What's the idea?

- Arhaus is focused on a wealthy audience, which is less susceptible to adverse macroeconomic conditions.

- By focusing on the premium segment, Arhaus has greater pricing power and the ability to pass on price increases to its customers.

- In the long term, Arhaus has room to more than triple its number of stores.

- Despite strong growth, the share of online sales in the revenue structure remains low, suggesting significant potential for e-commerce growth.

- Given that Arhaus still has a weak geographic footprint, there is still potential to benefit from economies of scale and improve operating leverage.

- The company trades at a discount to the industry average. According to the Wall Street consensus, the upside potential is over 70%.

About Company

Arhaus (ARHS) designs and markets premium furniture, lighting, textiles, decor, and other premium home products. The company operates 81 stores in 28 states in the US and also sells products through its own website. Arhaus was founded in 1986 and is headquartered in Boston Heights, Ohio.

Why do we like Arhaus Inc?

Reason 1. Industry potential and strong competitive position

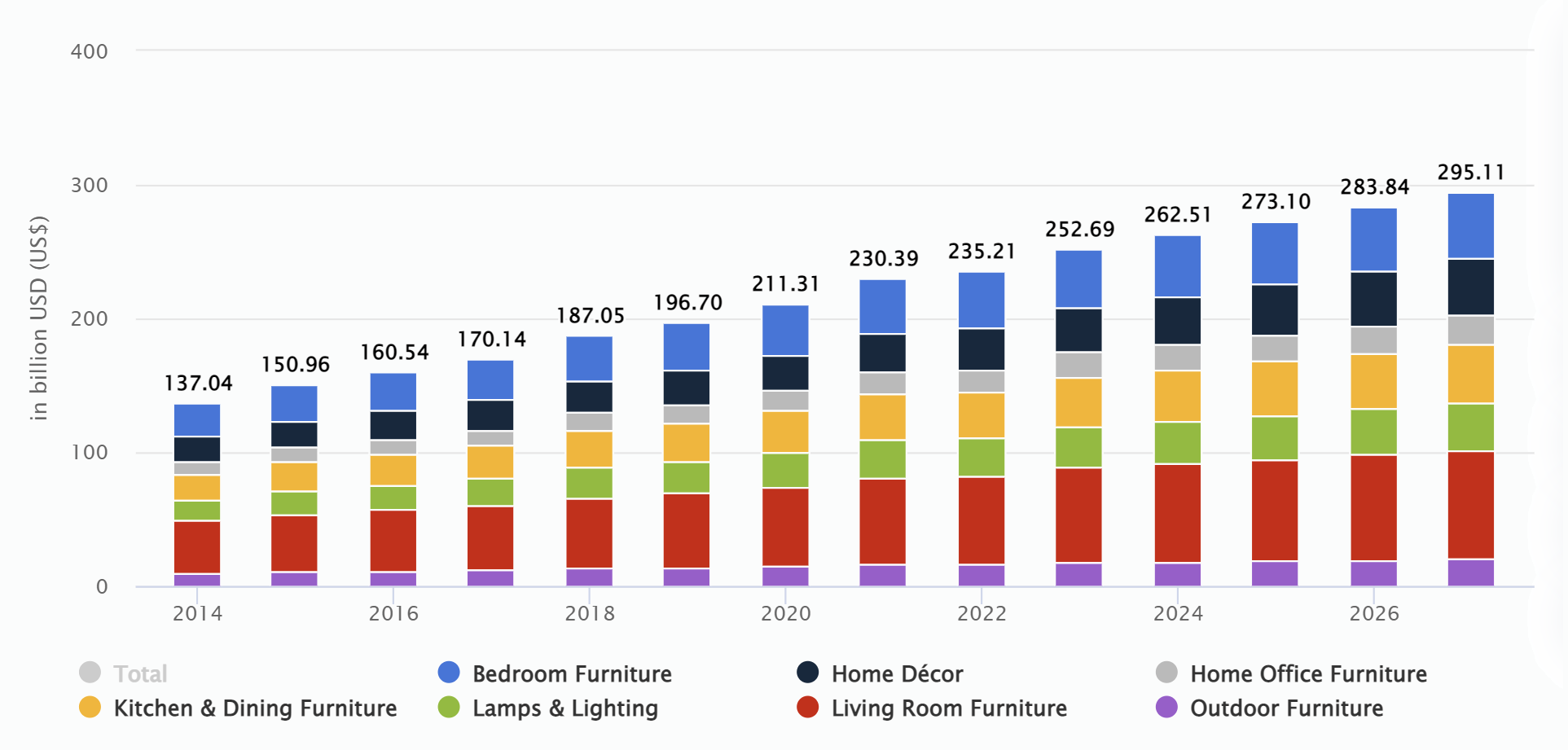

The ongoing urbanization and the growth of the construction and hospitality industries support the increasing demand for indoor and outdoor furniture. According to Statista, the US furniture market is valued at $235 billion and is expected to reach $295 billion by 2026, implying growth at a compound annual rate (CAGR) of 3.98% over the forecast period.

Expected dynamics of the target market

The furniture industry is characterized by a large volume and a high fragmentation degree. Due to the relatively low market entry threshold, in addition to giants such as Ikea, Wayfair, and Williams-Sonoma, there are a large number of family firms and small companies specializing in a particular segment.

The Arhaus business model has several advantages over that of its competitors. About half of the company's products are locally made in the US. This has provided a significant contribution to Arhaus's excellent performance results in the past two years when many of the company’s market peers faced supply chain challenges.

Arhaus is focused on serving a wealthy audience. The company sells one-of-a-kind pieces of furniture produced by small manufacturers. As a result, Arhaus has been able to build a loyal customer base of people with annual incomes over $100,000 who are willing to overpay for aesthetics and exclusivity. Thus, the company's target audience is less susceptible to unfavorable macroeconomic conditions than buyers in the lower and middle price segments.

