What's the idea?

- Re-establishing supply chains can help improve business margins

- The arrival of a new CEO can accelerate the company's growth

- Low debt burden will help to cope with short-term difficulties

About Company

Foot Locker Inc. — is a footwear and apparel retail company. Its brand portfolio includes Foot Locker, Lady Foot Locker, Kids Foot Locker, Champs Sports, Eastbay, atmos, WSS, Footaction, and Sidestep. Foot Locker operates 2,799 shops located predominantly in shopping malls and urban shopping areas in 28 countries. Geographically, the company's business is divided into three segments:

- North America

- Europe, the Middle East and Africa

- Asia-Pacific region

In addition to physical outlets, the company uses omnichannel capabilities and allows purchases to be made via websites and apps.

Why do we like Foot Locker Inc.?

Reason 1. Rebuilding supply chains

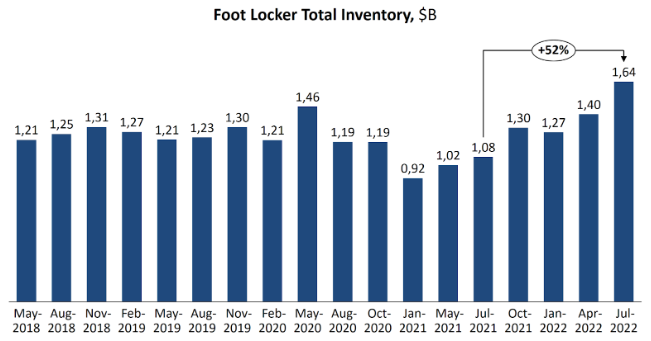

Like many other retailers, Foot Locker has experienced supply chain challenges that have impacted business margins and inventory accumulation. As the chart below shows, as of June 30, 2022, the company's inventory had grown by 52% year-on-year to $1.65 billion.

In the future, we expect supply chains to have much less of an impact on business because

- According to DHL research, there is a global shift towards better and more sustainable supply chains, including through the creation of geographically diversified operations. While Reuters analysis suggests that it will take until 2024 to fully recover in some sectors, we anticipate that the effects of the implemented measures will be noticeable as early as 2023.

- Container shipping costs are declining: the Freightos Baltic Index (FBX), reflecting this trend, fell from $9,293 at the start of the year to $3,045 as of November 3.

The Global Supply Chain Pressure Index, which has been rapidly approaching zero for the past five months, has also fallen due to the abovementioned factors.

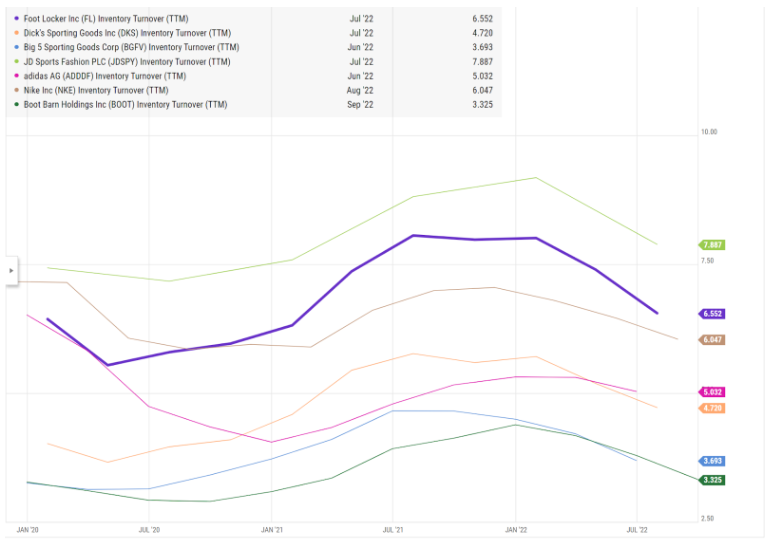

During the Q2 earnings conference call, management also reported that Foot Locker is beginning to overcome the supply difficulties common to other retailers. In terms of inventory turnover, Foot Locker (the purple line in the chart below) is now broadly in line with overall market trends, with the figure itself at a fairly high 6.6x.

In our view, the improved supply chain situation will allow Foot Locker to improve its business margins and increase its turnover rate, which could positively impact the company's capitalisation.

