 02/17/2023). After the release, the options can be sold.

About Company

Chegg (CHGG) operates an online learning platform that helps students with their academic studies. The company operates in two segments: under Chegg Services it provides subscription services that can be accessed through websites and mobile devices; while the Required Materials segment provides students with printed and electronic textbooks. Chegg was founded in 2005 and is headquartered in Santa Clara, California.

Why do we like Chegg Inc?

Reason 1. Target market potential

According to GlobalData, the education technology market was valued at $183.4 billion in 2021 and is expected to grow at a compound annual rate of 16.0% through 2026 to reach $410.2 billion at the end of the forecast period. The high growth rate is due to the rapid digitalization in education, as well as the widespread use of learning through digital platforms.

Over the next five years, spending on digital technologies is expected to exceed 5% of total education spending. This is due to government initiatives to provide funds and grants for the introduction of smart learning systems, which will also drive the growth of the EdTech market during the forecast period.

Expected dynamics of the educational technologies market

North America, a key market for Chegg, will contribute approximately 46% of future growth. In addition, the Post-Secondary education segment is the second-largest after the Secondary education segment (K-12), with a market share ranging from 20% to 25%, according to various estimates. Thus, the size of the target market is expected to reach about $82 billion by 2026. In other words, the expected market dynamics provide significant opportunities for Chegg.

The firm's management estimates the global academic market at 100 million English-speaking students worldwide. Chegg Services currently has 7.8 million subscribers, which suggests a relatively high penetration level. However, the company’s management expects to expand its capabilities by launching tools in foreign languages. In the last quarter, the company launched a beta version of its app in Spanish.