In addition, due to its focus on the premium segment, Arhaus has greater pricing power and is able to pass on price increases to its customers, while maintaining an acceptable level of margins.

Reason 2. Significant room for further expansion

Arhaus estimates its target market at $100 billion. Thus, with annual revenue of $1.23 billion, the company’s market share is less than 1.5%. Arhaus’ relatively low penetration rate is also reflected in the comparatively low number of showrooms. By the end of 2022, the company operated 81 stores in 28 states. The total number of stores included 72 traditional showrooms and 10 small studios (Design and Loft Studios) — a concept launched just two years ago.

Geographical presence of Arhaus

The company expects to open 12 new showrooms in 2023, implying 14% year-on-year growth. According to strategic plans, Arhaus expects to open 5-7 showrooms per year. The company's management believes that the market potential allows it to have more than 165 showrooms and more than 100 design studios in the long term perspective. Given the relatively low level of the company’s geographic coverage, such estimates look extremely rational. By comparison, Williams-Sonoma ended the year with 489 stores in the US and 530 worldwide. This leaves room for Arhaus to more than triple growth in the long term.

Arhaus also has significant potential to develop online sales. In 2022, the e-commerce segment grew by 43% and became the company’s fastest growing sales channel. However, the share of online sales still remains quite low at 17% of total revenue. For comparison, the average share of online sales in the industry is 35%.

Geographic expansion and growing e-commerce business would be hard to achieve without the development of logistics infrastructure. In 2022, Arhaus launched a distribution center in Dallas, enabling faster shipping in the US western regions. In addition, the company expanded its distribution center in Ohio. Through the implementation of these initiatives, Arhaus reduced the backlog and completed orders that were planned to be postponed to 2023. Management believes that the logistics infrastructure expansion will support the company’s growth in the next 7-10 years.

Financial performance

Arhaus' 2022 financial results can be summarized as follows:

- Revenue stood at $1.23 billion, up 54% from a year earlier. Growth was driven by both new store openings and higher same-store sales.

- Gross profit increased from $329.9 million to $525.1 million. Gross margin rose from 41.40% to 42.72%.

- Operating income increased from $33.4 million to $184.7 million. The operating margin rose from 4.18% to 15.03% due to strong sales growth and improved operating leverage.