Reason 2. Positive data in the industry

If we analyse the latest financial results of US Apparel retail companies according to Yahoo Finance, we see the following:

- October 28 — Carters — expected EPS: 1.7, EPS in report: 1,67

- October 26 — Boot Barn Holdings — expected EPS: 0.9, EPS in report: 1,06

- October 12 — Aritzia Inc. — expected EPS: 0.33, EPS in report: 0.44

- October 12 — Fast Retailing Co. — expected EPS: -125.02, EPS in report: 347,4

- October 11 — ABC-Mart — expected EPS: 60.37, EPS in report: 76,33

Thus, most of the retailers performed better than expected. If Foot Locker joins this trend, it could have a markedly positive impact on the company's stock price.

After analysing the reports of the companies presented above, we would like to highlight the following:

- Carters reports a continued recovery in supply chains, with Boot Barn lowering its online sales forecast due to competitors having products back in stock on online sites. This is further evidence of a global supply chain recovery.

- It is noted, however, that difficulties remain, and a full recovery is yet to be seen.

Among other things, on June 27, Foot Locker reported that it had signed an agreement to sell the Team Sales business unit to BSN Sports. As this business generated less than 1% of the company's annual sales, we believe the deal will benefit the company. In addition to the cash flow from the sale, the deal will help management optimise the company's structure, allowing them to focus staff resources on strategically important projects.

Reason 3. New CEO

On August 19, the company announced that as part of the planned process, former company president Richard Johnson will step down from his post with effect from September 1 and Mary Dillon, former CEO of Ulta Beauty, will take his place. To ensure a smooth transition, Johnson will remain with the company as an advisor until April 2023.

We consider this news positive, as Dillon has 35 years of experience leading a consumer-facing business. In her eight years at the helm, Ulta Beauty has made good progress, with a CAGR of 16% in revenue and a market capitalisation that has tripled, making it the leading cosmetics shop in the US. In addition, Dillon has executive experience at companies such as U.S. Cellular, McDonalds and PepsiCo.

A fresh perspective on the company's business processes and a wealth of experience could help accelerate Foot Locker's growth rate. Still, it will probably take around 3-4 quarters for these expectations to be incorporated into the company's stock price before Dillon's performance can be quantified.

Financial Indicators

The company's results for the last 12 months:

TTM revenue: up from $8.72 billion to $8.77 billion

TTM operating profit: down from $889 million to $691 million:

in terms of operating margin -/down from 10.2% to 7.9% mainly due to increase in SG&A expenses from 20.1% to 21.6%

TTM net profit: down from $1.02 billion to $0.49 billion

In terms of net margins, we see a decline from 11.7% to 5.6%

Operating cash flow: decrease from $858 mln to $162 mln, mainly due to lower profits and investment in inventory

Free cash flow: down from $695 million to $116 million

Based on the results of the last reporting period ending on July 30, 2022:

Revenue: down from $2.28 billion to $2.07 billion

Operating profit: decreased from $268 million to $157 million:

In terms of the operating margin: down from 11.8% to 7.6% due to SG&A expenses rising from 19.8% to 21.9%

Net profit: decreased from $430 million to $94 million

In terms of net margins: down from 18.9% to 4.6% due to no profit from non-operating investment activities in Q2 2022 (last year it was $291 million).

Operating cash flow: decreased from $402 million to $102 million, mainly due to investment in an inventory of $413 million

Free cash flow: down from $415 million to $258 million

The company reported negative financial results in the last quarter, but we expect positive supply chain trends to enable it to realise inventory faster and turn cash flows in the direction of recovery.

- Cash and cash equivalents: $386 million

- Net debt: $76 mln

- Net debt/normalised EBITDA TTM: 0.07x

Although the company has relatively small cash reserves given the negative cash flows, Foot Locker's debt load is around zero, giving it sufficient financial strength to cope with temporary difficulties.

Evaluation

In terms of trading multiples, Foot Locker is undervalued relative to the industry as a whole:

Foot Locker pays a dividend to its shareholders with a current annual yield of 5.08%.

Among other things, according to the Form 10-Q, as of July 30, 2022, the company had about $1.1 billion left in its buyback programme authorisation, which represents about 38% of the company's market capitalisation. The programme has no time constraints and, in our view, can be actively used after the cash flows recover.

Ratings of other investment houses

The minimum price target set by William Blair is $29 per share. Guggenheim and Bank of America have, in turn, set a target price of $43. According to the consensus, the fair value of the stock is $37.6 per share, which suggests an upside of 42.17%.

Key risks

- If the company is unable to cope with a short-term slump in cash flow, it will have to raise debt capital, which could have a negative impact on shareholder value due to increased risk.

- A new president of the company, in addition to new opportunities, also brings risks of mismanagement.

Comments

Submitted by Elliott on Wed, 11/16/2022 - 03:29

I think the admin of this website is genuinely working hard for his site, as here every material is quality based information.