What's the idea?

- The alternative investment industry is expected to grow at a double-digit rate in the coming years. Carlyle is one of the largest private equity fund managers.

- Private equity funds do not imply the possibility of withdrawal of assets by investors. Carlyle does not risk a sharp reduction in assets under management and a fall in management fees.

- The rich background of Carlyle's co-founders makes it possible to run the company successfully until a permanent CEO is found.

- If the challenging macroeconomic environment becomes sustained, Carlyle's stock price will be supported by dividend payments.

- The company is trading at a discount to the industry average. According to Wall Street consensus, the upside potential is more than 50%.

About Company

The Carlyle Group Inc. (CG.US) is one of the largest private equity (PE) fund managers. The company operates in three segments: Global Private Equity, Global Credit and Global Investment Solutions. The Carlyle Group was founded in 1987 and is headquartered in Washington, DC.

Why do we like The Carlyle Group LP?

Reason 1. Industry opportunity

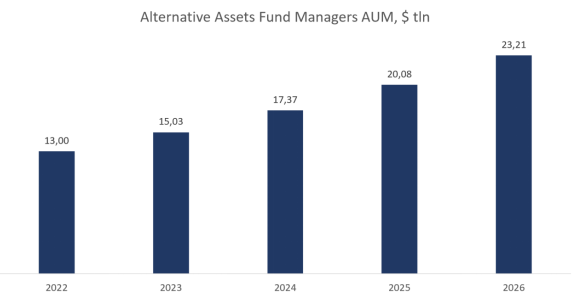

According to Preqin's 2022 Global Alternatives study, asset under management (AUM) of alternative asset managers today stands at $13 trillion. AUM is expected to grow at a compound annual growth rate (CAGR) of 15.4% to reach $23.2 trillion by 2026. Private equity and venture capital (PEVC) is the largest asset class: these AUMs are estimated to exceed $11 trillion by 2026, accounting for almost half of all assets under management (49%).

AUM of alternative asset managers

According to Preqin's November 2021 survey of more than 300 investors, the majority of institutional players are still investing in alternative assets. 86% of investors said performance met or exceeded their expectations in 2021. And while they are wary of rising interest rates, 51% of respondents expect to invest the same amount in alternative assets in the future, while 32% said they plan to increase their investments. As respondents were institutional players with a strong focus on planning and bureaucratic procedures, it is unlikely that they will change allocation of investment portfolios, even though the macroeconomic environment is deteriorating.

The Carlyle Group has $369 billion in assets under management and its main competitors are:

- Blackstone (AUM — $951 billion)

- Apollo Global Management (AUM — $523 billion)

- KKR & Co. (AUM — $496 billion)

- CVC Capital Partners (AUM — $131 billion)

- Thoma Bravo (AUM — $122 billion)

Although Carlyle is one of the market leaders and the fourth-largest company by assets under management, the gap with Blackstone is a multiple, giving Carlyle room for further growth.

Reason 2. Headwinds are temporary

Carlyle has lost about half of its capitalisation over the past year. The decline is due both to general market factors — tighter monetary policy and reduced appetite for risky assets — and to specific reasons specific to Carlyle Group and other companies in the private equity industry. These reasons include:

- Reduced financial results

- Lack of a permanent general director

- Slowdown in fundraising

For the first nine months of 2022, the company's revenue fell 45.2% year-on-year due to a multiple of lower performance allocations. The decline was driven by significant exposure to private equity — the Global Private Equity segment accounted for 73.4% of total revenue, while Global Credit accounted for 17.7% and Global Investment Solutions 8.8%.

After Kewsong Lee's high-profile sacking as CEO in August this year, Carlyle’s stock lost over a billion dollars of its market value. William Conway, one of Carlyle's founders, has temporarily taken over the company. Due to the lack of a permanent CEO and the difficult macroeconomic environment, Carlyle Group has faced a sharp slowdown in fundraising. While the company raised $10 billion last quarter, the amount has now fallen to $6 billion. As a result, the amount of assets under management fell 2% and the capital available for investment fell 9% to $74 billion.

Volume of assets under management by Carlyle Group

Private equity firms have always been highly volatile, with revenues falling in times of pessimism but recovering just as quickly when the market is bullish. Unlike mutual funds, private equity funds do not imply that investors can withdraw their assets. Most often such funds are set up for 5 to 10 years. Carlyle does not risk a steep decline in AUM and management fees, only the performance fee. So the key question analysts are asking is not "will the financials recover" but "when will they recover".