Large global academic market opportunity

Reason 2. Competitive positioning

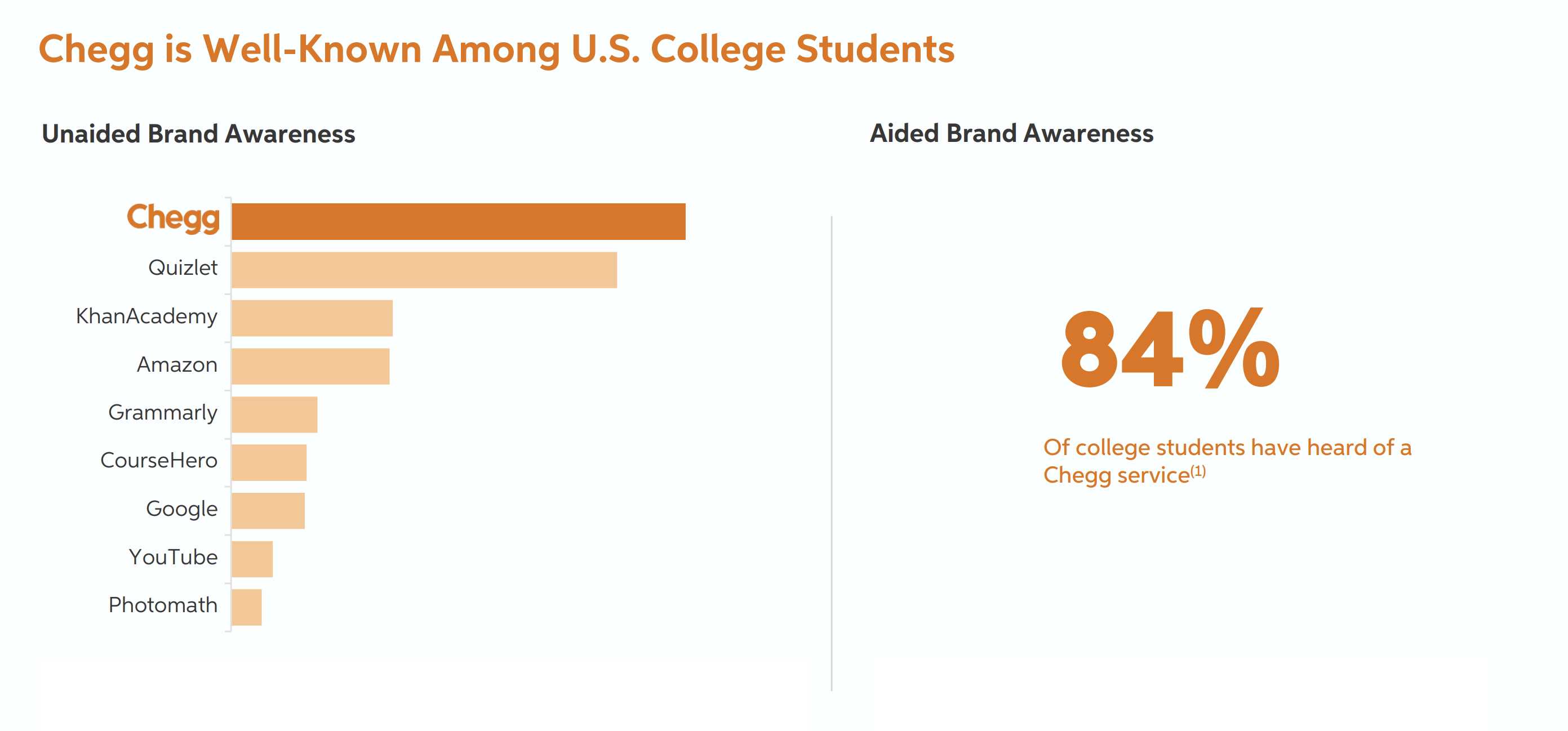

The ability to benefit from market conditions depends largely on a company's competitive positioning. Chegg's major strengths include its focus on academic programs, while most competitors offer solutions for continuing education or advanced training. According to the company, Chegg is one of the most recognized brands among college students in the US.

Chegg awareness among US college students

While platforms like Coursera primarily make money helping people who want to improve their skills and competencies, Chegg attracts students who need textbooks and homework guides. Given that academic programs last for several years, Chegg's customer base is more stable, and its subscriber LTV is higher than that of competitors (LTV represents the accumulated profit that a company can receive from a loyal customer in the long run). It is worth noting that from 2016 to 2021, Chegg grew its subscriber base at a compound annual rate of 39%.

Chegg Services subscribers

Until recently, Chegg was a simple website with access to textbook task solutions. Prudent strategic management and targeted acquisitions have allowed the company to expand its range of services and significantly deepen its competitive moat. In addition to academic programs such as Chegg Study, Chegg Writing, and Chegg Math, the company offers an online course platform, Thinkful, acquired in 2019. In 2002, Chegg closed its takeover of Busuu, thereby entering the growing foreign language learning market.

Services offered

It is likely that Chegg will continue to strengthen its competitive position through M&A deals. The company generates solid cash flow and has a fairly liquid balance sheet, with cash equivalents and short-term investments accounting for 39.2% of total assets. The company’s management has already signaled possible new acquisitions, while the current macroeconomic environment allows it to conclude the deals on the most favorable terms.

Reason 3. Exemplary capital allocation

Chegg is exemplary in terms of capital allocation. In Q3, the company's net income was $252 million, exceeding revenue of $165 million. The anomalous profit was largely due to the fact that Chegg has bought back its own bonds with a par value of $500 million maturing in 2026 for $400 million. These bonds were traded at a significant discount to face value and, thus, provided the company's shareholders with a risk-free return. As a result of the transaction, Chegg received $94 million in other income.

In June 2022, shortly after the $1 billion share buyback program was nearly completed, the firm announced it would increase the program by another $1 billion. Under the current buyback program, $642.6 million is still available, representing approximately 24% of the company's market capitalization. Thus, Chegg is able to increase its stock value by almost a quarter just through the redistribution of capital.