- Net income amounted to $136.6 million compared to $21.1 million a year earlier. Net margin increased from 2.65% to 11.12%.

Dynamics of the company's financial results

Company margin dynamics

- The company's margins have risen substantially in recent years, driven by rapid sales growth and consequent reductions in fixed costs as a percentage of revenue. Given that Arhaus still has a weak geographic footprint, there is still potential to benefit from economies of scale and improve operating leverage.

- In 2022, cash from operations amounted to $74.5 million compared to $146.2 million a year earlier. Free cash flow decreased from $98.4 million to $21.8 million. The decline was driven by lower customer deposits as Arhaus reduced its backlog and completed orders that were scheduled to be deferred to next year.

Company’s cash flow

Arhaus has a strong balance sheet: total debt is $52.37 million, while total cash and short-term Investments account for $152.5 million. Thus, net debt is negative and equals to -$100.2 million.

Valuation

The Arhaus stock has lost a significant amount of value over the past month as management issued weak guidance for 2023. The forecast provides for same-store sales in the range of -4% to +1% from current levels and EBITDA of $180 million to $195 million versus $205 million according to a consensus forecast. The main reason behind the weak outlook is that the firm sold a significant part of the backlog in 2022. In addition, new stores are not expected to open until the end of the year, meaning they will not make a significant contribution to the company's financial results.

However, the recent market correction provided investors with an attractive opportunity regarding the stock. Despite high growth rates and potential for further expansion, Arhaus trades at a discount to the industry average on the following multiples: EV/EBITDA — 6.67x, P/E — 8.46x, Forward P/E — 10.94x.

Comparable valuation

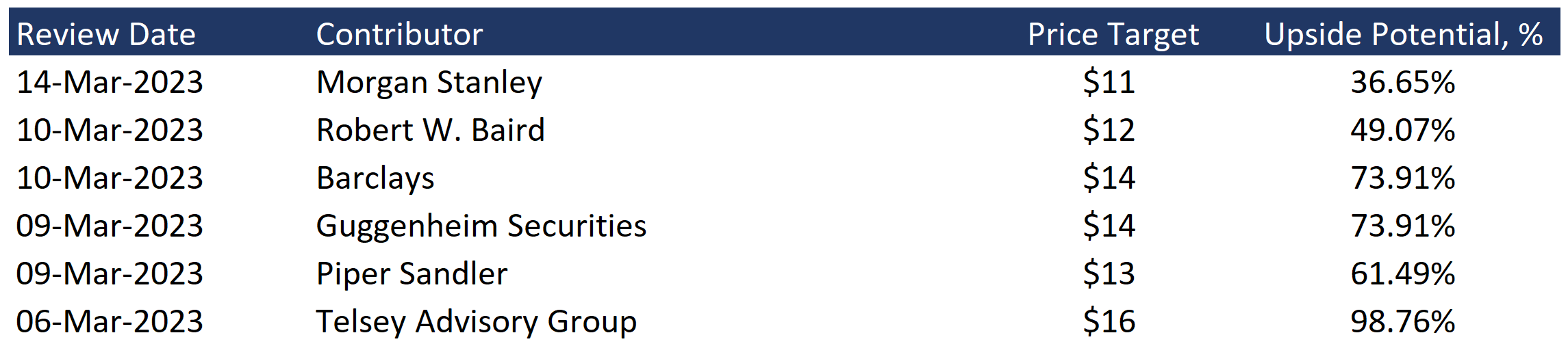

The minimum price target from investment banks was set by Morgan Stanley is $11 per share. Telsey Advisory estimates ARHS at $16 per share. According to the Wall Street consensus, the stock’s fair market value is $13.2, implying a 76% upside potential.

Price targets of investment banks

Key risks

- The furniture industry is highly correlated with the real estate market. Weaker real estate demand driven by higher interest rates could dampen results for furniture retailers, including Arhaus.

- Arhaus operates in a highly competitive market with several peers having significantly larger resources. This factor may affect the company's ability to grow organically in the long term.