The absence of a permanent CEO is a reasonable cause for concern, as the CEO largely determines the direction of the company's strategic development. However, in our view, the influence of this factor is very limited, as the company's founders remain its majority shareholders and it is they who determine the vector of Carlyle's development. The wealth of professional experience of William Conway, David Rubenstein and Daniel D'Agnello makes it possible to successfully manage the company until a permanent CEO is found.

Reason 3. Dividend yield

If the challenging macroeconomic environment is sustained, Carlyle's stock price will be supported by dividend payments. Today, the company provides shareholders with a yield of 4.3%, the best among its peers. The company has the ability not only to maintain its current level of payout, but also to increase it.

First, for the first nine months of 2022, Carlyle distributed $325.4 million in dividends, representing just 28.9% of net profits for the period. If the financial performance recovers to last year's level, the payout ratio will be halved.

Secondly, Carlyle has a payment history of more than a decade. The company even paid a dividend in 2020.

History of the company's dividend payments

Financial indicators

Carlyle's financial results for the past 12 months can be summarised as follows

- Carlyle's largest item of revenue is investment income, which is primarily generated by performance fees. It fell 51.6% to $3.25 billion at the end of the most recent reporting period.

- Management fees, the second largest source of income, rose 21% to $2.02 billion.

- Incentive fees rose by 19.7% to $58.4 million and other income by 14.1% to $392 million.

- Total revenue for the last 12 months was $5.72 billion, down 34.9% on 2021. The decline is due to a two-fold reduction in investment income.

- TTM net profit stood at $1.75 billion compared to $2.98 billion at the end of the year. Net margins declined by 3.4 percentage points to 30.52%.

Carlyle Group revenue trends

Carlyle Group net profit and margins

The financial results for Q3 2022 are as follows:

- Investment income was $422 million, compared with $1.14 billion a year earlier.

- Management fees rose 31.5% year on year to $536 million.

- Incentive fees rose 15.3% to $15.1 million and other income rose 37.1% to $115 million.

- Net income was $280.8 million compared to $532.8 million a year earlier. Net margin decreased by 6.7 percentage points to 25.8%.

Carlyle Group revenue trends

Carlyle Group net profit and margins

Operating cash flow for TTM's most recent reporting period was $230 million, compared with $1.79 billion for the year-ago period. The decrease was due to lower net income and an increase in the company's investments in financial assets (in Carlyle's case, investments are considered part of operating activities). Free cash flow per equity declined from $1.75 billion to -$427.7 million. Negative free cash flow is due to the acquisitions of a number of smaller companies, including Abingworth LLP and CLO Management.

Company cash flow

Carlyle has a healthy balance sheet: total debt is $2.24 billion, cash equivalents and short-term investments account for $1.54 billion and net debt is $696 million, which is three times the TTM of operating cash flow — Net Debt/Cash From Operations — 3.02x.

Evaluation

Carlyle today trades at 2019/20 levels, although since then the company's assets under management have risen by more than 60%. The company trades at a discount to the industry average: EV/Sales — 3.17x, P/Cash flow — 5.62x, P/E — 6.13x, P/B — 1.79x.

Comparable estimate

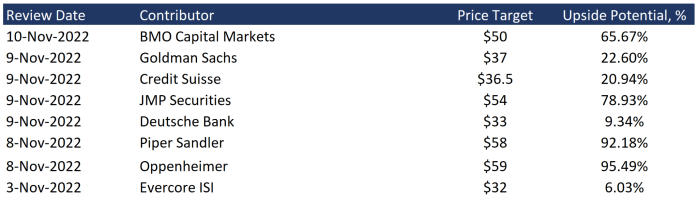

The minimum price target from investment banks set by Evercore is $32 per share. Oppenheimer, on the other hand, values Carlyle at $59 per share. By consensus, the fair market value of the stock is $44.90 per share, suggesting a 53.24% upside.

Price targets of investment banks

Key risks

- The asset management industry is highly sensitive to economic cycles. If the economy plunges into recession, Carlyle could face a further slowdown in fundraising and revenue would fall significantly.

- Carlyle has to compete with other private equity mastodons not only for available assets but also for investment targets. This factor may affect the company's ability to grow organically over the long term.

- The impact of risks arising from the absence of a permanent CEO is limited. Nevertheless, possible future reshuffles in the top management team could lead to uncertainty and affect the company's ability to successfully grow assets under management.