Financial performance

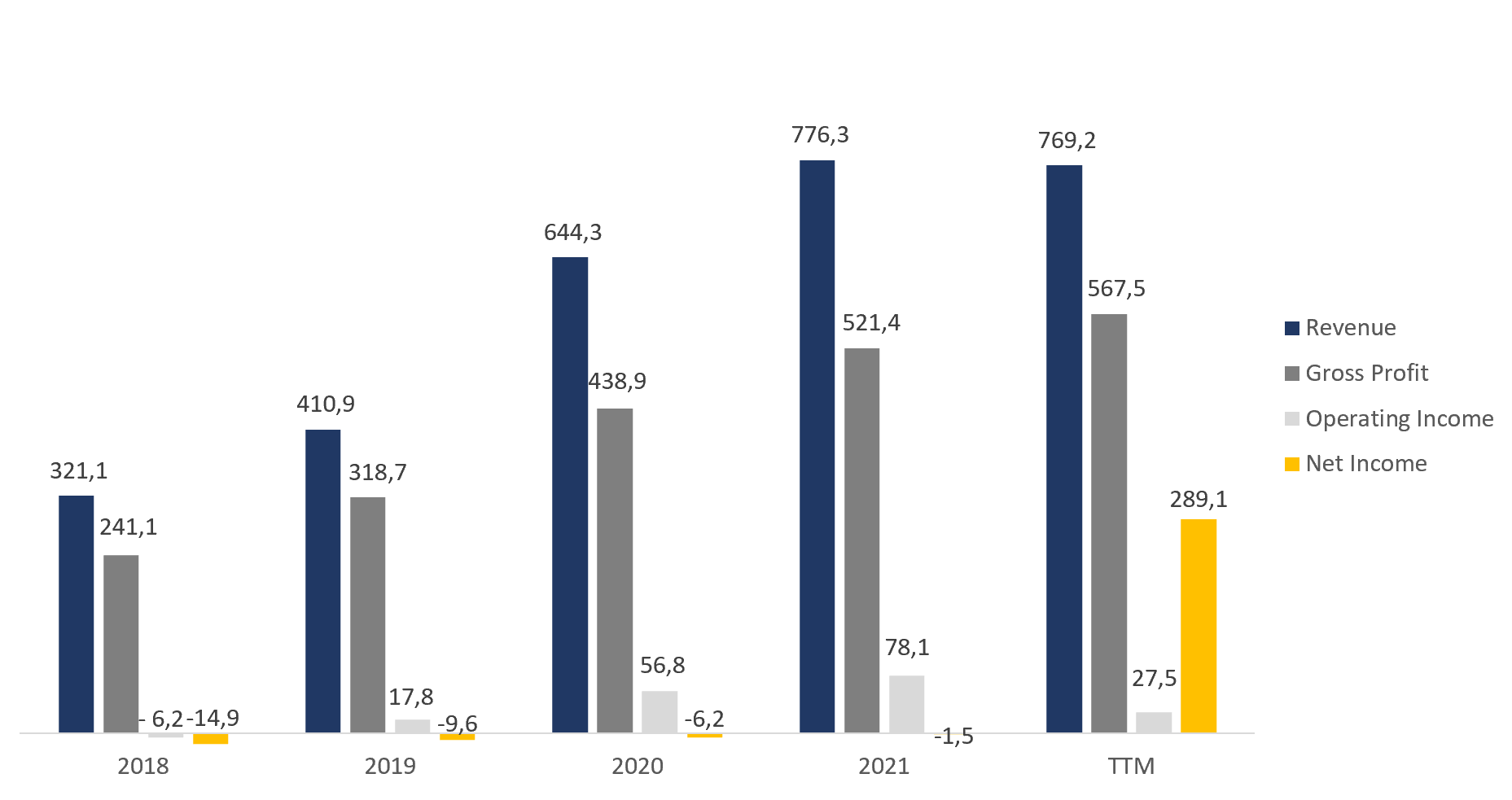

The company's results for the last 12 months can be summarized as follows:

- Over the trailing 12 months (TTM), revenue stood at $769.2 million, a decrease of 0.9% over 2021.

- Gross profit increased from $521.4 million to $567.5 million. Gross margin rose from 67.16% to 73.78%.

- Operating income decreased from $78.1 million to $27.5 million. Operating margin was 3.57% compared to 10.06% for the year.

- Net income stood at $289.1 million compared to -$1.5 million at the end of the year. Net margin increased from -0.19% to 37.58%, which is driven by other income from the bond repurchase in Q3 2022.

Dynamics of the company's financial results

Company margin dynamics

The decrease in revenue that has been observed in recent quarters is due to the abnormal growth of the indicator in 2021 and, as a result, the high base effect. However, the company retained most of the newly attracted users.

At first glance, Chegg does not seem to be operating efficiently and shows low profitability. However, the company's operating margin has always been affected by massive stock compensation. Thus, in the first nine months of 2022, compensation increased by 29.1% YoY and reached 23.3% of total operating expenses.

Share of stock compensation in total operating expenses

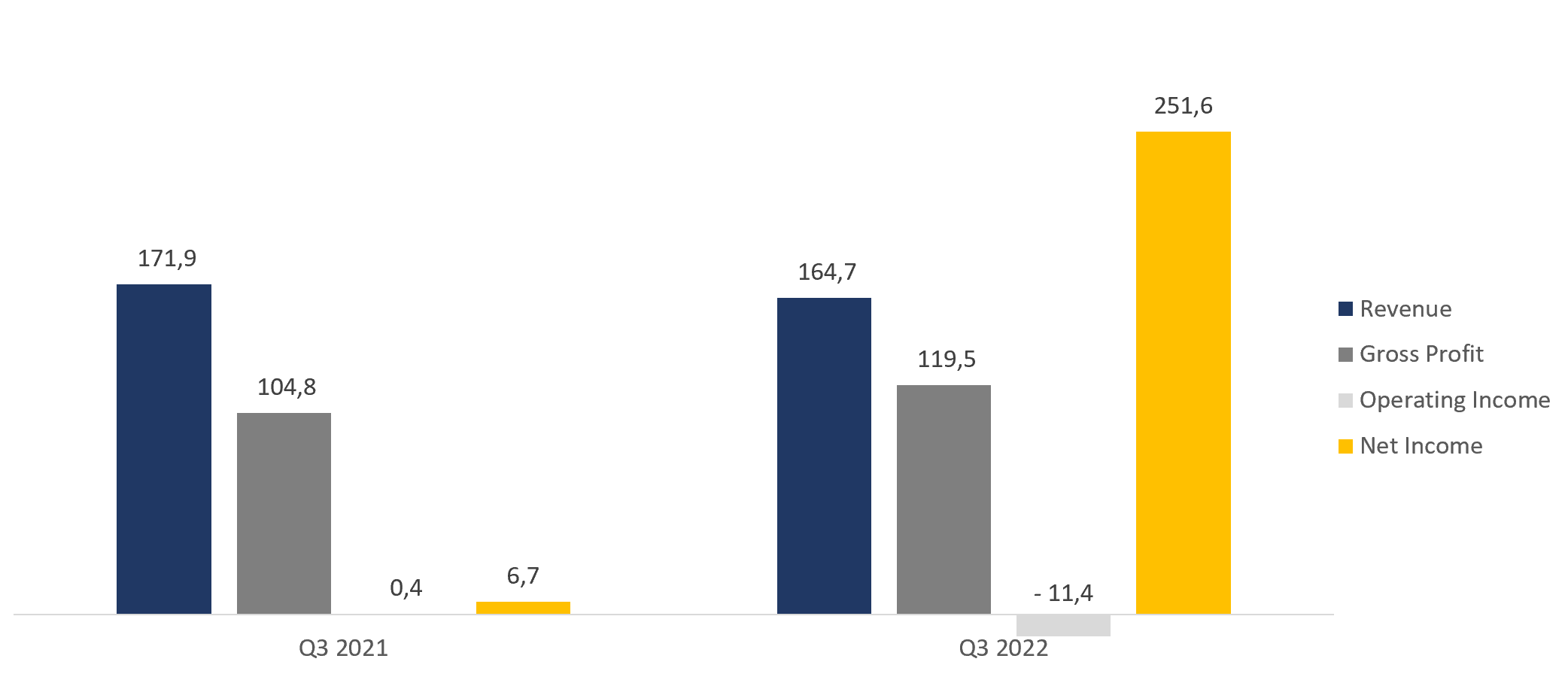

The company’s Q3 2022 financial results are as follows:

- Revenue decreased by 4.2% YoY, from $171.9 million to $164.7 million.

- Gross profit rose 14.0% YoY: from $104.8 million to $119.5 million. Gross margin was 72.56% compared to 60.97% last year.

- Operating income stood at -$11.4 million compared to $0.4 million a year earlier. Operating margin decreased from 0.21% to -6.94%.

- Net income was $251.6 million compared to $6.7 million a year earlier. Net margin was 152.70% compared to 3.87% last year.

Trends in the company's financial results

In terms of efficiency, in this case, the most representative indicator is cash flow. Cash from operations (TTM) amounted to $246.8 million in the latest reporting period, compared to $273.2 million for the full year. Free cash flow decreased from $168.1 million to $136.4 million. The decline was driven by a loss on early redemption of debt (which offsets other income from the repurchase of the notes) and a tax benefit related to the release of valuation allowance.

Company cash flow

The company has a healthy balance with total debt of $1.2 billion, cash equivalents and short-term investments of $940.8 million, and net debt of $246.8 million, which is equivalent to Net Debt/EBITDA of 2.20x.

Evaluation

Chegg trades at a premium by EV/Sales multiple, however, it is one of only two companies in the industry (along with Stride) with positive margins and cash flow. The firm trades at a discount to Stride by earnings multiples of EV/Sales — 3.74x, EV/EBITDA — 22.02x, P/Cash flow — 16.50x, P/E — 10.63x, FWD P/E — 15.61x.

Comparable valuation

The minimum price target set by BNP Paribas is $18 per share. In turn, Northland Securities values CHGG at $35 per share. By consensus, the stock’s fair market value is estimated at $29.5 per share, which implies a 38.17% upside potential.

Price targets of investment banks

Key risks

- The company will release its 2022 financial results on Monday, February 6. Given the mixed results of some tech companies, it's hard to provide a prediction for Chegg’s report. There is a possibility of increased volatility in the company's stock. We consider it appropriate to hedge the position by buying PUT options (strike 15, expiration date 02/17/2023). After the release, the options can be sold.

- Although Chegg more than covers its stock compensations with massive buybacks, large compensations may dilute equity and burn shareholder value.

- If Chegg fails to retain subscribers acquired during the pandemic, the company's financials could continue to decline, impacting its share price.